Déjà

Vu? Auto-Loan Delinquency Hits New Record High For, Um … Some Reason

https://hotair.com/archives/2019/02/13/deja-vu-auto-loan-delinquency-hits-new-record-high-um-reason/

February 13, 2019

Is this a failure of the labor market? Or is it a rerun on a

smaller scale of the financial crash that created the Great Recession?

According to the Federal Reserve of New York, a record number

of Americans are three months or more behind on their car payments —

even worse than during the crash in the previous decade:

A record 7 million Americans are

90 days or more behind on their auto loan payments, the Federal Reserve Bank of

New York reported Tuesday, even more than during the wake of the financial

crisis.

Economists warn that this is a

red flag. Despite the strong economy and low unemployment rate, many Americans

are struggling to pay their bills.

That seems incongruous in an economy where growth has spread out

across the spectrum. Job creation has picked up, wages have increased in real

terms at the best rate since before the Great Recession, and the overhang of

discouraged workers finally appears to be evaporating. Still, the New York Fed

blames this on a lack of widespread impact from the economy:

“The substantial and growing number of

distressed borrowers suggests that not all Americans have benefited from the

strong labor market,” economists at the New York Fed wrote in a blog post.

Maaaayyyyybeee, but there’s something else

going on here too. In the same blog post, the NY Fed also notes that the

delinquencies are mainly coming

from subprime loans:

The flow into serious delinquency (that is, the share of

balances that were current or in early delinquency that became 90+ days

delinquent) in the fourth quarter of 2018 crept up to 2.4 percent,

substantially above the low of 1.5 percent seen in 2012.

In the chart below, we

disaggregate the delinquency rate by the borrower’s credit score at

origination. The relative performance between each credit score group stands

out immediately; but the increase in delinquency is most obvious among the

loans of the two groups of lower-score borrowers, shown by the blue and red

lines in the chart below. Borrowers with credit scores less than 620 saw their

transitions into delinquency exceed 8 percent in the fourth quarter (annualized

as a moving sum), a development that is surprising during a strong economy and

labor market. Meanwhile, the delinquency transitions among those with the

highest credit scores have remained stable and very low. In aggregate, the

increasing share of prime loans has partially offset the deteriorating

performance of the subprime sector.

That increase in the percentage of prime lending

as a hedge against subprime risk has only happened recently. Over the last

several years, subprime lending increased significantly, including in the

auto-loan market. By 2013,

subprime auto lending had increased 18.8%, while subprime auto-loan securities

had grown 63.5%. Many of those loans carried high

interest rates, sometimes as high as revolving credit-card rates.

Did people expect to marry credit risks to high interest rates and not get defaults?

The Washington Post buries the scope of that risk towards the

end of their article:

He noted that non-prime and

subprime auto loans increased from 28 percent of the market in 2009 to 39

percent in 2015, a reminder of how aggressively lenders went after borrowers

who were on the margin of being able to pay. More lenders are giving people six

or seven years to repay now vs. four of five years in the past, according to

Experian, another tactic to try to make loans look affordable that might not

otherwise be.

That’s a more accurate look at the aggressive nature of subprime

lenders, which also has echoes of the housing bubble and its 2008 collapse. The

NY Fed blames this mainly on “auto finance reporters,” but this chart shows a

more nuanced picture:

Half of all auto-finance reporter loans are subprime, which

accounts for $75 billion in outstanding debt. However, 25% of all auto loans

written by large institutions are also subprime — and that accounts for over

$97 billion in outstanding debt. Those “too big to fail” institutions

apparently didn’t learn any lessons, and neither did the investors who are

buying securities based on subprime debt. And how much backstop are the auto finance

reporters getting from the large banks?

The only potential good news is that auto-loan debt isn’t large

enough to knock out financial institutions — on its own, anyway. Does anyone

want to bet that subprime lending in the housing markets hasn’t followed along in the same

manner, though?

Three Ways to Avoid

Death of Dollar – and America

Three Ways to Avoid

Death of Dollar – and America

Little remains of the vast edifice of family, community and

faith relationships that once unified and anchored the American way of life.

These things have not disappeared from the horizon. They are still important,

but they have deteriorated. There is no more consensus about what they mean,

and they no longer serve as anchors of certainty.

One final anchor remains that does unite Americans. This

anchor survives despite everything. Now, even this seems targeted for

destruction.

The Last Anchor That Unites Everyone

It seems almost irreverent to affirm, but this last anchor is

the American dollar. Money is not supposed to be a social anchor. Other more

immaterial things—moral, principles, social bonds—should play this role.

However, today money bridges the seemingly unbridgeable chasms that polarize

the nation in a way nothing else can.

It is not just money. What unites Americans across the

board is the dollar, which is accepted everywhere either in its physical or

virtual form. No one questions its dominant role. As the world’s reserve

currency, it keeps global trade running while everything else falls apart. When

the other anchors fail, the dollar is always there to spend ways out of a

crisis.

Calling the dollar the last anchor does not mean that money

should or does run everything. The dollar is much more than a simple unit of

currency. It has immense symbolic importance since it is attached to notions of

national sovereignty, power and the American way of life. The dollar sustains

the myth of an America that will never fail. Thus, its fall is unimaginable to

many Americans who cannot visualize the country without it.

A Culture of Intemperance

However, there is a darker side to the dollar. It

facilitates the frenetic intemperance of a culture that

rejects limits. People want everything instantly and effortlessly, and the

dollar is ever-ready to supply the means to buy fleeting happiness. The

government offers its dollar subsidies to keep people dependent and happy. So

many others seem willing to sustain this frenzied lifestyle by contracting debt

of all types—private, corporate and governmental.

And the dollar is the ideal instrument for this frenzy. It

is stable, flexible and plentiful. What sustains the dollar is the world’s

willingness to buy U.S. Treasury bonds as a stable investment. There seems to

be no limit to the frenetic appetite for these debt dollars worldwide.

However, the dollar cannot solve the nation’s problems no

matter how many trillions are thrown at them. Like any currency, the dollar is

only as strong as the society that sustains it. With the decline of America’s

institutions, it is inevitable that the dollar too will face a decline—perhaps

radically and dramatically.

This dollar decline could happen in three different ways,

especially in these erratic times.

The Post-2008 U.S. Is Unprepared for New

Economic Crises

First, it can be destroyed by overconfidence. The grand

myth holds that the dollar cannot be destroyed because it has never been

destroyed before, despite several close calls.

There is no logic to this affirmation. All things temporal

can be destroyed, especially if they are neglected. However, the argument does

carry some weight in a culture that is run on emotions and feelings.

The fact is that the dollar is surviving on borrowed time.

The 2008 crisis provoked world finance leaders to use every tool in their

toolboxes to fix the crisis. Programs of zero or even negative interest, quantitative easing and other

vehicles have all run their course with limited effects. Overconfident

Americans need to take notice of dangers on the horizon.

Risks still abound in today’s global economy with trade

wars and political tensions. Many economic observers say that should a major

crisis hit the world economy, the financial systems could go down. And there

are very few new tricks that can be employed to stem the grave damage since the

root causes are not being addressed.

The mantra that the dollar is indestructible is hardly

reassuring.

The Very Real Debt Threat

The second factor that could cause the dollar’s decline is

debt in all its forms, especially American sovereign debt. When the world no

longer wants to buy American debt, the crushing burden of high interest rates

will have disastrous consequences for the nation.

The present governmental debt shows no sign of diminishing.

People have gotten used to the idea of annual $800 billion deficits. It will be

the new normal over the coming years as no Senator or U.S. Congressman wants to

take things off their shopping lists or face the firestorm of public opprobrium

for urging fiscal restraint.

Also, corporate debt now stands at nearly $9 trillion. The quality of

investment-grade bonds has deteriorated with many in or bordering on junk

category. This debt could trigger defaults, bankruptcies, burst bubbles of

immense proportions, all of which will weigh heavily on the dollar.

Similarly, personal debt has climbed back to pre-2008

crisis levels.

Indeed, ours is a world awash in debt of all sizes, types,

and nations. As the world’s reserve currency, the dollar cannot escape the

reverberations of a world financial crisis when major players default.

Sidelining the Dollar as the World’s Reserve

Currency

The final threat is more deliberate and targeted. As the

preferred unit of currency in commodity markets, the dollar is under direct

attack today through a new European Union mechanism called a Special Purpose Vehicle (SPV).

Everyone knows that no currency (or even basket of

currencies) can replace the dollar as the world’s reserve currency. However,

the European Union, China, Russia and Iran are seeking to create a

clearinghouse that will run circles around U.S. sanctions against the Islamic

Republic of Iran. They are setting up a credit system that will allow the

barter trading of commodities without the use of American dollars.

In this way, the dollar can come to be challenged and

sidelined by many major countries in international trade, and potentially even

losing its privileged status.

The Collapse of the Postwar Order

Any of these three ways can drag down the U.S. dollar from

its post-World War II throne. This would be disastrous since it would hasten

the collapse of the postwar order with no replacement save chaos and

disorder.

However, the greatest catastrophe would be for American

society. The collapse of America’s last anchor will increase the fragmentation

and polarization of the nation. All these three ways are avoidable if America’s

political leaders would apply themselves energetically and without further loss

of time toward addressing the root causes of the threats the nation faces. It

would involve the need for great restraint, sacrifice and new national

priorities.

The real problem facing America today is much more a moral

problem than an economic one. Society needs anchors, especially moral

anchors to unify the nation. When those anchors are gone, the nation is left

rudderless in a sea of chaos.

John Horvat II is a scholar, researcher, educator, international speaker,

and author of the book Return

to Order: From a Frenzied Economy to an Organic Christian Soceity--Where We've

Been, How We Go Here, and Where We Need to Go. He lives in Spring Grove, Pennsylvania, where he is the

vice president of the American Society for the Defense of Tradition, Family and

Property.

After Lehman's

Collapse: A Decade of Delay

Now that the 2018

midterms are over, folks can address the elephant in the room. If one tuned

into Fox Business midday on January 7, one heard legendary corporate raider

Carl Icahn dilate on the dimensions of the pachyderm, which he pegged at $250

trillion. That’s the size of worldwide debt. But can that be right -- it’s

more than eleven times the official U.S. federal government’s debt? And in case

you didn’t notice, it is a quarter of one quadrillion bucks. Pretty soon we’ll

be talking real money.

Icahn’s $250T quotation

for worldwide debt came out last year. On September 13, Bloomberg ran “$250

Trillion in Debt: the World’s Post-Lehman Legacy” by Brian Chappatta, who

draws off data from the Institute of International Finance’s July 9 “Global Debt

Monitor,” (to read IIF reports, one must sign up). Chappatta wonders how the

world’s central bankers can “even pretend to know how to reverse what they’ve

done over the past decade”:

[Central banks] kept

interest rates at or below zero for an extended period […] and used bond-buying

programs to further suppress sovereign yields, punishing savers and promoting

consumption and risk-taking. Global debt has ballooned over the past two

decades: from $84 trillion at the turn of the century, to $173 trillion at the

time of the 2008 financial crisis, to $250 trillion a decade after Lehman Brothers

Holdings Inc.’s collapse.

Chappatta breaks global

debt down into four categories: financial corporations, nonfinancial

corporations, households, and governments. In every category, global nominal

debt rose from 2008 to 2018, with the debt of governments hitting $67T. In the

important debt-as-a-percentage-of-gross-domestic-product measurement, three of

the categories rose while only financial corporations fell, “leaving their

debt-to-GDP ratio as low as it has been in recent memory.” Global banks seem to

be “healthier and more resilient to another shock.” After reporting on

worldwide debt, Chappatta then looks at U.S. debt.

What’s interesting about

debt in America is that as a percentage of GDP, households and financial

corporations have sharply reduced their debt. It is only government in America

that has seen a sharp debt-to-GDP uptick, and it was quoted at more than 100

percent of GDP. That’s rather higher than for all government debt worldwide.

Since the U.S. isn’t the

only nation that has been busy buying bonds and creating money, one might

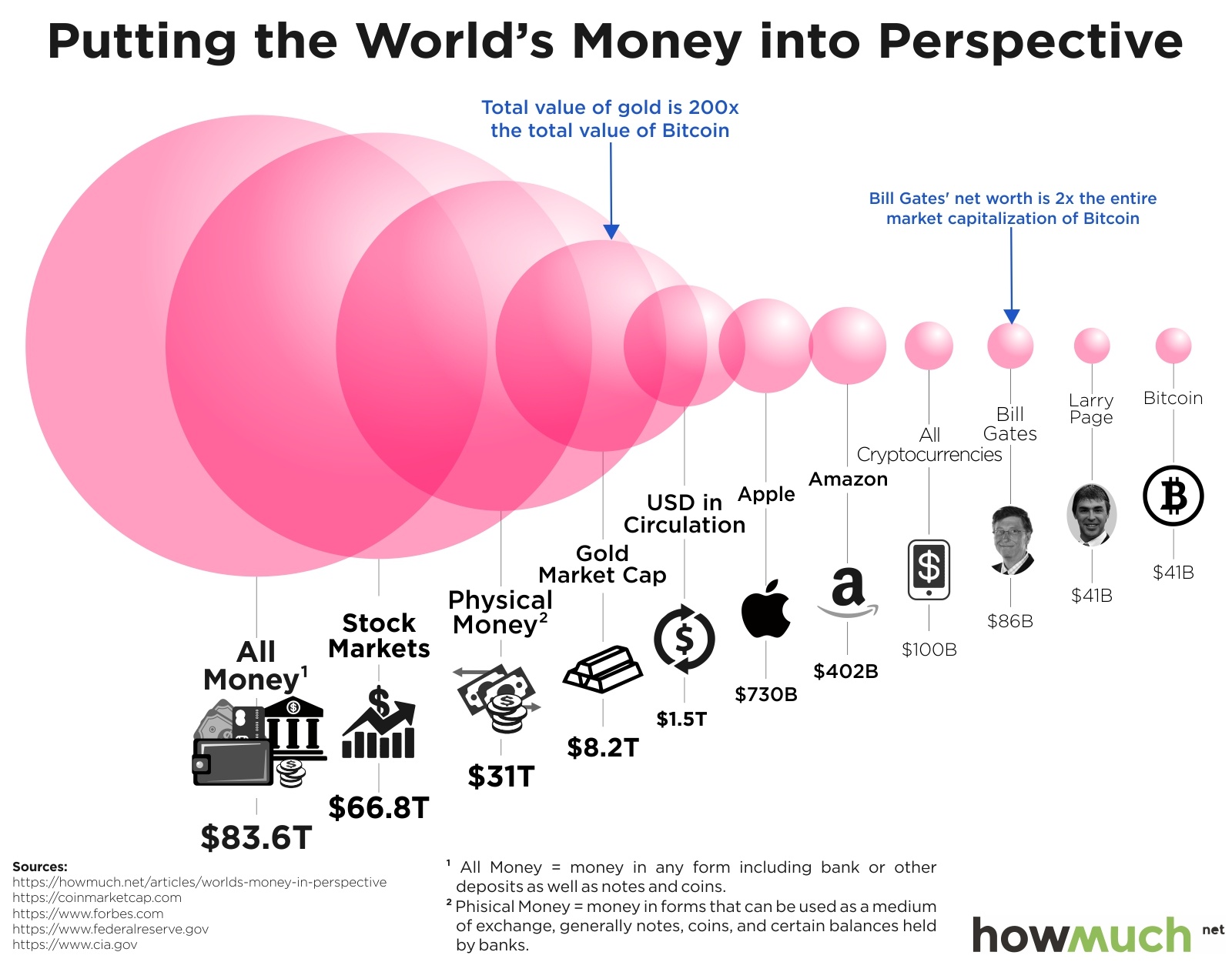

wonder just how much money there is in the world. In June of 2017,HowMuch put out

“Putting the

World’s Money into Perspective,” which is a nice little graphic that puts the

category “All Money” at $83.6T.

{kind=link}

In November of

2017, MarketWatch ran

“Here’s

all the money in the world, in one chart” by Sue Chang, who in

her short intro to the chart has some interesting things to say about global

money, including cryptocurrencies. She writes of “narrow money” and “broad money” and pegs the latter at

$90.4T, (or what Sen. Everett Dirksen would call “real money”.) If you want to

examine Chang’s chart more closely, I’ve “excised”

it here for your convenience; don’t miss the notes on the right

margin. (Because its depth is 13,895 pixels, you might want to just save the

chart to your computer rather than print it off.)

{kind=link}

So, in addition to an

historic run-up in debt, there’s been a monster amount of new money created.

Chappatta calls it the “grandest central-bank experiment in history.” His use

of “experiment” is apropos, as one wonders whether the world’s central bankers

and their economists really know what they’ve been doing.

One ray of hope might

just be President Trump’s choice of Jerome Powell as Chairman of the Federal

Reserve, (Trump has such good instincts about people). One can get a sense of

the man from his January talk with David Rubenstein at the Economic Club of

Washington, D.C. (video and

transcript). It’s refreshing that Mr. Powell disdains the “Fed speak” used

by his predecessors.

Chappatta’s article is

quite worth reading, and it’s not very long. The charts are user-friendly,

although animated ones are a bit “creative.” The last section, “China Charges

Forward,” is especially worthwhile.

This is the post-Lehman

legacy. To pull the global economy back from the brink, governments borrowed

heavily from the future. That either portends pain ahead, through austerity

measures or tax increases, or it signals that central-bank meddling will become

a permanent fixture of 21st century financial markets.

Given those

alternatives, let’s try a little austerity. But austerity would entail spending

cuts, and Congress has a poor history in that regard. In fact, since fiscal

2007, the year before the financial crisis, total federal spending has gone

from $2.72T a year to more than $4T. While austere citizens deleverage and get

their fiscal affairs in order, Congress shamefully borrows and spends like

never before.

Congress’ solutions are

to bail out, prop up, and do whatever it takes to avoid reforming what it has

created. So they farm out their responsibilities to the Federal Reserve.

Indeed, in the July 17, 2012 meeting of the Senate Banking Committee (go to the

53:50 point of this C-SPAN video), Chuck Schumer told Federal Reserve Chairman

Ben Bernanke the following:

So given the political

realities, Mr. Chairman, particularly in this election year, I'm afraid the Fed

is the only game in town. And I would urge you to take whatever actions you

think would be most helpful in supporting a stronger economic recovery… So get

to work, Mr. Chairman. (Chuckles.)

So the Fed is “the only

game in town” because there are only monetary solutions for the economy, right?

There aren’t any fiscal solutions, as they would involve Congress, and Congress

is busy running for re-election, right? Sounds like you’re abdicating your

responsibilities, Chuck.

The last decade has been

an exercise in delay. Congress has avoided doing the difficult and unpopular

things that would help avoid future financial collapses. If Congress were

serious about balancing the budget, then social programs would be on the chopping

block, because that’s where the real

money goes.

"The Federal Reserve is a key mechanism for perpetuating this

whole filthy system, in which "Wall Street rules."

Wall Street rules

The Federal Reserve sent a clear message to Wall Street on

Friday: It will not allow the longest bull market in American history to end.

The message was received loud and clear, and the Dow rose by more than 700

points.

Hundreds of thousands of federal workers remain furloughed or

forced to work without pay as the partial government shutdown enters its third

week, but the US central bank is making clear that all of the resources of the

state are at the disposal of the financial oligarchy.

Responding to Thursday’s market selloff following a dismal

report from Apple and signs of a manufacturing slowdown in both China and the

US, the Fed declared it was “listening” to the markets and would scrap its

plans to raise interest rates.

Speaking at a conference in Atlanta, where he was flanked by his

predecessors Ben Bernanke and Janet Yellen, both of whom had worked to reflate

the stock market bubble after the 2008 financial crash, Chairman Jerome Powell

signaled that the Fed would back off from its two projected rate increases for

2019.

“We’re listening sensitively to the messages markets are

sending,” he said, adding that the central bank would be “patient” in imposing

further rate increases. To underline the point, he declared, “If we ever came

to the conclusion that any aspect of our plans” was causing a problem, “we

wouldn’t hesitate to change it.”

This extraordinary pledge to Wall Street followed the 660 point

plunge in the Dow Jones Industrial Average on Thursday, capping off the worst

two-day start for a new trading year since the collapse of the dot.com bubble.

William McChesney Martin, the Fed chairman from 1951 to 1970,

famously said that his job was “to take away the punch bowl just as the party

gets going.” Now the task of the Fed chairman is to ply the wealthy revelers

with tequila shots as soon as they start to sober up.

Powell’s remarks were particularly striking given that they

followed the release Friday of the most upbeat jobs report in over a year, with

figures, including the highest year-on-year wage growth since the 2008 crisis,

universally lauded as “stellar.”

While US financial markets have endured the

worst December since the Great Depression,

amid mounting fears of a looming recession

and a new financial crisis, analysts have been

quick to point out that there are no “hard”

signs of a recession in the United States.

Both the Dow and the S&P 500 indexes have fallen more than

15 percent from their recent highs, while the tech-heavy NASDAQ has entered

bear market territory, usually defined as a drop of 20 percent from recent

highs.

The markets, Powell admitted, are “well ahead of the data.” But

it is the markets, not the “data,” that Powell is listening to.

Since World War II, bear markets have occurred, on average,

every five-and-a-half years. But if the present trend continues, the Dow will

reach 10 years without a bear market in March, despite the recent losses.

Now the Fed has stepped in effectively to pledge that it

will

allocate whatever resources are needed to ensure that no

substantial market correction takes place. But this

means

only that when the correction does come, as it

inevitably

must, it will be all the more severe and the Fed will have

all the less power to stop it.

From the standpoint of the history of the institution, the Fed’s

current more or less explicit role as backstop for the stock market is a

relatively new development. Founded in 1913, the Federal Reserve legally has

had the “dual mandate” of ensuring both maximum employment and price stability

since the late 1970s. Fed officials have traditionally denied being influenced

in policy decisions by a desire to drive up the stock market.

Federal Reserve Chairman Paul Volcker, appointed by Democratic

President Jimmy Carter in 1979, deliberately engineered an economic recession

by driving the benchmark federal funds interest rate above 20 percent. His

highly conscious aim, in the name of combating inflation, was to quash a wages

movement of US workers by triggering plant closures and driving up

unemployment.

The actions of the Fed under Volcker set the stage for a vast

upward redistribution of wealth, facilitated on one hand by the trade unions’

suppression of the class struggle and on the other by a relentless and dizzying

rise on the stock market.

Volcker’s recession, together with the Reagan administration’s

crushing of the 1981 PATCO air traffic controllers’ strike, ushered in decades

of mass layoffs, deindustrialization and wage and benefit concessions, leading

labor’s share of total national income to fall year after year.

These were also decades of financial deregulation, leading to

the savings and loan crisis of the late 1980s, the dot.com bubble of 1999-2000,

and, worst of all, the 2008 financial crisis.

In each of these crises, the Federal Reserve carried out what

became known as the “Greenspan put,” (later the “Bernanke put”)—an implicit

guarantee to backstop the financial markets, prompting investors to take ever

greater risks.

In 2008, this resulted in the most sweeping and systemic

financial crisis since the Great Depression, prompting Fed Chairman Bernanke,

New York Fed President Tim Geithner and Treasury Secretary Henry Paulson (the

former CEO of Goldman Sachs) to orchestrate the largest bank bailout in human

history.

Since that time, the Federal Reserve has carried out its most

accommodative monetary policy ever, keeping interest rates at or near zero

percent for six years. It supplemented this boondoggle for the financial elite

with its multi-trillion-dollar “quantitative easing” money-printing program.

The effect can be seen in the ever more staggering wealth of the

financial oligarchy, which has consistently enjoyed investment returns of

between 10 and 20 percent every year since the financial crisis, even as the

incomes of workers have stagnated or fallen.

American capitalist society is hooked on the toxic growth of

social inequality created by the stock market bubble. This, in turn, fosters

the political framework not just for the decadent lifestyles of the financial

oligarchs, each of whom owns, on average, a half-dozen mansions around the world,

a private jet and a super-yacht, but also for the broader periphery of the

affluent upper-middle class, which provides the oligarchs with political

legitimacy and support. These elite social layers determine American political

life, from which the broad mass of working people is effectively excluded.

The Federal Reserve is a key mechanism for

perpetuating this whole filthy system, in

which “Wall Street rules.” But its services in behalf

of

the rich and the super-rich only compound the fundamental

and

insoluble contradictions of capitalism, plunging the system

into

ever deeper debt and ensuring that the next crisis will be

that

much more violent and explosive.

In this intensifying crisis, the working class must assert its

independent interests with the same determination and ruthlessness as evinced

by the ruling class. It must answer the bourgeoisie’s social counterrevolution

with the program of socialist revolution.

the depression is already here for most of us below the

super-rich!

Trump and

the GOP created a fake economic boom on our collective credit card:

The equivalent of maxing out your credit cards and saying look how

good I'm doing right now.

*

Trump criticized Dimon in 2013

for supposedly contributing to the country’s economic downturn. “I’m

not Jamie Dimon, who pays $13 billion to settle a case and then pays $11

billion to settle a case and who I think is the worst banker in

the United States,” he told reporters.

*

"One

of the premier institutions of big business, JP Morgan Chase, issued

an internal report on the eve of the 10th anniversary of the 2008

crash, which warned that another “great liquidity crisis”

was possible, and that a government bailout on the scale of that

effected by Bush and Obama will produce social unrest, “in light of

the potential impact of central bank actions in driving

inequality between asset owners and labor."

*

"Overall, the reaction

to the decision points to the underlying fragility of financial markets,

which have become a house of cards as a result of the massive inflows of

money from the Fed and other central banks, and are now extremely

susceptible to even a small tightening in financial conditions."

*

"It is significant that what the Financial Times described

as a “tsunami of money”—estimated to reach $1 trillion for the year—has failed

to prevent what could be the worst year for stock markets since the global

financial crisis."

*

"A

decade ago, as the financial crisis raged, America’s banks were in

ruins. Lehman Brothers, the storied 158-year-old investment house,

collapsed into bankruptcy in mid-September 2008. Six months earlier, Bear

Stearns, its competitor, had required a government-engineered rescue to

avert the same outcome. By October, two of the nation’s largest commercial

banks, Citigroup and Bank of America, needed their own government-tailored

bailouts to escape failure. Smaller but still-sizable banks, such as

Washington Mutual and IndyMac, died."

*

The GOP said the "Tax Cuts and Jobs Act" would reduce

deficits and supercharge the economy (and stocks and wages). The White

House says things are working as planned, but one year

on--the numbers mostly suggest otherwise.

No comments:

Post a Comment