Banks can always rely on the government to bail them out when the house of cards collapses.

With the passage of time, swamp-dwellers

like Eric Holder and Lois Lerner, knee-deep in the mud with congressional contempt

charges, continue to be financially enriched and will slowly be forgotten,

while more recognizable swamp royalty like Hillary Clinton get to run for

president.

Until Americans see

guilty members within the United States

government wearing orange jumpsuits and

serving time, the

investigations and congressional hearings are mere sideshow

spectacles to appease the masses.

So when it was revealed that the financial system was in reality a snake pit of corruption and conflicts of interest, it was a case of all hands on deck to provide the justification for the trillions of dollars made available to the very banks and financial institutions whose activities had sparked the crisis, while hundreds of millions of workers the world over were made to pay through wage cuts and austerity measures.

So when it was revealed that the financial system was in reality a snake pit of corruption and conflicts of interest, it was a case of all hands on deck to provide the justification for the trillions of dollars made available to the very banks and financial institutions whose activities had sparked the crisis, while hundreds of millions of workers the world over were made to pay through wage cuts and austerity measures.

NO PRESIDENT IN HISTORY SUCKED IN

MORE BRIBES FROM CRIMINAL BANKSTERS THAN BARACK OBAMA!

This was not because of

difficulties in securing indictments or convictions. On the contrary, Attorney

General Eric Holder told a Senate committee in March of 2013 that the Obama

administration chose not to prosecute the big banks or their CEOs because to do

so might “have a negative impact on the national economy.”

Bank of England governor tells Jackson Hole conference: Existing financial system will not hold

One of the fictions most assiduously promoted by the ideological representatives of the capitalist economy is that those in charge of monetary and economic policy have a sound knowledge of the system over which they preside and a clear idea of what they are doing. Such operations assume great importance when events, such as the financial crash of 2008, reveal to masses of working people that this is not the case.

The collapse eleven years ago was preceded by assertions as to the “efficiency” of the market. A “great moderation” had been established in which the evils of the past had been finally conquered, with anyone who dared to differ being declared guilty of blasphemy against gods such as Fed chairman Alan Greenspan.

So when it was revealed that the financial system was in reality a snake pit of corruption and conflicts of interest, it was a case of all hands on deck to provide the justification for the trillions of dollars made available to the very banks and financial institutions whose activities had sparked the crisis, while hundreds of millions of workers the world over were made to pay through wage cuts and austerity measures.

The bailouts may have been regrettable, it was argued, but these measures were necessary to prevent something even worse. New regulations were being put in place to prevent a recurrence and after a period of “unconventional” measures—essentially the handout of virtually free money to the “malefactors of great wealth”—things would return to “normal.”

This piece of fiction was exposed at the conference of central bankers and financial experts held at Jackson Hole, Wyoming last week.

Reporting on the meeting, the Financial Times noted “there was a sense that things would never be the same again.” In an interview with the newspaper the president of the St Louis Federal Reserve, James Bullard said there had been a “regime shift” in economic conditions.

Its manifestations are all too apparent. The supply of ultra-cheap money, either through interest rate cuts or the purchases of financial assets by central banks, so-called “quantitative easing,” has failed to provide any significant stimulus to the real economy, inflation continues to remain below the target rate set by central banks of 2 percent and interest rates remain at historic lows.

So persistent is this phenomenon that the financial system has entered a kind of Alice in Wonderland world where some $16 trillion worth of bonds are trading at negative yields, meaning that an investor holding them to maturity would suffer a loss.

“Something is going on,” Bullard told the Financial Times, “and that’s causing a total rethink of central banking and all our cherished notions about what we think we’re doing. We just have to stop thinking that next year things are going back to normal.”

However much they seek to promote the illusion that they are in control, those in charge of the financial system do have to engage in a discussion over the mounting problems they confront and what might be done to alleviate them. And a couple of papers presented at the meeting were significant from that standpoint.

Over the past months, the realisation has begun to grow that trade war is not a passing phase but is now a permanent feature of economic and political life. This is coupled with the recognition that the role of the US dollar as the basis of stability for the financial system is now increasingly being called into question.

Mark Carney, the retiring governor of the Bank of England, told the conference the present international monetary system based on the US “won’t hold” and that a new international monetary system had to be constructed.

He noted that the US accounted for only 10 percent of global trade and 15 percent of global GDP but the dollar formed the basis for half of world trade invoices and two-thirds of global securities issuances. Movements in the dollar, therefore, were of fundamental importance to other economies even if they had few trade links with the US. They were forced to hoard dollars in order to guard against capital flight.

The dollar was just as important as in 1971 when US President Nixon removed it gold backing and ended the Bretton Woods system of fixed currency relations anchored by gold.

At that time US Treasury Secretary John Connally dismissed the concerns of other countries with the dictum “our dollar, your problem.” This had now broadened, Carney said, to “any of our problems is your problem.”

For decades the mainstream view had been that countries could achieve price stability and regulate economic growth by targeting inflation and adopting floating exchanges rates. This consensus was now “increasingly untenable.” This was because US developments now had “significant spillovers onto both the trade performance and the financial conditions of countries even with relatively limited direct exposure to the US economy.”

He said there was little that could be done in the short term and central bankers had to “play the cards they have been dealt as best they can.”

However, in the longer term “we need to change the game.” The international monetary system could not be reformed overnight but equally “blithe acceptance of the status quo is misguided.”

“Risks are building, and they are structural. As [the late economist] Rudi Dornbusch warned, ‘In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.’”

In the medium term he called for the International Monetary Fund to increase its resources and set up a global fund to deal with capital flight. In the longer term there needed to be multipolar global economy and consideration should be given to the establishment of a “synthetic hegemonic currency.” possibly through a network of central bank digital currencies, in order to “dampen the domineering influence of the US dollar on global trade” so that US shocks would not reverberate around the world as they do now.

In essence this is a modern-day version of the proposal advanced by the British representative John Maynard Keynes at the Bretton Woods conference in 1944 for the establishment of a global currency, bancor. At that time, the US asserted its power and insisted that the dollar, backed by gold, had to be the international currency. But since the removal of the gold backing in 1971 as a stable anchor, the global financial system has become increasingly impacted by movements in the US dollar.

“The deficiencies of the international monetary and financial system have become increasingly potent,” Carney concluded and that “even a passing acquaintance with monetary history suggests that this centre won’t hold.”

Similar warnings of financial instability were given in another paper presented by Stanford University economists Arvind Krishnamurthy and Hanno Lustig who pointed to the role played by dollar-denominated investments in providing global investors with safe assets.

They recalled the warnings by economist Robert Triffin in 1960 about the essential contradiction at the heart of the Bretton Woods system. Triffin pointed out that the expansion of global trade and finance depended on the continual outflow of US dollars. But this meant that this pool of dollars would outgrow the gold backing that was its anchor, leading to a crisis. That crisis erupted when Nixon ended dollar-gold convertibility.

The authors noted that Triffin’s logic could be extended to the current situation. “The supply of safe dollar assets is no longer backed by gold; however, the supply is fueled by increases in public and private leverage. Will dollar leverage be supplied in a manner consistent with financial stability? The events of the last 15 years suggest that policy makers should pay close attention to this question.”

BANKS RAN THIS COUNTRY AND RAN

IT INTO THE GROUND FOR MORE THAN A CENTURY.

“The Federal Reserve is

a key mechanism for perpetuating this whole filthy system,

in which “Wall Street rules.” But its services in behalf

of the rich and the super-rich only compound the fundamental

and insoluble contradictions of capitalism, plunging the system

into ever deeper debt and ensuring that the next crisis will be

that much more violent and explosive.”

“Hundreds of thousands

of federal workers remain furloughed or forced to work without pay as the

partial government shutdown enters its third week, but the US central bank is

making clear that all of the resources of the state are at the disposal of the

financial oligarchy.”

“A decade ago, as the

financial crisis raged, America’s banks were in ruins. Lehman Brothers, the

storied 158-year-old investment house, collapsed into bankruptcy in

mid-September 2008. Six months earlier, Bear Stearns, its competitor, had

required a government-engineered rescue to avert the same outcome. By October,

two of the nation’s largest commercial banks, Citigroup and Bank of America,

needed their own government-tailored bailouts to escape failure. Smaller but

still-sizable banks, such as Washington Mutual and IndyMac, died.”

NICOLE GELINAS

Bank Money: ‘The Root of

All Evil’

Waste and corruption are the result of banks' privilege to create

money out of nothing

The one force that causes the most harm in

our economy also happens to be the least well-known and understood.

While the left blames greedy corporations

and individuals, and the right blames the government, it is in fact the

collusion between the government and private banks that leads to problems

like environmental degradation, unemployment, income inequality, and many more.

In the United States and most other

countries, the government grants private banks the right to create money out of

nothing and forces individuals to accept said money as legal tender and to use

it to pay their taxes.

The Coinage Act of 1965 states, “United States coins and

currency (including Federal reserve notes and circulating notes of Federal

reserve banks and national banks) are legal tender for all debts, public

charges, taxes, and dues.”

Today, the “notes” are mostly electronic

credits in the form of bank deposits, but the same law applies. So much for

legal tender—what about creating money out of nothing? Don’t banks take savers’

deposits and then loan them out to borrowers?

The short answer is no. Instead of taking

in savings from companies and individuals, then waiting for a suitable

borrower, banks use a simple accounting trick to create new money whenever

someone applies for a loan.

Let’s assume you apply for a mortgage of

$450,000. Once it’s approved, the bank simply credits your account with

$450,000 in the form of a deposit, which you can then use to spend on your

house. This is the bank’s liability. On the bank’s asset side, it credits

itself with a loan of $450,000 to you, which you will pay back over the course

of 30 or so years, plus interest.

For this process, no savings are necessary.

The only thing the bank has to do from a regulatory perspective is keep a very

low fraction of its assets in cash or balances at the Federal Reserve (Fed), so

it can pay out some cash on demand if needed. This is often not more than 1

percent of its assets, hence the term “fractional reserve” banking.

The Root

The popular saying has it that money is the

root of all evil. However, the original quote from the Bible would be more

accurately applied to the process described above, wherein banks are allowed to

create money out of nothing and charge you interest for the trouble: “for

the love of money

is the root of all evil.”

Money itself, of course, cannot be evil. It

merely measures the value of goods and services produced and the value of

capital saved. However, under the bank money monopoly, the new money created

doesn’t measure production and savings, but actually changes them.

The creation of “money,” in the form of the

loan and deposit, required nothing to be produced and nothing to be saved. The

production only begins later, when the contractors start building the

house—although even that is not guaranteed, given that many mortgages or other

loans are used to buy up existing assets, which drives up prices.

Even loans that finance new construction

alter the economy in unnatural ways: bankers’ prejudice directs production

instead of consumer demand from their own savings. And the bank, which can

repossess the collateral unless the loan is repaid, gets something for nothing.

The principle at work here is pure love of

money—nothing more. The bank does not need to expend any effort but can “earn”

the interest on the loan, which is the same as a private tax on the money

supply. It is the equivalent of a few designated individuals being allowed to

keep a money press at home, which they could then use to print cash, make

loans, and charge interest against. Meanwhile, everyone else is forced to use

those printed loans to make investments. Clearly, this is not fair.

The Problem

The ease with which banks can create money

explains the recurring colossal blunders in risk management and loan creation,

of which the subprime crisis is only the most recent manifestation. Because

money is free, it makes sense for banks to loan out as much as possible. After

all, they don’t have to do anything to source the funds, but get to reap the

interest payments as the loans are repaid.

If the market for money were not completely

cartelized by the government for the banks, even this perverse mechanism would

have its limit, and would ultimately lead to the demise of the participating

banks—just as what played out in the 2008 crisis.

However, because banks, regarded as too big

to fail, collude with the government and sponsor politicians with campaign

contributions, they can always rely on the government to bail them out when the

house of cards collapses. This is not a problem of too little regulation, but

instead of the wrong kind of regulations, perpetrating a systematic theft of

public resources.

Banks

can always rely on the government to bail them out when the house of cards collapses.

Even this is just the tip of the iceberg.

Because the capital allocation process in this system is so flawed, the private

sector is encouraged to spend funds on inefficient and unnecessary vanity

projects—real estate is the most obvious, along with massive industrial

overcapacity.

Because big corporations have better access

to big banks, they have better access to this artificial “capital,” and they

can therefore crowd out smaller players that may be able to service their

communities better. Too much real estate development and industrial

overcapacity also put the most strain on environmental resources.

The process leads to the centralization and

bureaucratization of everything, not just the government. Big corporations,

paying lower interest charges than their smaller competitors, end up providing

the majority of goods and services. This is why we see the same brands and

chains everywhere.

Because the money supply “tax” needs to be

paid to private banks, corporations are constantly looking for ways to cut

costs, which often means firing people and replacing them with robots.

Workers and ordinary consumers, on the

other hand, get trapped. They have no choice but to meet high interest payments

on credit card loans and mortgages, while the prices of goods, and anything

they might invest in, shoot through the roof.

The Solution

Of course, it doesn’t have to be this way.

If banks did not have the privilege of creating money out of nothing, and

instead had to source their loans from real savings, their incentives would

change immediately. It would also help if there were no government bailouts.

In that case, investment would equal real

savings and would by definition be limited, because savings require a reduction

in consumption. This is harder to achieve than simply printing money. Resources

would, therefore, be economized. Opportunities for accumulating extravagant

wealth, while still present, would also be reduced, and there would be a

natural tendency toward a more even wealth distribution—not one engineered by a

centralized bureaucracy.

Honest

banking and honest money have existed before in history.

If banks and borrowers had skin in the

game, capital allocation decisions would be examined not according to the “love

for money” principle, but rather according to how productive the investment

would be.

More productivity means producing more with

less, thus saving natural resources. Less capital investment would mean more

room for humans to participate in the economic process. Prices for capital and

goods would be more stable.

This is not a dream, nor a vision of

Utopia. Honest banking and honest money have existed before in history. The

first step to solving this problem is to become aware of the problem.

This article is part of a special Epoch Times

series on the Federal Reserve. Click here to see all articles.

Views expressed in this article are the

opinions of the author and do not necessarily reflect the views of The Epoch

Times.

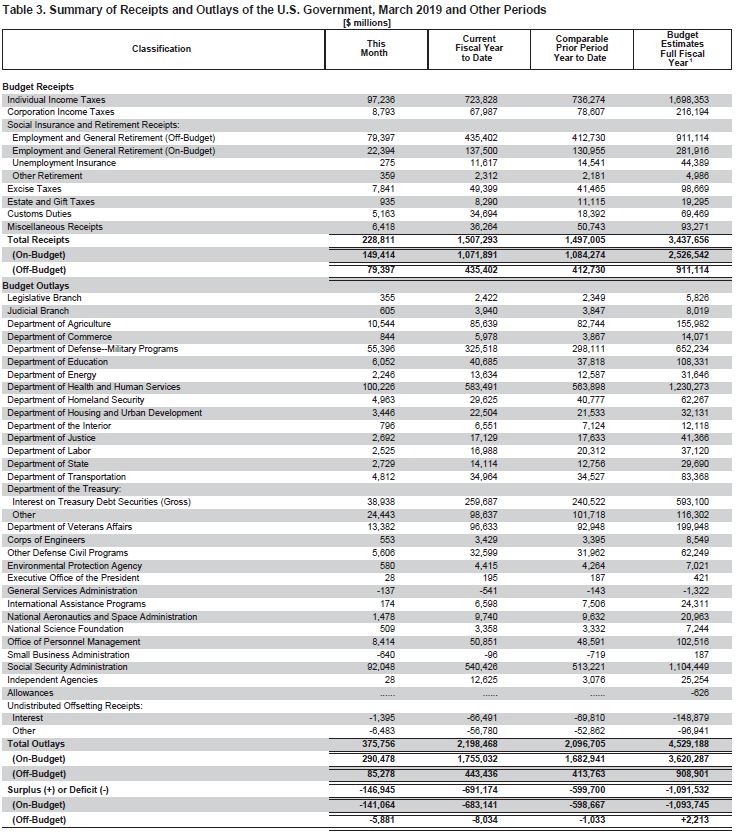

$2,198,468,000,000:

Federal Spending Hit 10-Year High Through March; Taxes Hit 5-Year Low

(Getty Images/Ron Sachs-Pool)

(CNSNews.com) - The federal government spent $2,198,468,000,000

in the first six months of fiscal 2019 (October through March), which is the

most it has spent in the first six months of any fiscal year in the last

decade, according

to the Monthly Treasury Statements.

The last time the government spent more in the

October-through-March period was in fiscal 2009, when it spent

$2,326,360,180,000 in constant March 2019 dollars.

Fiscal 2009 was the fiscal year that

began with President George W. Bush

signing a $700-billion law to bailout

the banking industry in October 2008

and then saw President Barack Obama

sign a $787-billion stimulus law in

February 2009.

began with President George W. Bush

signing a $700-billion law to bailout

the banking industry in October 2008

and then saw President Barack Obama

sign a $787-billion stimulus law in

February 2009.

At the same time that the Treasury was spending the most it has

spent in ten years, it was also taking in less in tax revenue than it has in

the past five years.

{kind=link}

In the October-through-March period, the Treasury collected $1,507,293,000,000

in total taxes. The last time it collected less than that in the first six

months of any fiscal year was fiscal 2014, when it collected $1,420,897,880,000

in constant March 2019 dollars.

The difference in the federal taxes taken in and the spending

going out resulted in a federal deficit of $691,174,000,000 for the first six

months of the fiscal year.

During those six months, the Department of Health and Human

Services spent the most money of any federal agency with outlays of $583.491 billion.

The Social Security Administration was second, spending $540.426 billion. The

Department of Defense was third, spending $325.518 billion. Interest on

Treasury securities was third, coming in at $259.687 for the six-month period.

Both individual and corporation income taxes were down in the

first six months of this fiscal year compared to last year. In the first six

months of fiscal 2018, the Treasury collected $736,274,000,000 in individual

income taxes (in constant March 2019 dollars). In the first six months of this

fiscal year, it collected $723,828,000,000.

In the first six months of fiscal 2018, the Treasury collected

$80,071,070,000 in corporation income taxes (in constant March 2019 dollars).

In the first six months of this fiscal year, it collected $67,987,000,000.

(Historical budget numbers in this story were adjusted to March

2019 dollars using the Bureau of Labor Statistics inflation calculator.)

(Table 3 from the Monthly

Treasury Statement,

seen below, summarizing federal receipts and outlaws for the past month and for

the fiscal year to date and compares it to the previous fiscal year.)

{kind=link}

After Lehman's Collapse: A

Decade of Delay

Now that the 2018

midterms are over, folks can address the elephant in the room. If one tuned

into Fox Business midday on January 7, one heard legendary corporate raider

Carl Icahn dilate on the dimensions of the pachyderm, which he pegged at $250

trillion. That’s the size of worldwide debt. But can that be right -- it’s

more than eleven times the official U.S. federal government’s debt? And in case

you didn’t notice, it is a quarter of one quadrillion bucks. Pretty soon we’ll

be talking real money.

Icahn’s $250T quotation

for worldwide debt came out last year. On September 13, Bloomberg ran

“$250 Trillion in Debt: the World’s

Post-Lehman Legacy” by Brian Chappatta, who draws off data from the Institute of International Finance’s July 9 “Global Debt

Monitor,” (to read IIF reports, one must sign up). Chappatta wonders how the

world’s central bankers can “even pretend to know how to reverse what they’ve

done over the past decade”:

[Central banks] kept

interest rates at or below zero for an extended period […] and used bond-buying

programs to further suppress sovereign yields, punishing savers and promoting

consumption and risk-taking. Global debt has ballooned over the past two

decades: from $84 trillion at the turn of the century, to $173 trillion at the

time of the 2008 financial crisis, to $250 trillion a decade after Lehman

Brothers Holdings Inc.’s collapse.

Chappatta breaks global

debt down into four categories: financial corporations, nonfinancial

corporations, households, and governments. In every category, global nominal

debt rose from 2008 to 2018, with the debt of governments hitting $67T. In the

important debt-as-a-percentage-of-gross-domestic-product measurement, three of

the categories rose while only financial corporations fell, “leaving their

debt-to-GDP ratio as low as it has been in recent memory.” Global banks seem to

be “healthier and more resilient to another shock.” After reporting on

worldwide debt, Chappatta then looks at U.S. debt.

What’s interesting about

debt in America is that as a percentage of GDP, households and financial

corporations have sharply reduced their debt. It is only government in America

that has seen a sharp debt-to-GDP uptick, and it was quoted at more than 100

percent of GDP. That’s rather higher than for all government debt worldwide.

Besides the massive

racking up of debt over the last decade there’s something else that should

concern us: the massive creation of new money. One of the ways money is created

is when central banks engage in the “bond-buying programs” that Chappatta

refers to. We call such programs “quantitative easing.” When the Federal

Reserve buys assets, like treasuries and mortgage-backed securities, it needs

money. So the Fed just creates the money ex nihilo.

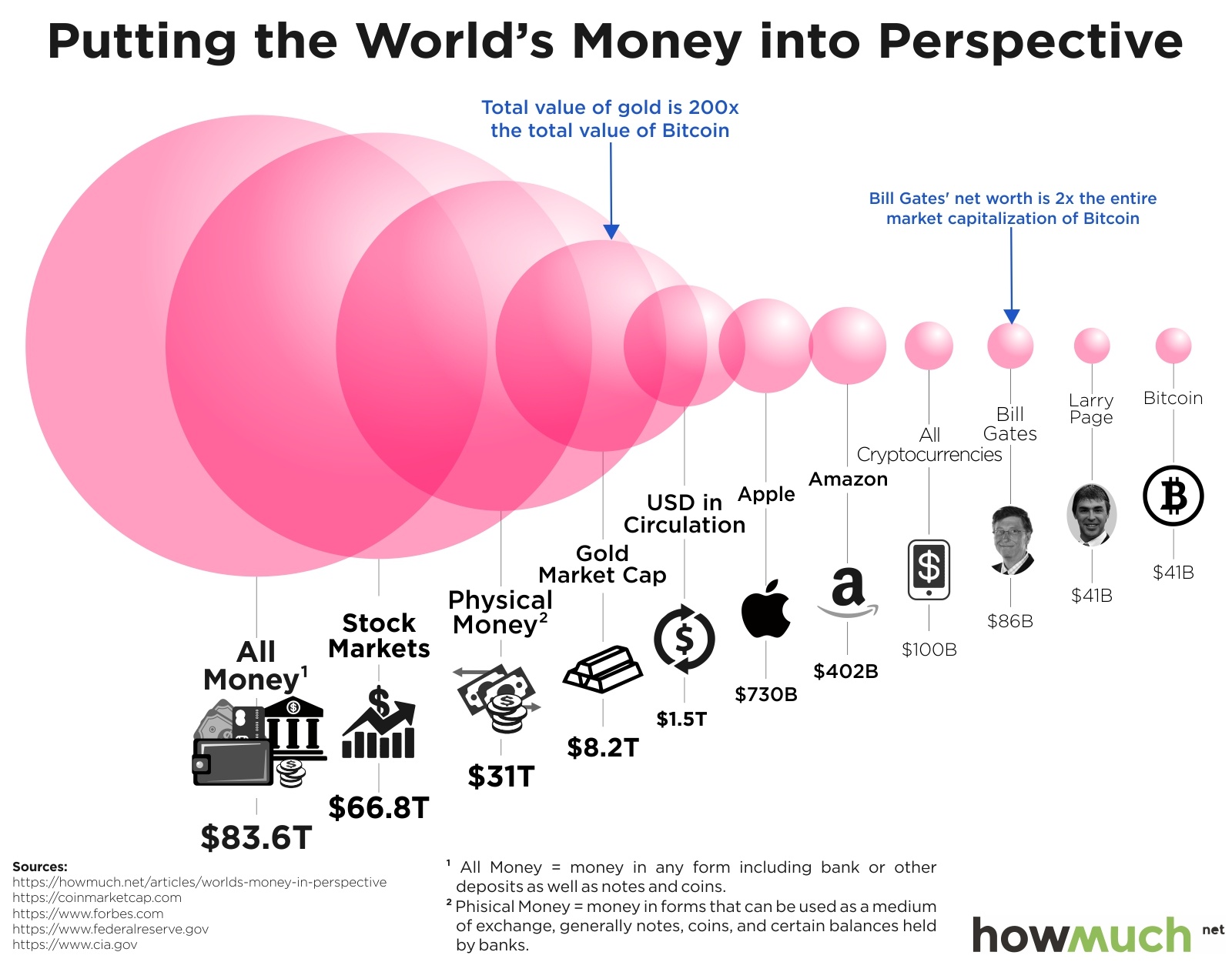

Since the U.S. isn’t the

only nation that has been busy buying bonds and creating money, one might

wonder just how much money there is in the world. In June of 2017,HowMuch put

out “Putting the World’s Money into

Perspective,” which is a nice little graphic that puts the category “All

Money” at $83.6T.

{kind=link}

In November of

2017, MarketWatch ran “Here’s all the money in the world, in

one chart”

by Sue Chang, who in her short intro to the chart has some interesting things

to say about global money, including cryptocurrencies. She writes of “narrow

money” and “broad money” and pegs the latter at

$90.4T, (or what Sen. Everett Dirksen would call “real money”.) If you want to

examine Chang’s chart more closely, I’ve “excised” it here for your

convenience; don’t miss the notes on the right margin. (Because its depth is

13,895 pixels, you might want to just save the chart to your computer rather

than print it off.)

{kind=link}

So, in addition to an

historic run-up in debt, there’s been a monster amount of new money created.

Chappatta calls it the “grandest central-bank experiment in history.” His use

of “experiment” is apropos, as one wonders whether the world’s central bankers and

their economists really know what they’ve been doing.

One ray of hope might

just be President Trump’s choice of Jerome Powell as Chairman of the Federal

Reserve, (Trump has such good instincts about people). One can get a sense of

the man from his January talk with David Rubenstein at the Economic Club of

Washington, D.C. (video and transcript). It’s refreshing that

Mr. Powell disdains the “Fed speak” used by his predecessors.

Chappatta’s article is

quite worth reading, and it’s not very long. The charts are user-friendly,

although animated ones are a bit “creative.” The last section, “China Charges

Forward,” is especially worthwhile.

This is the post-Lehman

legacy. To pull the global economy back from the brink, governments borrowed

heavily from the future. That either portends pain ahead, through austerity

measures or tax increases, or it signals that central-bank meddling will become

a permanent fixture of 21st century financial markets.

Given those

alternatives, let’s try a little austerity. But austerity would entail spending

cuts, and Congress has a poor history in that regard. In fact, since fiscal

2007, the year before the financial crisis, total federal spending has gone

from $2.72T a year to more than $4T. While austere citizens deleverage and get

their fiscal affairs in order, Congress shamefully borrows and spends like

never before.

Congress’ solutions are

to bail out, prop up, and do whatever it takes to avoid reforming what it has

created. So they farm out their responsibilities to the Federal Reserve.

Indeed, in the July 17, 2012 meeting of the Senate Banking Committee (go

to the 53:50 point of this C-SPAN video), Chuck Schumer told

Federal Reserve Chairman Ben Bernanke the following:

So given the political

realities, Mr. Chairman, particularly in this election year, I'm afraid the Fed

is the only game in town. And I would urge you to take whatever actions you

think would be most helpful in supporting a stronger economic recovery… So get

to work, Mr. Chairman. (Chuckles.)

So the Fed is “the only

game in town” because there are only monetary solutions for the economy, right?

There aren’t any fiscal solutions, as they would involve Congress, and Congress

is busy running for re-election, right? Sounds like you’re abdicating your

responsibilities, Chuck.

"The Federal Reserve is a key mechanism for

perpetuating this whole filthy system, in

which "Wall Street rules."

Wall Street rules

The Federal Reserve

sent a clear message to Wall Street on Friday: It will not allow the longest

bull market in American history to end. The message was received loud and

clear, and the Dow rose by more than 700 points.

Responding to Thursday’s

market selloff following a dismal report from Apple and signs of a

manufacturing slowdown in both China and the US, the Fed declared it was

“listening” to the markets and would scrap its plans to raise interest rates.

Speaking at a

conference in Atlanta, where he was flanked by his predecessors Ben Bernanke

and Janet Yellen, both of whom had worked to reflate the stock market bubble

after the 2008 financial crash, Chairman Jerome Powell signaled that the Fed

would back off from its two projected rate increases for 2019.

“We’re listening

sensitively to the messages markets are sending,” he said, adding that the

central bank would be “patient” in imposing further rate increases. To

underline the point, he declared, “If we ever came to the conclusion that any

aspect of our plans” was causing a problem, “we wouldn’t hesitate to change

it.”

This extraordinary

pledge to Wall Street followed the 660 point plunge in the Dow Jones Industrial

Average on Thursday, capping off the worst two-day start for a new trading year

since the collapse of the dot.com bubble.

William McChesney

Martin, the Fed chairman from 1951 to 1970, famously said that his job was “to

take away the punch bowl just as the party gets going.” Now the task of the Fed

chairman is to ply the wealthy revelers with tequila shots as soon as they

start to sober up.

Powell’s remarks were

particularly striking given that they followed the release Friday of the most

upbeat jobs report in over a year, with figures, including the highest

year-on-year wage growth since the 2008 crisis, universally lauded as

“stellar.”

While US financial

markets have endured the worst December since the Great

Depression, amid mounting fears of a looming recession and a new

financial crisis, analysts have been quick to point out that there are no

“hard” signs of a recession in the United States.

Both the Dow and the

S&P 500 indexes have fallen more than 15 percent from their recent highs,

while the tech-heavy NASDAQ has entered bear market territory, usually defined

as a drop of 20 percent from recent highs.

The markets, Powell

admitted, are “well ahead of the data.” But it is the markets, not the “data,”

that Powell is listening to.

Since World War II,

bear markets have occurred, on average, every five-and-a-half years. But if the

present trend continues, the Dow will reach 10 years without a bear market in

March, despite the recent losses.

Now the Fed has stepped

in effectively to pledge that it will

allocate whatever

resources are needed to ensure that no

substantial market

correction takes place. But this means only that when the

correction does come, as it inevitably must, it will be all the more

severe and the Fed will have all the less power to stop it.

From the standpoint of

the history of the institution, the Fed’s current more or less explicit role as

backstop for the stock market is a relatively new development. Founded in 1913,

the Federal Reserve legally has had the “dual mandate” of ensuring both maximum

employment and price stability since the late 1970s. Fed officials have

traditionally denied being influenced in policy decisions by a desire to drive

up the stock market.

Federal Reserve

Chairman Paul Volcker, appointed by Democratic President Jimmy Carter in 1979,

deliberately engineered an economic recession by driving the benchmark federal

funds interest rate above 20 percent. His highly conscious aim, in the name of

combating inflation, was to quash a wages movement of US workers by triggering

plant closures and driving up unemployment.

The actions of the Fed

under Volcker set the stage for a vast upward redistribution of wealth,

facilitated on one hand by the trade unions’ suppression of the class struggle

and on the other by a relentless and dizzying rise on the stock market.

Volcker’s recession,

together with the Reagan administration’s crushing of the 1981 PATCO air

traffic controllers’ strike, ushered in decades of mass layoffs,

deindustrialization and wage and benefit concessions, leading labor’s share of

total national income to fall year after year.

These were also decades

of financial deregulation, leading to the savings and loan crisis of the late

1980s, the dot.com bubble of 1999-2000, and, worst of all, the 2008 financial

crisis.

In each of these

crises, the Federal Reserve carried out what became known as the “Greenspan

put,” (later the “Bernanke put”)—an implicit guarantee to backstop the

financial markets, prompting investors to take ever greater risks.

Since that time, the Federal Reserve has carried out its

most accommodative monetary policy ever, keeping interest rates at or near zero

percent for six years. It supplemented this boondoggle for the financial elite

with its multi-trillion-dollar “quantitative easing” money-printing program.

The effect can be seen in the ever more staggering wealth

of the financial oligarchy, which has consistently enjoyed investment returns

of between 10 and 20 percent every year since the financial crisis, even as the

incomes of workers have stagnated or fallen.

American capitalist

society is hooked on the toxic growth of social inequality created by the stock

market bubble. This, in turn, fosters the political framework not just for the

decadent lifestyles of the financial oligarchs, each of whom owns, on average,

a half-dozen mansions around the world, a private jet and a super-yacht, but

also for the broader periphery of the affluent upper-middle class, which

provides the oligarchs with political legitimacy and support. These elite

social layers determine American political life, from which the broad mass of

working people is effectively excluded.

In this intensifying

crisis, the working class must assert its independent interests with the same

determination and ruthlessness as evinced by the ruling class. It must answer

the bourgeoisie’s social counterrevolution with the program of socialist

revolution.

the depression is already

here for most of us below the super-rich!

Trump and the GOP created a fake economic boom on

our collective credit card: The equivalent of maxing out your credit

cards and saying look how good I'm doing right now.

*

Trump criticized

Dimon in

2013 for supposedly contributing to the country’s economic

downturn. “I’m not Jamie Dimon, who pays $13 billion to settle a case

and then pays $11 billion to settle a case and who I think is the worst

banker in the United States,” he told reporters.

*

"One

of the premier institutions of big business, JP Morgan Chase, issued

an internal report on the eve of the 10th anniversary of the 2008

crash, which warned that another “great liquidity crisis”

was possible, and that a government bailout on the scale of that

effected by Bush and Obama will produce social unrest, “in light of

the potential impact of central bank actions in driving

inequality between asset owners and labor."

*

"Overall,

the reaction to the decision points to the underlying fragility of

financial markets, which have become a house of cards as a result of the

massive inflows of money from the Fed and other central banks, and are now

extremely susceptible to even a small tightening in financial

conditions."

*

"It

is significant that what the Financial

Times described as a “tsunami of money”—estimated to reach $1

trillion for the year—has failed to prevent what could be the worst year for

stock markets since the global financial crisis."

*

"A decade ago, as the financial

crisis raged, America’s banks were in ruins. Lehman Brothers, the storied

158-year-old investment house, collapsed into bankruptcy in mid-September

2008. Six months earlier, Bear Stearns, its competitor, had required a

government-engineered rescue to avert the same outcome. By October, two of

the nation’s largest commercial banks, Citigroup and Bank of America,

needed their own government-tailored bailouts to escape failure. Smaller

but still-sizable banks, such as Washington Mutual and IndyMac,

died."

*

The

GOP said the "Tax Cuts and Jobs Act" would reduce deficits and

supercharge the economy (and stocks and wages). The White House says

things are working as planned, but one year on--the numbers mostly

suggest otherwise.

FROM THE MAGAZINE

Finance’s Lengthening Shadow

The growth of nonbank lending

poses an increasing risk.

Economy, finance, and

budgets

CITY JOURNAL

A decade ago, as the financial crisis raged, America’s banks were in ruins. Lehman Brothers, the storied 158-year-old investment house, collapsed into bankruptcy in mid-September 2008. Six months earlier, Bear Stearns, its competitor, had required a government-engineered rescue to avert the same outcome. By October, two of the nation’s largest commercial banks, Citigroup and Bank of America, needed their own government-tailored bailouts to escape failure. Smaller but still-sizable banks, such as Washington Mutual and IndyMac, died.

After the

crisis, the goal was to make banks safer. The 2010 Dodd-Frank law, coupled with

independent regulatory initiatives led by the Federal Reserve and other bank

overseers, severely tightened banks’ ability to engage in speculative ventures,

such as investing directly in hedge funds or buying and selling securities for

short-term gain. The new regime made them hold more reserves, too, to backstop

lending.

Yet the

financial system isn’t just banks. Over the last ten years, a plethora of

“nonbank” lenders, or “shadow banks”—ranging from publicly traded investment

funds that purchase debt to private-equity firms loaning to companies for

mergers or expansions—have expanded their presence in the financial system, and

thus in the U.S. and global economies. Banks may have tighter lending standards

today, but many of these other entities loosened them up. One consequence:

despite a supposed crackdown on risky finance, American and global debt has

climbed to an all-time high.

Banks

remain hugely important, of course, but the potential for a sudden, 2008-like

seizure in global credit markets increasingly lies beyond traditional banking.

In 2008, government officials at least knew which institutions to rescue to

avoid global economic paralysis. Next time, they may be chasing shadows.

The 2008 financial crisis vaporized 8.8 million American jobs,

triggered 8 million house foreclosures, and still roils global politics. Many

commentators blamed a proliferation of complex financial instruments as the

primary reason for the meltdown. Notoriously, financiers had taken subprime

“teaser”-rate mortgages and other low-quality loans and bundled them into

opaque financial securities, such as “collateralized debt obligations,” which

proved exceedingly hard for even sophisticated investors, such as the overseas

banks that purchased many of them, to understand. When it turned out that some

of the securities contained lots of defaulting loans—as Americans who never

were financially secure enough to purchase homes struggled to pay housing

debt—no one could figure out where, exactly, the bad debt was buried (many

places, it turned out). Global panic ensued.

The

“shadow-financing” industry played a role in the crisis, too. Many nonbank

mortgage lenders had sold these bundled loans to banks, so as to make yet more

bundled loans. But the locus of the 2008 crisis was traditional banks. Firms

such as Citibank and Lehman had kept tens of billions of dollars of such debt

and related derivative instruments on their books, and investors feared

(correctly, in Lehman’s case) that future losses from these soured loans would

force the institutions themselves into default, wiping out shareholders and

costing bondholders money.

The

ultimate cause of the crisis, however, wasn’t complex at all: a massive

increase in debt, with too little capital behind it. Recall how a bank works.

Like people, banks have assets and liabilities. For a person, a house or

retirement account is an asset and the money he owes is a liability. A bank’s

assets include the loans that it has made to customers—whether directly, in a

mortgage, or indirectly, in purchasing a mortgage-backed bond. Loans and bonds

are bank assets because, when all goes well, the bank collects money from them:

the interest and principal that borrowers pay monthly on their mortgage, for

example. A bank’s liabilities, by contrast, include the money it has borrowed

from outside investors and depositors. When a customer keeps his money in the

bank for safekeeping, he effectively lends it money; global investors who

purchase a bank’s bonds are also lending to it. The goal, for firms as well as

people, is for the worth of assets to exceed liabilities. A bank charges higher

interest rates on the loans that it makes than the rates it pays to depositors

and investors, so that it can turn a profit—again, when all goes well.

When the

economy tanks, this system runs into two problems. First, a bank’s asset values

start to fall as more people find themselves unable to pay off their mortgage

or credit-card debt. Yet the bank still must repay its own debt. If the value

of a bank’s assets sinks below its liabilities, the bank is effectively

insolvent. To lessen this risk, regulators demand that banks hold some money in

reserve: capital. Theoretically, a bank with capital equal to 10 percent of its

assets could watch those assets decline in value by 10 percent without

insolvency looming.

Yet

investors would frown on such a thin margin, and that highlights the second

problem: illiquidity. A bank might have sufficient capital to cover its losses,

but if depositors and other lenders don’t agree, they may rush to take their

money out—money that the bank can’t immediately provide because it has locked

up the funds in long-term loans, including mortgages. During a liquidity “run,”

solvent banks can turn to the Federal Reserve for emergency funding.

By 2008,

bank capital levels had sunk to an all-time low; bank managers and their

regulators, believing that risk could be perfectly monitored and controlled,

were comfortable with the trend. By 2007, banks’ “leverage ratio”—the

percentage of quality capital relative to their assets—was just 6 percent, well

below the nearly 8 percent of a decade earlier. Since then, thanks to tougher

rules, the leverage ratio has risen above 9 percent. Global capital ratios have

risen, as well. Many analysts believe that capital requirements should be

higher still, but the shift has made banks somewhat safer.

The

government doesn’t mandate capital levels with the goal of keeping any

particular bank safe. After all, private companies go out of business all the

time, and investors in any private venture should be prepared to take that

risk. The capital requirements are about keeping the economy safe. Banks tend to hold similar assets—various types of

loans to people, businesses, or government. So when one bank gets into trouble,

chances are that many others are suffering as well. A higher capital reserve

lessens the chance of several banks veering toward insolvency simultaneously,

which would drain the economy of credit. It was that threat—an abrupt shutdown

of markets for all lending, to good borrowers and bad—that led Washington to

bail out the financial industry (mostly the banks) in 2008.

But what if the financial industry, in creating credit, bypasses

the banks? According to the global central banks and regulators who make up the

international Financial Stability Board, this type of lending constitutes

“shadow banking.” That’s an imprecise, overly ominous term, evoking Mafia dons

writing loans to gamblers on betting slips and then kneecapping debtors who

don’t pay the money back on time, but the practice is nothing so Tony

Soprano-ish. The accountancy and consultancy firm Deloitte defines shadow

banking, wonkily, as “a market-funded credit intermediation system involving

maturity and/or liquidity transformation through securitization and

secured-funding mechanisms. It exists at least partly outside of the

traditional banking system and does not have government guarantees in the form

of insurance or access to the central bank.”

“Shadow banking is nothing new, encompassing everything from

corporate bond markets to payday lending.”

In plain

English, “maturity and/or liquidity transformation” is exactly what a bank

does: making a long-term loan, such as a mortgage, but funding it with

short-term deposits or short-term bonds. Outside of a bank, the activity

involves taking a mortgage or other kind of longer-term loan, bundling it with

other loans, and selling it to investors—including pension funds, insurers, or

corporations with large amounts of idle cash, like Apple—as securities that

mature far more quickly than the loans they contain. The risks here are the

same as at the banks, but with a twist: if people and companies can’t pay off

the loans on the schedule that the lenders anticipated, all the investors risk

losing money. Unlike small depositors at banks, shadow banks don’t have

recourse to government deposit insurance. Nor can shadow-financing participants

go to the Federal Reserve for emergency funding during a crisis—though, in many

cases, they wouldn’t have to: pensioners and insurance policyholders generally

don’t have the right to remove their money from pension funds and insurers

overnight, as many bank investors do.

Understood

broadly, shadow banking is nothing new, encompassing everything from corporate

bond markets to payday lending. And much of it isn’t very shadowy; as a recent

U.S. Treasury report noted, the government “prefers to transition to a

different term, ‘market-based finance,’ ” because applying the term “shadow

banking” to entities like insurance companies could “imply insufficient

regulatory oversight,” when some such sectors (though not all) are highly

regulated. It isn’t always easy to separate real banks from shadow banks,

moreover. Just as before the financial crisis, banks continue to offer shadow

investments, such as mortgage-backed securities or bundled corporate loans,

and, conversely, banks also lend money to private-equity funds and other shadow

lenders, so that they, in turn, can lend to companies.

Such

market-based finance has its merits; sound reasons exist for why a pension-fund

administrator doesn’t just deposit tens of billions of dollars at the bank,

withdrawing the money over time to meet retirees’ needs. For people and

institutions willing, and able, to take on more risk, market-based finance can

offer higher interest rates—an especially important consideration when the

government keeps official interest rates close to zero, as it did from 2008 to

2016. Shadow finance also offers competition for companies, people, and

governments unable to borrow from banks cheaply, or whose needs—say, a

multi-hundred-billion-dollar bond to buy another company—would be beyond the

prudent coverage capacity of a single bank or even a group of banks.

Theoretically,

bond markets and other market-based finance instruments make the financial

system safer by diversifying risk. A bank holding a large concentration of

loans to one company faces a major default risk. Dispersing that risk to dozens

or hundreds of buyers in the global marketplace means—again, in theory—that in

a default, lots of people and institutions will suffer a little pain, rather

than one bank suffering a lot of pain.

But too much of a good thing is sometimes not so good, and, in this

case, the extension of shadow banking threatens to reintroduce the risks that

innovation was supposed to reduce. Recent growth in shadow banking isn’t

serving to disperse risk or to tailor innovative products to meet borrowers’

needs. Two less promising reasons explain its expansion. One is to enable

borrowers and lenders to skirt the rules—capital cushions—that constrain

lending at banks. The other—after a decade of record-low, near-zero interest

rates as Federal Reserve policy—is to allow borrowers and lenders to find

investments that pay higher returns.

The world

of market-based finance has indeed grown. Between 2002 and 2007, the eve of the

financial crisis, the world’s nonbank financial assets increased from $30

trillion to $60 trillion, or 124 percent of GDP. Now these assets, at $160

trillion, constitute 148 percent of GDP. Back then, such assets made up about a

quarter of the world’s financial assets; today, they account for nearly half

(48 percent), reports the Financial Stability Board (FSB).

Within

this pool of nonbank assets, the FSB has devised a “narrower” measure of shadow

banking that identifies the types of companies likely to pose the most systemic

risk to the economy—those most susceptible, that is, to sudden, bank-like

liquidity or solvency panics. The FSB believes that pension funds and insurance

companies could largely withstand short-term market downturns, so it doesn’t

include them in this riskier category. That leaves $45 trillion in narrow

shadow institutions and investments, a full 72 percent of it held in

instruments “with features that make them susceptible to runs.” That’s up from

$28 trillion in 2010—or from 66 percent to 73 percent of GDP.

Of that

$45 trillion market, the U.S. has the largest portion: $14 trillion. (Though,

as the FSB explains, separation by jurisdiction may be misleading; Chinese

investment vehicles, for example, have sold hundreds of billions of dollars in

credit products to local investors to spend on property abroad, affecting

Western asset prices.) Compared with this $14 trillion figure, American commercial

banks’ assets are worth just shy of $17 trillion, up from about $12 trillion

right before the financial crisis. Banks as well as nonbank lenders have grown,

in other words, but the banks have done so under far stricter oversight.

An analysis of one particular area of shadow financing shows the

potential for a new type of chaos. A decade ago, an “exchange-traded fund,” or

ETF, was mostly a vehicle to help people and institutions invest in stocks. An

investor wanting to invest in a stock portfolio but without enough resources to

buy, say, 100 shares apiece in several different companies, could purchase

shares in an ETF that made such investments. These stock-backed ETFs carried

risk, of course: if the stock market went down, the value of the ETF tracking

the stocks would go down, too. But an investor likely could sell the fund

quickly; the ETF was liquid because the underlying stocks were liquid.

Over the

past decade, though, a new creature has emerged: bond-based ETFs. A bond ETF

works the same way as a stock ETF: an investor interested in purchasing debt

securities but without the financial resources to buy individual bonds—usually

requiring several thousand dollars of outlay at once—can purchase shares in a

fund that invests in these bonds. Since 2005, bond ETFs have grown from

negligible to a market just shy of $800 billion—nearly 10 percent of the value

of the U.S. corporate bond market.

These

bond ETFs are riskier, in at least one way, than stock ETFs. Some bond ETFs, of

course, invest solely in high-quality federal, municipal, and corporate

debt—bonds highly unlikely to default in droves. Default, though, isn’t the

only risk: suddenly higher global interest rates could cause bond funds to lose

value (as new bonds, with the higher interest rates, would be more attractive).

And with the exception of federal-government debt, even the highest-quality

bonds aren’t as liquid as stocks; they have maturities ranging anywhere from

hours remaining to 100 years.

Investors

in bond-based ETFs, then, face a much bigger “liquidity” and “maturity”

mismatch risk. If the investors want to sell their ETF shares in a hurry, the

fund managers might not be able to sell the underlying bonds quickly to repay

them, particularly in a tense market. That’s especially true, since bond

markets are even less liquid than they were pre–financial crisis. Because of

new regulations on “market making,” banks will be highly unlikely to buy bonds

in a declining market to make a buck later, after the panic subsides.

Alook at a related type of debt-based ETF raises even bigger

mismatch concerns. “In 2017, investors poured $11.5 billion into U.S. mutual

funds and exchange-traded funds that invest in high-yield bank loans,” notes

Douglas J. Peebles, chief investment officer of fixed-income—bonds—at the

AllianceBernstein investment outfit. A high-yield bank loan is one that carries

particular risk, such as a loan to a company with a poor credit rating or to a

company borrowing money to merge with another firm or to expand; the “yield”

refers to the higher interest rate required to compensate for this risk. Rather

than keep this loan on its books, the bank is selling it, in these cases, to

the exchange-traded funds that are a rising component of shadow banking.

This new

demand has induced lending that otherwise wouldn’t exist—in many cases, for

good reason. “The quality of today’s bank loans has declined,” Peebles

observes, because “strong demand has been promoting lax lending and sketchy

supply. . . . Companies know that high demand means they can borrow at

favorable rates.” Further, says Peebles, “first-time, lower-rated

issuers”—companies without a good track record of repaying debt—are responsible

for the recent boom in loan borrowers, from fewer than 300 institutions in 2007

to closer to 900 today. The number of bank-loan ETFs (and similar “open-ended”

funds) expanded from just two in 1992 to 250 in June 2018.

Peebles

worries as well about the extra risk that this financing mechanism poses to

investors. “In the past, banks viewed the loans as investments that would stay

on their balance sheets,” he explains, but now that banks sell them to ETFs,

“most investors today own high-yield bank loans through mutual funds or ETFs,

highly liquid instruments. . . . But the underlying bank loan market is less

liquid than the high-yield bond market,” with trades “tak[ing] weeks to

settle.” He warns: “When the tide turns, strategies like these are bound to run

into trouble.”

The peril to the economy isn’t just that current investors could lose

money in a crisis, though big drops in asset markets typically lead people to

curtail consumer spending, deepening a recession. The bigger danger is a repeat

of 2008: fear of losses on existing investments might lead shadow-market

lenders to cut off credit to all potential new borrowers, even worthy ones.

Banks, because they’re dependent on shadow banks to buy their loans, would be

unlikely to fill the vacuum. “Although non-bank credit can act as a substitute

for bank credit when banks curtail the extension of credit, non-bank and bank

credit can also move in lockstep, potentially amplifying credit booms and

busts,” says the FSB. The porous borders between the supposedly riskier parts

of the nonbank financial markets—ETFs—and the less risky ones also could work

against a fast recovery in a crisis. Thanks to recent regulatory changes,

insurance companies, for example, are set to become big purchasers of bond ETF

shares.

Worsening

this hazard, just as with the collateralized debt securities of the financial

meltdown, many bond-based ETFs contain similar securities. Such duplication

could eradicate the diversification benefit that the economy supposedly gets

from dispersing risk. Contagion would be accelerated by the fact that

debt-based ETFs, like stock-based ETFs, must “price” themselves continuously

during the day, according to perceived future losses; this, in effect,

introduces the risk of stock-market-style volatility into long-term bond

markets. (Bond-based mutual funds, of course, have existed for decades, but

they did not trade like stocks and thus did not feature this particular risk.)

Via the plunging price of collateralized debt obligations, we saw, in 2008,

what happened to the availability of long-term credit when exposed to the

pricing signals of an equity-style crash, but those collateralized debt

obligations traded far less frequently than bond ETFs do today. Bond ETFs may

be more efficient, yes, in reflecting any given day’s value; that supposed

benefit could also allow a panic to spread more rapidly.

During

the last global panic, the answer to getting credit flowing again—so that

companies could perform critical tasks, such as meeting payrolls, before

revenue from sales came in—was to provide extraordinary government support to

the large banks. But even if one believes that such bailouts are a sensible

approach to financial crises—a highly tenuous position—how would the government

provide longer-term support to hundreds of individual funds, to ensure that the

broader market keeps functioning for credit-card and longer-term corporate

debt? This would greatly expand the government safety net over supposedly

risk-embracing financial markets—by even more than it was expanded a decade

ago.

“When both regular banks and shadow banks are tapped out, we may

need shadow-shadow finance to take up the slack.”

Unwise lending also harms borrowers. Private-equity firms, too, are

increasingly lending companies money, instead of just buying those firms

outright, their older model. As the Financial Times recently reported,

private-equity funds—or, more accurately, their related private-credit

funds—have more than $150 billion in money available for investment. They make

loans that banks won’t, or can’t, make, though this is leading banks to take

greater risks to compete. “It’s been great for borrowers,” says Richard Farley,

chair of law firm Kramer Levin’s leveraged-finance group, as “there are deals

that would not be financed,” or would not be financed on such favorable terms.

Competition

is usually healthy, and risky finance can spark innovation that otherwise

wouldn’t have happened. But easy lending can also make economic cycles more

violent. Even in boom years, excess debt can plunge firms that otherwise might

muddle through a recession deep into crisis, or even cause them to fail, adding

to layoffs and consumer-spending cutbacks. We can see this happening already,

as the Financial Times reports, with bankrupt

firms like Charming Charlie, an accessories store that expanded too fast; Six

Month Smiles, an orthodontic concern; and Southern Technical Institute, a

for-profit technical college.

The

numbers are troubling. The expansion of shadow banking has unquestionably

brought a pileup of debt. The Securities Industry and Financial Markets

Association, a trade group, estimates that U.S. bond markets, overall, have

swollen from $31 trillion to nearly $42 trillion since 2008. Federal government

borrowing accounts for a lot of that, but not close to all of it. The

corporate-bond market, for example, went from $5.5 trillion to $9.1 trillion

over the same decade. Corporations, in other words, owe almost twice as much

today in bond obligations as they did a decade ago. That’s sure to make it

harder for some, at least, to recover from any future downturn.

There are policy approaches to resolving these debt issues. An

unpopular idea would be to treat markets that act like banks, as banks—requiring

ETFs, say, to hold the same capital cushions and adhere to the same prudence

standards as banks. In the end, though, the bigger problem is cultural and

political. What we’re seeing, more than a decade after the financial crisis,

results from the government’s mixed signals about financial markets. On the one

hand, the U.S. government, along with its global counterparts, realized in 2008

that debt had reached unsustainable levels; that’s partly why it sharply raised

bank capital requirements. On the other hand, the government recognized that

the economy is critically dependent on debt. Absent large increases in workers’

pay, consumer and corporate debt slowdowns would stall the economy’s

until-recently modest growth. That’s why the U.S. and other Western governments

have kept interest rates so low, for so long.

Thus, we

find ourselves with safer banks but scarier shadows. Global debt levels are now

$247 trillion, or 318 percent, of world GDP, according to the Institute of

International Finance, up from $142 trillion owed in 2007, or 269 percent of

GDP. When both regular banks and shadow banks are tapped out, we may have to

invent shadow-shadow finance to take up the slack.

Nicole Gelinas is a City Journal contributing editor, a senior

fellow at the Manhattan Institute, and the author of After the Fall: Saving Capitalism from Wall

Street—and Washington.

Decade after financial crisis

JPMorgan predicts next one’s

coming soon

Published

time: 13 Sep, 2018 14:00

© Ole Spata

/ Global Look Press

With the 10th anniversary

approaching of the catalyst for the last major global stock market crash – the

Lehman Brothers’ collapse – strategists from JPMorgan are predicting the next

financial crisis to strike in 2020.

Wall Street’s largest

investment bank analyzed the causes of the crash and measures taken by

governments and central banks across the world to stop the crisis in 2008, and

found that the economy remains propped up by those extraordinary steps.

According to the bank’s

analysis, the next crisis will probably be less painful, however, diminished

financial market liquidity since the 2008 implosion is a “wildcard” that’s

tough to game out.

“The main attribute of

the next crisis will be severe liquidity disruptions resulting from these

market developments since the last crisis,” the reports says.

Changes to central bank

policy are seen by JPMorgan analysts as a risk to stocks, which by one measure

have been in the longest bull market in history since the bottom of the crisis.

JPMorgan’s Marko

Kolanovic has previously concluded that the big shift away from actively

managed investing has escalated the danger of market disruptions.

“The shift from active to

passive asset management, and specifically the decline of active value

investors, reduces the ability of the market to prevent and recover from large

drawdowns,” said JPMorgan’s Joyce Chang and Jan Loeys.

The bank estimates that

actively managed accounts make up only about one-third of equity assets under

management, with active single-name trading responsible for just 10 percent or

so of trading volume.

JPMorgan referred to its

hypothetical scenario as the “great liquidity crisis,” claiming

that the timing of when it could occur “will largely be determined by

the pace of central bank normalization, business cycle dynamics, and various

idiosyncratic events such as escalation of trade war waged by the current US

administration.”

As US banks report record profits

Regulators, Congress move to

end all restraints on Wall Street speculation

On Tuesday, the US

House of Representatives passed a bill to exempt the vast majority of financial

firms from the Dodd-Frank bank regulations passed after the 2008 Wall Street

crash. This coincided with press reports that the Federal Reserve Board and

other bank regulators will announce as soon as next week proposals to gut the

provision of Dodd-Frank most hated by Wall Street—the so-called “Volcker Rule.”

The accelerating

offensive against even the most minimal restrictions on financial speculation

takes place in the context of surging bank profits and CEO pay. On Tuesday, the

Federal Deposit Insurance Corporation, one of the agencies that is preparing to

eviscerate the Volcker Rule, reported that US banks recorded record profits of

$56 billion in the first quarter of 2018, a 28 percent increase over the same

period last year.

As the tenth

anniversary of the September 2008 Wall Street crash approaches, the token

restrictions on the banks that were passed during the Obama administration are

being dismantled. These minimal measures, including increased capital reserve

requirements, annual “stress tests” and limited restrictions on risky

derivative trading, were mainly enacted to provide political cover for the

administration’s multi-trillion-dollar bailout of the financial institutions

responsible for the wholesale destruction of jobs, millions of home

foreclosures and the wiping out of retirement savings.

After eight years of

the Dodd-Frank bank “reform,” the American financial oligarchy exercises its

dictatorship over society and the government more firmly than ever. This

unaccountable elite will not tolerate even the most minimal limits on its

ability to plunder the economy for its own personal gain.

The Volcker Rule,

named after the former chairman of the Federal Reserve Board Paul Volcker, was

included in the 2010 Dodd-Frank act but not drafted and approved by the

regulatory agencies until 2013. It took effect only in 2015.

The rule ostensibly

bars commercial banks, which benefit from federally guaranteed retail deposits

and other government backstops, from speculating with bank funds, including

customers’ deposits, on their own account—a practice known as proprietary

trading. However, the rule incorporates huge loopholes allowing banks to

speculate with their own funds under cover of hedging their investments and

providing liquidity to the financial markets.

At the time of its adoption, the Wall Street Journal cynically but accurately

wrote: “Rest assured banks will find loopholes. And rest assured some of the

Volcker rule-writers will find private job opportunities to help with that

loophole search once they decide to lay down the burdens of government

service.”

No banks have been

cited for violating the rule since it took effect.

Nevertheless, top

Wall Street CEOs such as JPMorgan’s Jamie Dimon and Goldman Sachs’ Lloyd

Blankfein have campaigned ferociously against the measure, denouncing it as an

arbitrary restriction on the financial markets and an impediment to economic

growth. Wall Street lobbyists have spent many millions of dollars bribing

politicians of both parties to weaken the rule to the point of complete

irrelevance.

In a speech to

international bankers in March, Randal Quarles, the Fed’s new vice chairman for

supervision, said, “We want banks to be able to engage in market making and

provide liquidity to financial markets with less fasting and prayer about their

compliance with the Volcker Rule.”

The plan is to make

the rule a dead letter through administrative changes in the language of the

regulation rather than by means of legislation. At the behest of the major

banks, federal regulators are preparing to widen even further the existing

loopholes, allowing the banks to carry out short-term trades with their own

funds and amass more speculative assets in the name of “market-making.” They

will also end requirements that the banks provide documentation to prove that

their activities comply with the rule, relying instead on assurances from the

bankers.

The banking bill

passed by the House on Tuesday increases the Dodd-Frank asset threshold for

financial firms to be considered “systemically important financial

institutions,” and thus subject to tighter regulatory oversight, from $50

billion to $250 billion. This is being presented by Democratic as well as

Republican backers as a matter of fairness to small and midsize banks. In fact,

the exemption covers such giant companies as American Express, SunTrust Banks and

Fifth Third Bank.

These companies will

no longer be subject to yearly Federal Reserve “stress tests” or higher capital

reserve requirements. The bill also exempts banks with less than $10 billion in

assets from the Volcker Rule and exempts banks that have granted fewer than 500

mortgages from reporting requirements.

Thirty-five House

Democrats joined all but one of the House Republicans to pass the measure,

which now goes to President Trump, who has pledged to sign it. The Senate

version was passed in March with broad Democratic support, including 11

Democratic co-sponsors. A total of 17 Senate Democrats voted for the bill.

Another aspect of the

attack on Dodd-Frank is the strangulation of the Consumer Financial Protection

Bureau (CFPB). This agency, lacking any serious enforcement powers and fully

subordinate to the Federal Reserve, was set up under Obama-era legislation to

give the impression of government support for consumers victimized by illegal

or fraudulent banking practices. Despite its toothless character, it was

immediately targeted by Wall Street for destruction.

Under Trump, this

process is now well underway. The White House pressured the Obama holdover

Richard Cordray to resign as director of the CFPB and installed Mick Mulvaney,

Trump’s budget director, as acting head of the bureau to oversee its

dismantling. Mulvaney has halted investigations, imposed a hiring freeze,

stopped the agency from collecting certain data from banks and proposed cutting

off public access to a database of consumer complaints.

Despite

for-the-record verbal protests by Democratic politicians over the gutting of

bank regulations, the removal of restrictions on financial institutions is a

bipartisan policy. Trump’s scorched earth approach is an intensification of the

basic line of the Obama administration rather than a departure from it.

In 2011, the Senate

Permanent Subcommittee on Investigations produced a 650-page report on the

financial crisis documenting in detail the fraudulent and illegal activities of

the major Wall Street banks, aided by corrupt and compliant federal regulatory

agencies and credit rating firms that had a vested interest in promoting the

banks’ subprime mortgage fraud and other swindles. At the time, the chairman of

the subcommittee, Michigan Senator Carl Levin, gave a press conference at which

he said the investigation had found “a financial snake pit rife with greed,

conflicts of interest and wrongdoing.”

Nevertheless, Obama

pursued a deliberate policy of shielding the big banks and their top executives

from criminal prosecution. Financial speculation and fraud continued unabated,

subsidized by the government’s policy of supplying the banks with virtually

free credit by means of near-zero interest rates and the Fed’s money-printing

“quantitative easing” program.

Despite a wave of

scandals, including the manipulation of the key Libor interest rate, JPMorgan’s

$6.2 billion “London Whale” derivative loss, money-laundering cases involving

some of the world’s biggest banks, and the forging of documents to facilitate

home foreclosures, not a single leading banker was criminally charged, let

alone jailed during the Obama years.

This was not because

of difficulties in securing indictments or convictions. On the contrary,

Attorney General Eric Holder told a Senate committee in March of 2013 that the

Obama administration chose not to prosecute the big banks or their CEOs because

to do so might “have a negative impact on the national economy.”

Meanwhile, government

policies favored the further consolidation of financial institutions, including

JPMorgan’s subsidized takeover of Bear Stearns and Washington Mutual, Bank of

America’s acquisition of Merrill Lynch, and Wells Fargo’s absorption of

Wachovia. As a result, the stranglehold of a handful of megabanks over economic

and social life in America is tighter than ever.

Who Can We Blame For The Great Recession?

|

This year

marks the tenth anniversary of the “Great Recession” and the media are trying

to determine if we have learned anything from it. The Queen visited the London

School of Economics after the “Great Recession” to ask her chief economists why

they hadn’t seen this disaster coming. They told her they would get back to her

with an answer. Later, they wrote her a letter saying that the best

economic theory asserts that recessions are random events and they had

successfully predicted that no one can predict recessions.

Still,

George Packer, a staff writer at the New Yorker magazine since 2003, thinks he

knows more than the LSE academics. He wrote the following in the August 27 print

issue:

"It was caused by reckless

lending practices, Wall Street greed, outright fraud, lax government oversight

in the George W. Bush years, and deregulation of the financial sector in the

Bill Clinton years. The deepest source, going back decades, was rising inequality.

In good times and bad, no matter which party held power, the squeezed middle

class sank ever further into debt...

"In

February, 2009, with the economy losing seven hundred thousand jobs a month,

Congress passed a stimulus bill—a nearly trillion-dollar package of tax cuts,

aid to states, and infrastructure spending, considered essential by economists

of every persuasion—with the support of just three Republican senators and not

a single Republican member of the House."

Typically,

journalists will defer to an expert on matters in which they aren’t trained,

which is most subjects. But Packer didn’t bother to ask an economist as the

Queen did. Had he done so, he would have received the same answer from

mainstream economists – recessions are random events and can’t be predicted. If

economists knew the causes of recessions they could predict them when they see

the causes present.

So where