American Economic Confidence Fell Back to Negative in May

The honeymoon is over.

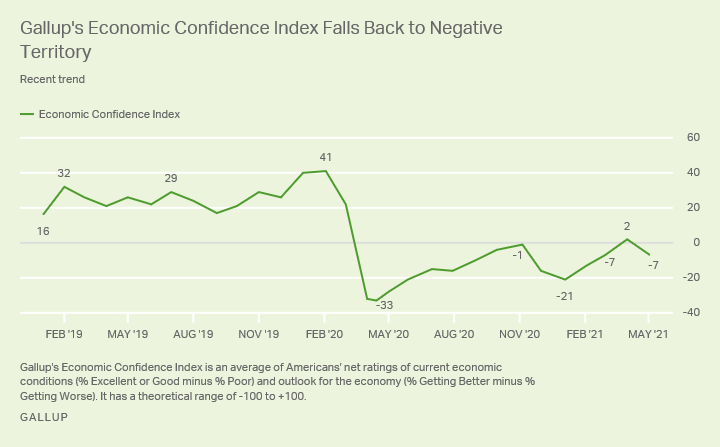

Economic confidence slipped back into negative territory, according to survey data released by Gallup on Monday.

Gallup’s Economic Confidence Index dropped to -7, down from +2 in April and back to the level registered in March.

Gallup said the recent shifts in confidence “may reflect public reaction to a stronger-than-anticipated jobs report in April, followed by a weaker-than-expected report in May.” It is also likely that confidence has been shaken by rising prices and shortages of some products and materials, including the recent widespread gas shortages.

In February of 2020, prior to the pandemic hitting public perceptions, Gallup’s economic confidence index stood at 41.

The decline in May came mostly from a sharp drop in Republican confidence in the month. Republicans in the index register at -52, down from -35 in April. Democrat confidence declined from 31 to 27. Independents went from -4 to -3, a slight improvement.

Two-thirds of Democrats say the economy is getting better, according to Gallup. Just 13 percent of Republicans agree. More than eight in 10 Republicans, 84 percent, believe the economy is getting worse. Independents are slightly more likely to say the economy is getting worse (50%) rather than getting better (44%), Gallup said.

Consumer Confidence Stalls as Hope Falls Apart

Consumer confidence notched down slightly in May as improved assessments of current conditions were swamped by a negative turn in expectations for later this year.

The Conference Board reported Tuesday that its consumer confidence index fell to 117.2 from April’s 117.5 reading, the highest level since February of 2020, just before the pandemic began.

The expectations component of the index, which asks consumers to look out over the next six months, unexpectedly turned sharply downward, falling to 99.1 from 107.9 in April.

The share of consumers expecting business conditions to improve over the next six months fell from 33.1 percent to 30.3 percent, while the share expecting business conditions to worsen rose from 12.1 percent to 14.8 percent. The proportion expecting more jobs fell from 31.7 percent to 27.2 percent, while those anticipating fewer jobs rose from 14.4 percent last month to 17.3 percent.

The income side was more balanced. The share saying they expect incomes to increase fell but so did the share expecting incomes to fall.

The present situation index, based on consumers’ assessment of current business and labor market conditions, jumped to the very strong reading of 144.3 from the already elevated 131.9.

Consumers are very pleased with the current jobs market. The share saying jobs are “plentiful” jumped rom 36.3 percent to 46.8 percent. Those sayng they are hard to get fell to 12.2 from 14.7 percent.

The share saying business conditions are good fell a bit from 19.4 percent to 18.7 percent. But this was offset by a decline in those saying conditions are bad from 24.5 percent to 21.8 percent.

“After rebounding sharply in recent months, U.S. consumer confidence was essentially unchanged in May,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “Consumers’ assessment of present-day conditions improved, suggesting economic growth remains robust in Q2. However, consumers’ short-term optimism retreated, prompted by expectations of decelerating growth and softening labor market conditions in the months ahead. Consumers were also less upbeat this month about their income prospects—a reflection, perhaps, of both rising inflation expectations and a waning of further government support until expanded Child Tax Credit payments begin reaching parents in July.

Huge Miss: New Home Sales Crash as Prices Hit Record High

Sales of new homes plummeted more than expected in April.

Sales fell to a seasonally adjusted annual rate of 863,000 last month, the Commerce Department reported Tuesday. That followed a revised sales pace of 917,000 in March, down from the initially reported 1.021 million sales.

April’s figure is 5.9 percent lower than the revised March figure and 15.5 percent lower than the preliminary number. Each of the previous three months was revised lower. Despite the disappointing data, this was the best sales number for April since 2005.

Economists had expected sales to come in at an annual rate of 955,000.

The median price of a new home sold last month rose to $372,400, up from $310,100 in April 2020, a nearly 20.1 percent year-over-year gain.

On a monthly basis, the median price of a new home rose an astonishing 12.6 percent, ending three consecutive months of declines.

This is the highest median new home price ever recorded. It is also the second-fastest ever monthly gain, following October 2014’s 13.6 percent gain, and the biggest year-over-year jump since November 1987.

Adjusted for inflation, the median price is 10 percent above the March 2007 housing bubble peak.

The miss on new home sales is even more notable because mortgage rates declined in April, which tends to make homes more affordable. But record-high prices in both new and existing homes are putting them out of reach for some would-be buyers and home builders appear to be holding off on projects while labor and materials shortages push up their costs.

No comments:

Post a Comment