America Faces No Greater Threat Than Joe Biden and the Democrat Party. Their Assault to Our Borders Is As Great As Their Assault to Free Speech and Free Elections

Tuesday, August 2, 2022

BIDENOMICS - MIDDLE AMERICA GETS SCREWED - ILLEGALS GET THE JOBS AND BIG OIL RAKES IN STAGGERING PROFITS - Credit Card Debt Jumps Most in 20 Years as Inflation Soars

GET READY, THE ECONOMIC PAIN JUST WORSENED, CREDIT CARD BALANCES EXPLODE, BANKRUPTCY WAVE AHEAD

American households increasingly relied on their credit cards this spring as prices rose at the fastest rate in four decades.

Credit card balances jumped $46 billion in the second quarter of the year. Compared with a year ago, balances are up 13 percent, the largest increase in more than 20 years, according to data released Tuesday by the Federal Reserve Bank of New York.

Credit card balances typically rise in the April through June period. This year’s increase was driven by the highest rate of inflation in 40 years. The Consumer Price Index was up 8.6 percent in the quarter compared with a year earlier, the biggest increase since the fourth quarter of 1981.

Gasoline prices, which rose to record highs in the period, are also driving up spending. Food prices were up 10.4 percent compared with a year ago, the most inflation since 1979. Consumers are also spending more on services and travel. Total consumer spending rose 1.1 percent in June, 0.3 percent in May, and 0.5 percent in April.

Incomes have not kept up with inflation. Real average weekly wages fell one percent in June, 0.9 percent May, and were flat in April. Weekly earnings in June were 4.4 percent below the year-earlier level after adjusting for inflation.

Despite the increase, credit card balances remain slightly below their pre-pandemic level, the New York Fed said.

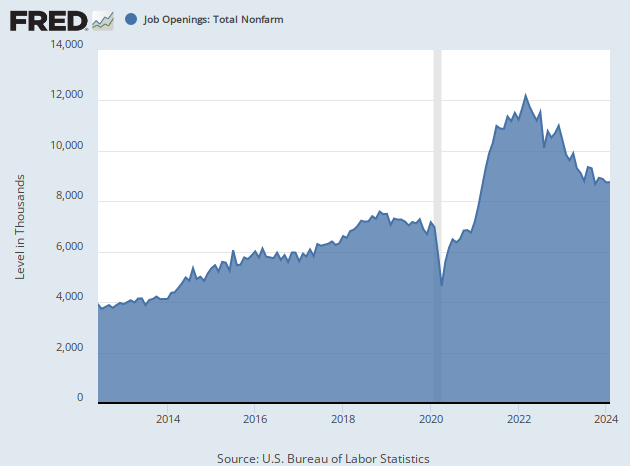

Job Openings Plunge as Employers Pull Back From Hiring

The number of job openings in the United States fell sharply in June as the Federal Reserve hiked interest rates, gas prices hit record highs, inflation soared, and growth in consumer spending slowed.

There were 10.7 million postings for job openings on the last business day in June, the U.S. Bureau of Labor Statistics said Tuesday, down from an upwardly revised 11.3 million a month earlier.

Economists had been expecting 11.1 million jobs in the June report on the government’s Job Openings and Labor Turnover Survey, or JOLTS. The sharper than expected decline indicates that demand for labor has plunged faster than economists expected.

The Federal Reserve has been trying to cool off the labor market by raising interest rates. In mid-June, the Fed hiked its interest rate target by 0.75 basis points, the largest increase since 1994. Tighter financial conditions can slow business expansion, lowering the demand for workers. Fed chairman Jerome Powell has said he would welcome a decline in job vacancies as a sign that the Fed’s efforts to tame inflation are working.

No comments:

Post a Comment