Similar to the Schumer-Manchin bill, Biden’s plan would have provided a $625 billion tax cut for the wealthiest Americans living in blue states — paid for by working and middle class Americans.

Democrats Latest Plan: Target Middle Class Americans with IRS Audits, Keep Billionaire Loopholes Open

A bill backed by Senate Majority Leader Chuck Schumer (D-NY) and Joe Manchin (D-WV) would unleash the Internal Revenue Service (IRS) on middle class Americans while keeping tax loopholes open for billionaires and their multinational corporations.

The plan, which Schumer and Manchin have agreed to, would massively bulk up IRS audits and criminal investigations to the sum of tens of billions of dollars — nearly all of which will be dedicated to going after middle class Americans squeezed by inflation.

The Wall Street Journal editorial board details the scheme:

The bill earmarks $45.6 billion for “enforcement,” including “litigation,” “criminal investigations,” “investigative technology,” “digital asset monitoring” and a new fleet of tax-collector cars. The result will be far more audits, civil suits and criminal referrals. [Emphasis added]

The main targets will by necessity be the middle- and upper-middle class because that’s where the money is. The Joint Committee on Taxation, Congress’s official tax scorekeeper, says that from 78% to 90% of the money raised from under-reported income would likely come from those making less than $200,000 a year. Only 4% to 9% would come from those making more than $500,000. [Emphasis added]

The IRS knows the super-wealthy employ lawyers and accountants who make litigation time-consuming and risky. It also knows that Democrats would howl if the agency pursues fraud in the earned-income tax credit program, despite what the IRS has estimated are $18 billion in improper payments each year. [Emphasis added]

At the same time, tax provisions hugely benefitting billionaires and their multinational corporations would go untouched.

The Schumer-Manchin plan includes billions in green energy tax credits that would be swooped up by billionaires to cut their corporations’ annual tax burdens. Jeff Bezos’s Amazon notoriously employs this strategy to pay close to zero in corporate income taxes.

Breitbart News’s John Carney writes:

Amazon’s tax bills were part of the inspiration for a minimum tax. The company faced no federal corporate income tax liability in 2017 and 2018. In the years since, it has had an effective tax rate that is just a fraction of the 21 percent rate put in place by the Trump administration’s tax reforms. According to the calculations of Matthew Gardner of the Institute on Taxation and Economic Policy, over the past four years Amazon’s effective aggregate tax rate was just 5.1 percent. [Emphasis added]

…

While the alternate minimum tax would prevent companies from using deductions for capital investments or stock-based compensation, it continues to allow them to use tax credits, Daniel Bunn of the Tax Foundation told us. In fact, the bill includes hundreds of billions of dollars worth of new tax credits aimed at fostering green technology adoption. And Amazon plays in beast mode when it comes to using tax credits to reduce its tax bill. [Emphasis added]

Jeff Bezo’s retail giant said in its annual report that tax credits reduced the taxes it would have otherwise owed by $1.1 billion. The company has said that most of those tax credits are federal research and development credits, although it does not give much detail in its annual reports. The Manchin-Schumer tax bill would not touch this. Amazon will lose the benefit of the write-off for stock-based compensation, but the company will most likely at least partially offset that by using the green tech tax credits. The end result could be no change in Amazon’s tax rate. [Emphasis added]

President Joe Biden and House Democrats tried to pass a similar tax plan last year as part of the administration’s “Build Back Better” agenda that has failed to catch on in Congress.

That plan would have targeted an additional nearly 600,000 working and middle class Americans earning less than $75,000 a year with IRS audits. Of those new IRS audits, more than 313,000 would have targeted the poorest of Americans who earn $25,000 or less a year.

Similar to the Schumer-Manchin bill, Biden’s plan would have provided a $625 billion tax cut for the wealthiest Americans living in blue states — paid for by working and middle class Americans.

John Binder is a reporter for Breitbart News. Email him at jbinder@breitbart.com. Follow him on Twitter here.

JOE BIDEN = SLUT FOR WALL STREET, OR ANYONE WITH A BIG BRIBE! JUST ASK THE SLUT HOW WELL HE DID OFF BLACKROCK!

VIDEO

Ralph Nader: Biden's First Year Proves He Is Still a "Corporate Socialist" Beholden to Big Business

https://www.youtube.com/watch?v=2jTIUtjkDss&t=28s

Hauser also didn’t like the prevalence of Big Law talent on the Department of Justice team, which signaled to him that the Biden administration could go soft on corporate malefactors. Alexander Nazaryan

THIS POS LAWYER HAS NEVER OPENED HER FAT MOUTH THAT LIES DID NOT POUR OUT!

Democrats in Washington D.C., such as Senator Elizabeth Warren of Massachusetts, have made noises about corporate “manipulation,” denouncing the handing over of billions of dollars to investors through share buyback programs instead of investing those funds in expansion or the hiring of more workers. Warren, who has repeatedly called herself a “capitalist to my bones,” has been working with the Biden administration on toothless legislation to tax share buybacks, which are expected to reach a record $1 trillion in 2022.

Oil giants reap record profits from war, pandemic and skyrocketing prices

As working class families the world over struggle to afford basic necessities amid historic inflation, driven by the pandemic and the US-NATO war against Russia in Ukraine, the world’s largest multinational oil corporations are announcing record profits.

Over the past week, the six major multinational oil giants—ExxonMobil, Chevron, Shell, BP, TotalEnergies and Eni—reported combined profits of over $64 billion in the second quarter alone. The orgy of profiteering is not limited to the six major oil companies. The smaller US companies Valero, Phillips 66 and Hess posted a massive combined quarterly profit of $8.62 billion.

In total, these nine companies reported over $72 billion in profits over three months. The oil companies, by and large, have refused to increase production, driving gas prices in the United States earlier this summer to an average of $5 a gallon and siphoning billions from working class families into their coffers. While the price of a gallon of gas has dipped somewhat in the last month to a nationwide average of $4.19 a gallon, this is still over a dollar more than the $3.17 recorded at this same time last year.

Every day during this period, the oil companies made $800 million in profit, or about $33.3 million an hour.

An analysis by the Natural Resources Defense Council (NRDC), an environmental lobbying group that tracks the profits of the 15 largest oil and gas companies in the United States, found that compared to the same period in 2021, oil company profits grew “a staggering 242 percent.”

The largest private oil company in the United States, ExxonMobil, reported a second-quarter profit of nearly $17.9 billion, which represents a year-to-year increase of 226 percent, according to the NRDC. Overall, ExxonMobil has reported over $23.3 billion in profits this year alone.

Chevron reported a second-quarter profit of $11.62 billion, a 277 percent year increase from a year ago. The United Steelworkers union played a key role in the company’s massive profit increase through its isolation and betrayal of Chevron workers’ struggles for improved wages and working conditions, including its sellout in June of a strike by 500 oil workers in Richmond, California.

UK-based Shell reported a second-quarter profit of $17.85 billion, a 107 percent increase from last year, bringing this year’s total profits to date to over $20 billion.

Italian-based oil giant Eni reported a second-quarter adjusted net profit of $3.88 billion, a year-to-year improvement of nearly $1 billion.

French-based TotalEnergies likewise posted an all-time-high second-quarter profit of $9.8 billion, nearly a three-fold increase from last year. This figure topped the company’s previous high set in 2008, when the price of a barrel of oil (Brent Crude) was $147, roughly $47 more than current prices.

The profit figures exceeded Wall Street expectations and left investors and oil billionaires salivating at the prospect of stock buybacks and increased dividend payments. Instead of using their ill-gotten profits to hire more workers, increase wages or invest in new technologies to improve safety and combat the impact of climate change, all of the oil companies announced a new round of stock buybacks.

Industry publication RigZone.com notes that TotalEnergies already “bought back $2 billion of its shares” in the second quarter, and “will do so again in the third quarter.” The publication continued: “The board of directors of the company also approved the distribution of the second dividend in 2022, 5 percent higher year-on-year.”

Similarly, BP has spent $3.9 billion on stock buybacks in the first half of the year and announced another $3.5 billion buyback for the third quarter. The New York Times reported that the company would “devote 60 percent of its ‘surplus cash flow’ this year to share buybacks,” and raise the stock dividend by 10 percent.

ExxonMobil has already spent $7.6 billion on dividends and share purchases through the second quarter.

The New York Times reported Tuesday that BP, Chevron, ExxonMobil, Shell and TotalEnergies have collectively spent some $25 billion in the first half of the year buying back their own shares.

While the portfolios of major oil company shareholders are booming, American families are falling deeper into debt, unable to keep up with record cost-of-living increases and soaring interest payments fueled by the Federal Reserve’s rate-hiking program. At the same time, the Fed is deliberately engineering a slowdown in economic activity in order to drive up unemployment and undermine workers’ struggles for higher wages and better working conditions.

On Tuesday, the New York Federal Reserve reported that US household debt exceeded $16 trillion for the first time ever. It noted that credit card balances increased by $46 billion last year.

According to CNN, in the past year overall credit card debt has “jumped by $100 billion, or 13 percent, the biggest percentage increased in more than 20 years.”

The oil companies’ price-gouging and profiteering in the midst of mass death from the pandemic and the escalating US-NATO war against Russia underscores the necessity for the working class to take possession not only of fuel, but also of food, medicine and all the other essentials of modern life to use for the betterment of all of humanity, not the enrichment of privileged idle few.

This means a conscious and united fight by the working class to put an end to the profit system and reorganize economic life on socialist foundations.

Coal millionaire Manchin promotes Democrats’ phony “climate” bill

The Biden administration and the Democratic Party are perpetrating a gigantic fraud on the American public in the form of the so-called Inflation Reduction Act of 2022, announced with great fanfare last week.

The deal was suddenly announced July 27 by Senate Majority Leader Charles Schumer and West Virginia Senator Joe Manchin and hailed by President Biden as a “historic” advance in the fight against climate change. The Democratic-aligned media called it a “big win” for the administration and the Democratic Party.

Schumer said he hoped to bring the measure to the Senate floor for a vote this week and get it passed before the August recess. However, its prospects remain unclear, with Arizona Democrat Kyrsten Sinema so far withholding her support, which represents the critical 50th vote given expected unanimous Republican opposition.

The title given to the measure, cynical to the core, is indicative of its basic purpose—to give the impression that the administration is doing something to address the crushing cost-of-living crisis that is gutting workers’ wages, as well as other incendiary factors such as the ever-growing chasm between the rich and the masses of people.

It is an elaborate political ploy crafted under conditions of an explosive crisis, not just of the Democratic Party, but of the entire two-party system upon which the corporate oligarchy relies to stabilize its rule.

The bill would allocate $369 billion over 10 years to “address” the climate crisis plus $64 billion to fund a three-year extension of Affordable Care Act subsidies for people buying health insurance, which otherwise would expire shortly before the November mid-term elections, causing premiums to soar for millions of voters.

It would raise an estimated $739 billion in new revenue, over 10 years, by imposing a minimum corporate tax of 15 percent ($313 billion), tightening the so-called “carried interest” tax loophole for hedge fund managers and wealthy investors ($14 billion), increasing tax enforcement by the Internal Revenue Service ($124 billion), and empowering Medicare to negotiate some drug prices with the pharmaceutical companies ($288 billion).

The excess of projected revenues over outlays, $300 billion over 10 years, a drop in the bucket compared to the massive federal deficit, is being touted for its “anti-inflationary” and budget discipline benefit.

Virtually all of the money for renewable energy development—solar, wind and other technologies—consists of massive tax credits for the growing clean energy industry. The bill also includes subsidies for purchasers of electric vehicles, which are tied to protectionist “made in America” requirements for the vehicles that will likely not be met until the end of the decade. The bill would also extend tax breaks for nuclear power corporations.

For the coal, oil and gas corporations, the main producers of greenhouse gases, the measure is an unabashed boondoggle. The Wall Street Journal published a front-page article last Friday headlined “Climate Bill is Boon for Fossil-Fuel Sector.” It notes that the bill requires the federal government to “offer more access for drilling on federal territory.”

Specifically, it would require the US Interior Department to offer up at least 2 million acres of federal land and 60 million acres of offshore territory to oil and gas products every year for the next decade. The Journal notes: “It would be the first-ever required minimum acreage for offshore oil and gas leasing and significantly increase the acreage requirements for onshore leasing.”

It would reinstate an 80-million-acre sale for the Gulf of Mexico from 2021 that was invalidated by a federal judge. This was the biggest offshore oil and gas lease sale in American history.

The bill would not only authorize new drilling in the Gulf of Mexico, but it would expand it to offshore Alaska.

Small wonder Shell CEO Ben van Beurden hailed the bill, saying, “The world needs new oil and gas to come on stream.”

Moreover, Manchin announced that he had secured a promise from President Biden, Senate Majority Leader Charles Schumer and House Speaker Nancy Pelosi to hold a vote on a separate measure in the fall that would make it easier for developers to override environmental objections when building pipelines, natural gas export facilities and other energy infrastructure.

Manchin has been pushing to override protests by environmentalists and small landholders in his home state of West Virginia against completion of the Mountain Valley gas pipeline between West Virginia and Virginia.

The bill scraps Biden’s campaign promise to end leasing of federal lands for oil and gas development. It is, as many climate groups have noted, “all carrot and no stick,” providing hundreds of billions in subsidies to companies that expand clean energy production and no penalties for polluters.

Brett Hartl, government affairs director at the Center for Biological Diversity, called it a “climate suicide pact.”

Wenonah Hauter, executive director of Food & Water Action, said in a statement that the bill “won’t solve the climate crisis and may make it worse.”

While the give-aways to big business are massive, the benefits for ordinary people in the form of lower drug costs are minimal. Drug prices negotiated between Medicare and Big Pharma would not begin to take effect until 2026. They would cover only 10 drugs that year, 15 more in 2027 and 20 more in 2029, according to the Kaiser Family Foundation.

Negotiated prices would not be permitted until nine to 13 years after a new drug’s introduction. No drugs with generic competitors would be affected. Insulin, which is a lifeline for tens of millions in the US, would not be covered. The investment firm Raymond James noted that prices for new drugs would be higher under the bill.

The 15 percent minimum corporate tax, 6 percent below the current corporate tax rate, will be widely evaded by big corporations and their army of tax lawyers. The tightening of the tax loophole for hedge fund owners and big investors will barely make a dent on the fortunes of the idle rich. Meanwhile, the sweeping tax cuts for corporations and the rich in Trump’s 2017 tax overhaul remain intact.

All of the social measures in the administration’s various iterations of “Build Back Better” last year are gone, including expanded child tax credits; paid sick and family care leave; dental, vision and hearing coverage under Medicare; and housing assistance.

In the course of 2021, the Democratic leadership reduced Biden’s proposed social spending and tax bill from $6 trillion to $3.5 trillion and finally to $1.75 trillion, in a never ending effort to win Manchin’s support, only to have him torpedo the final deal last December.

Manchin issued his own statement last Wednesday, boasting that the deal with Schumer eliminated “trillions in new spending” in Biden’s earlier bills. “Build Back Better is dead,” he gloated.

In keeping with his status as the most powerful man on Capitol Hill, Manchin appeared on all five of the Sunday morning television interview programs. He stressed that the bill protected fossil fuel production and described it as a gain for US energy “security” and “independence.”

Repeatedly praising his “Republican colleagues,” Manchin refused to even say he would like to see the Democrats retain control of Congress in the November elections or commit himself to supporting Biden in 2024.

The deal between Schumer and Manchin to produce something that could be packaged as climate-friendly and “progressive” was driven largely by political considerations. Inflation, recession, war, a raging pandemic, a Trump-dominated and increasingly fascistic Republican Party and a rightward hurtling, discredited Democratic Party—confronted by an insurgent working class—add up to a formula for social upheavals with revolutionary implications.

Biden’s poll numbers have continued to plunge—A CNN poll last week found that 75 percent of Democratic voters would like to see someone other than Biden as the party’s presidential candidate in 2024—and midterm elections are fast approaching that could see Trump’s coup supporters gaining control of Congress.

To obtain Senate passage of any bill that even nominally addresses the climate crisis and raises taxes on corporations and the wealthy, no matter how modestly, the Democrats must get every member of their caucus on board in the evenly divided chamber and use the budget reconciliation procedure, which prohibits the use of a filibuster. Then they can pass a measure with 50 votes plus the tie-breaker cast by Vice President Kamala Harris, the president of the Senate.

Under these conditions, Schumer entered into secret talks with Manchin several weeks ago with Biden’s blessing to salvage something from the debacle of the administration’s “Build Back Better” domestic agenda. The evident price was capitulation to Manchin’s basic demands.

Manchin, along with Sinema, occupies the right flank of the Democratic Senate caucus. A multi-millionaire coal operator, he is the Senate’s biggest recipient of campaign cash from the fossil fuel industry. Sinema shills for the hedge fund and investment industry, which has handed her $2.2 million in donations since 2017, more than any other senator, according to the OpenSecrets tracker. She has made clear her opposition to any reduction in the tax loophole for hedge fund and private equity managers.

READ MORE

GET READY, THE ECONOMIC PAIN JUST WORSENED, CREDIT CARD BALANCES EXPLODE, BANKRUPTCY WAVE AHEAD

15 Signs That A Day Of Reckoning Has Arrived For The U.S. Auto Industry

DRAMATIC Increase In Foreclosure Filings +150%

In the face of the daily cuts in their standard of living

resulting from the highest inflation in more than four

decades, workers are compelled to undertake a struggle for

necessary wage increases. But as they are driven into this

fight, it is necessary for workers to understand what is at

stake in order to better conduct the battle at hand.

Credit Card Debt Jumps Most in 20 Years as Inflation Soars

American households increasingly relied on their credit cards this spring as prices rose at the fastest rate in four decades.

Credit card balances jumped $46 billion in the second quarter of the year. Compared with a year ago, balances are up 13 percent, the largest increase in more than 20 years, according to data released Tuesday by the Federal Reserve Bank of New York.

Credit card balances typically rise in the April through June period. This year’s increase was driven by the highest rate of inflation in 40 years. The Consumer Price Index was up 8.6 percent in the quarter compared with a year earlier, the biggest increase since the fourth quarter of 1981.

Gasoline prices, which rose to record highs in the period, are also driving up spending. Food prices were up 10.4 percent compared with a year ago, the most inflation since 1979. Consumers are also spending more on services and travel. Total consumer spending rose 1.1 percent in June, 0.3 percent in May, and 0.5 percent in April.

Incomes have not kept up with inflation. Real average weekly wages fell one percent in June, 0.9 percent May, and were flat in April. Weekly earnings in June were 4.4 percent below the year-earlier level after adjusting for inflation.

Despite the increase, credit card balances remain slightly below their pre-pandemic level, the New York Fed said.

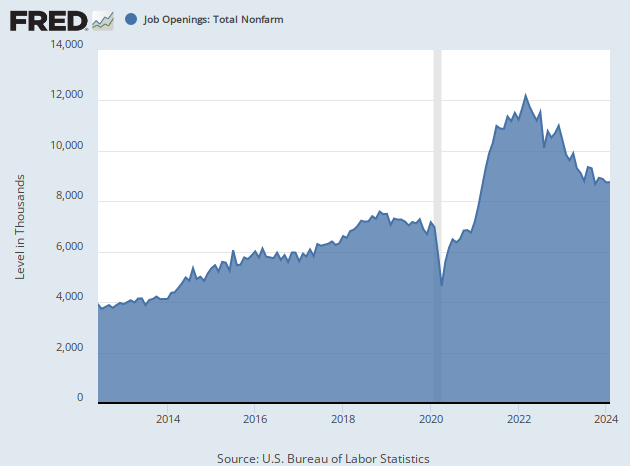

Job Openings Plunge as Employers Pull Back From Hiring

The number of job openings in the United States fell sharply in June as the Federal Reserve hiked interest rates, gas prices hit record highs, inflation soared, and growth in consumer spending slowed.

There were 10.7 million postings for job openings on the last business day in June, the U.S. Bureau of Labor Statistics said Tuesday, down from an upwardly revised 11.3 million a month earlier.

Economists had been expecting 11.1 million jobs in the June report on the government’s Job Openings and Labor Turnover Survey, or JOLTS. The sharper than expected decline indicates that demand for labor has plunged faster than economists expected.

The Federal Reserve has been trying to cool off the labor market by raising interest rates. In mid-June, the Fed hiked its interest rate target by 0.75 basis points, the largest increase since 1994. Tighter financial conditions can slow business expansion, lowering the demand for workers. Fed chairman Jerome Powell has said he would welcome a decline in job vacancies as a sign that the Fed’s efforts to tame inflation are working.

No comments:

Post a Comment