THE PURPOSE OF GOVERNMENT IS TO EXTRACT WEALTH FROM THE 99% AND TUCK IT INTO THE BOTTOMLESS POCKETS OF THE 1%.

25OK EXPECT EVICTION IN MEXICO'S SECOND LARGEST CITY

LOS ANGELES HOUSING NIGHTMARE BEGINS! EVICTION BAN FINALLY ENDS, ECONOMIC SHOCK, STREETS OF DANGER

JP Morgan: Shadow Vacancy About to UNLOAD onto Real Estate Market

BOOK:

#PouredOver: Matthew Desmond on Poverty, by America

Poverty, by America": Author Matthew Desmond on How U.S. Punishes the Poor & Rewards the Wealthy

Matthew Desmond on ‘Poverty, by America’

Poverty, by America - In conversation with Matthew Desmond

HUGE LAYOFFS, BEST BUY, DAVID'S BRIDAL, FINANCIAL CRISIS IS NOT SOLVED, BANKS INITIATE CREDIT CRUNCH

Pessimism on the Economy Hits All-Time Worst Level, Dragging Down Biden’s Approval Rating

The share of the American public holding negative views about the U.S. economy both now and in the future reached a record high 69 percent, a CNBC poll showed Tuesday.

This is the highest proportion of negative views about the economy in the 17-year history of CNBC’s All-America Economic Survey, which is based on a poll of 1,000 people nationwide.

The grim view of the economy is weighing on President Joe Biden’s popularity. His overall approval rating fell two points to 39 percent in the most recent survey compared with the November survey. Fifty-five percent say they disapprove of Biden, up a point from the November survey.

On the economy specifically, American’s disapprove of Biden’s handling of the issue by 62 percent to 34 percent. In the November survey, this was 57 percent to 38 percent, which means Biden has lost ground on this metric.

Biden’s approval among independents crashed nine points to just 27 percent. He even lost two points among Democrats, with 77 percent saying they approve.

Among women aged 18 to 49, a key constituency for Democrats, Biden’s approval fell 13 points to just 34 percent.

Just five percent of Americans say their income is rising faster than inflation. Twenty-six percent say their household income is keeping pace with rising prices. Sixty-seven percent said they are falling behind.

Just 24 percent say now is a good time to invest in stocks, the lowest reading in the survey’s history. The prior record was last quarter at 26 percent.

25OK EXPECT EVICTION IN MEXICO'S SECOND LARGEST CITY

LOS ANGELES HOUSING NIGHTMARE BEGINS! EVICTION BAN FINALLY ENDS, ECONOMIC SHOCK, STREETS OF DANGER

JP Morgan: Shadow Vacancy About to UNLOAD onto Real Estate Market

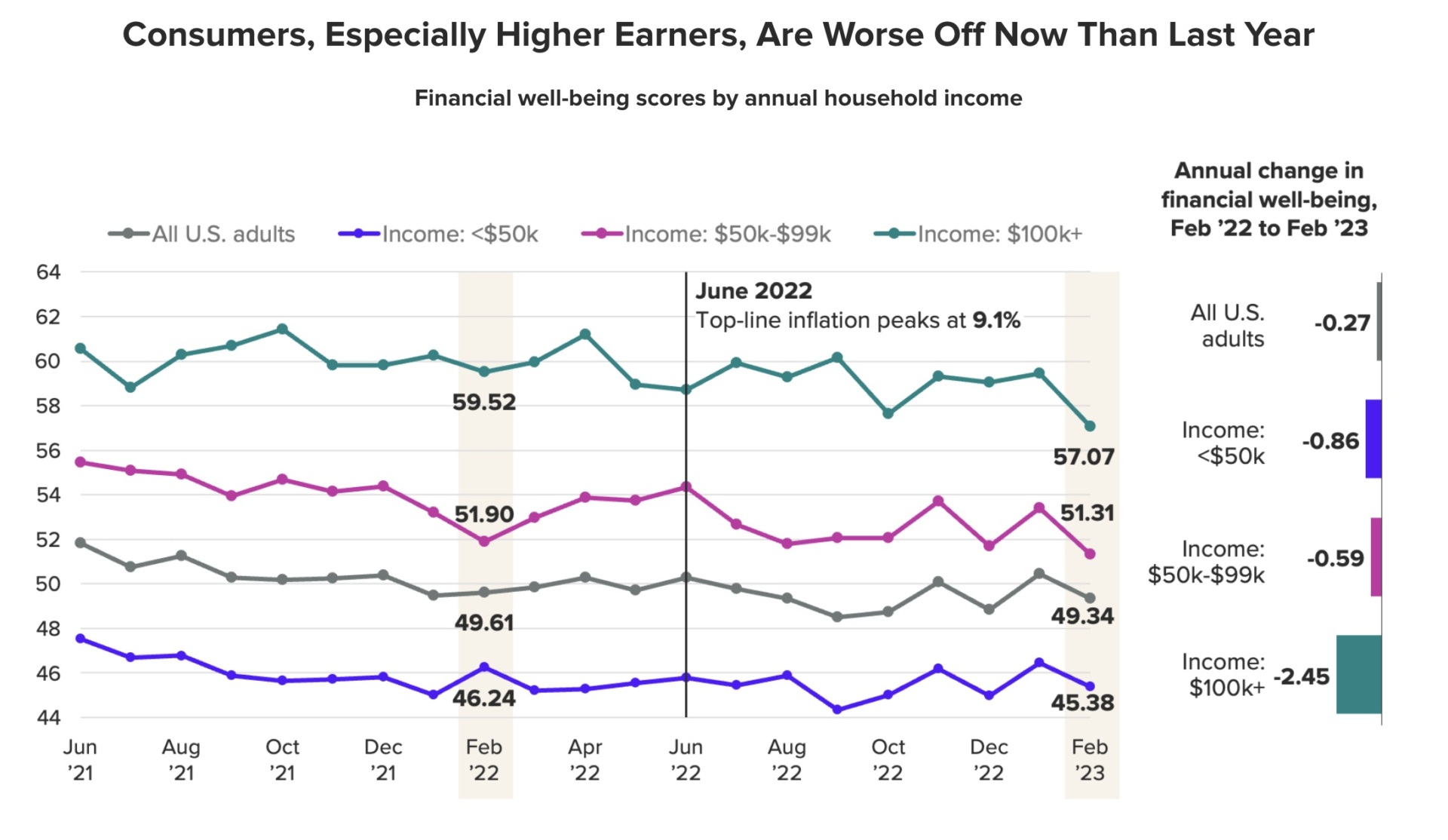

Survey: All Consumers Financially Worse off Following Biden’s Inflation, Debt

All U.S. consumers are financially worse off now than last year with growing personal debt following President Joe Biden’s inflation, a Morning Consult’s State of Consumer Banking and Payments report revealed Tuesday.

The report found that rising interest rates, soaring inflation, and the banking crisis has Americans feeling worse off financially than last year.

The financial well-being scores by annual household income dropped across all income levels in 2023. The hardest hit appears to be those earning larger incomes, though all consumers have felt the impacts of Biden’s fiscal and energy policies:

- Income <$50k (-0.86)

- Income $50k-$99K (-0.59)

- Income $100k+ (-2.45)

- All adults (-0.27)

One of the key drivers in negative well-being was Biden’s inflation, fueled by a manufactured energy crisis. In March, the Federal Reserve continued to increase interest rates by a quarter of a percent (25 basis points), a decision subject to speculation by financial experts, as the central bank weighed reducing soaring inflation and the stability of the banking system.

The report shows interest rates have most greatly impacted households earning over $100,000 a year. High earners are more likely to hold financial assets impacted by increased interest rates.

The middle class has also been hurt by inflation. In 2022, Biden’s 40-year-high inflation cost American households an average of $5,200 extra, or $433 per month, according to Bloomberg.

While the study found that high-income earners were most impacted by Biden’s inflation in 2022, younger consumers were burdened with personal debt.

“The share of millennials who reported having credit card, auto, mortgage, educational, medical, personal, ‘buy now, pay later,’ home equity and other types of debt was higher compared to any other generation, across all debt types examined,” the report found.

A driver of personal debt for younger generations was student loans. Thirty-three percent of millennials and 21 percent of Gen Zers revealed to the study that they have debt from attending institutions that often employ far-left professors. Sixteen percent of Gen Xers, the oldest of the younger generations, still retain student debt.

The report sampled 4,400 Americans per month from July 2021 to March 2023. No margin of error was provided.

Follow Wendell Husebø on Twitter @WendellHusebø. He is the author of Politics of Slave Morality.

No comments:

Post a Comment