America Faces No Greater Threat Than Joe Biden and the Democrat Party. Their Assault to Our Borders Is As Great As Their Assault to Free Speech and Free Elections

Tuesday, June 20, 2023

BIDENOMICS - WILL JOE DESTROY THE ECONOMY AS FAST AS HE DESTROYED THE BORDER? - if Joe Biden's economy is as great as he says it is, why have 401(k)s plunged 20%?

Video: Stephen Moore Slams the ‘Bidenomics Calamity’

Leading conservative economist speaks to a crowd of Freedom Center supporters about the worst President ever.

Speaking to a David Horowitz Freedom Center crowd on Wednesday, June 14, 2023 at the Four Seasons in Beverly Hills, conservative economist Stephen Moore took aim at the “abysmal” Joe Biden and the economic havoc he’s caused.

Look, here's where we are. We have the fastest growing economy in the world, the world, the world. We have 8.6 million new jobs just since I got in an office. Unemployment rates down to 3.6%. We've reduced the deficit last year by $320 billion, this year going to reduce it by $1.7 trillion dollars, trillion dollars.

Vanguard, which tracks about 5 million retirement accounts, found the average account balance for 401(k)s and 403(b)s was $112,572 in 2022 – down nearly $30,000 from the previous year.

"Vanguard participants’ average account balances decreased by 20% since year-end 2021, driven primarily by the decrease in equity and bond markets over the year," the report said.

I calculated a 26% drop based on the estimated $30,000 amount, but even if Vanguard is closer to correct, that's still a double-digit drop in the span of just a year, an astonishing amount.

It's obviously commeasurate with the stock and bond market drops, as the report noted.

It's also the result of battered consumers making early withdrawals for "hardship" from their savings. That could be sudden medical bills, suddenly surging credit card rates, or credit card debt piling up as inflation eats into paychecks.

About 2.8% of workers participating in employer-sponsored 401(k) plans made a so-called "hardship" withdrawal in 2022, according to the report. That marks a major increase from the 2% rate recorded before the pandemic began and is also up from the 2.1% reading in 2021.

Another reason is that worker wages fell 2.3% in 2022, according to this Bloomberg report last month:

US weekly wages fell in 2022, according to new Bureau of Labor Statistics figures, revealing widespread softness that wasn’t previously evident in other data.

Average weekly wages were $1,385 in the fourth quarter of last year, a rare 2.3% decline from the same period in 2021, the latest results from the Quarterly Census of Employment and Wages, published Wednesday, showed. The 2022 drop followed a 5.9% increase the year before.

But nobody's bills went down, let alone their credit card interest rates. As wages dropped, those things went up. Inflation squeezed workers from two ends. So the next thing to go was the 401(k) where worker contributions went down, and worker withdrawals went up:

The average 401(k) participant’s contribution rate dropped from 6.6% of their income in 2021 to 6.4% in December 2022, according to Bank of America’s 401(k) Participant Pulse report released Wednesday. It's a sign that Americans are more concerned about short-term financial needs right now, according to the bank’s analysis.

Which is sad stuff, and indicative of workers having personal finance fires to put out now, with no faith in the future. Some 40% of workers are now delaying retirement, mostly to age 68, in order to have enough money to retire on, not just from inflation but to help struggling family members, based on all of these retirement-savings eaters going on, according to a January MarketWatch report .

Meanwhile, bankruptcies are up 20% for consumers and 213% for corporations, and debt restructuring companies are enjoying a bumper harvest in new business.

Here's other nasty stuff from that Fox26 report published last month:

Credit card delinquencies are climbing, especially for people ages 18 to 39, at 8.3% from 5.1% a year ago, according to the New York Fed.

And Cox Automotive reports borrowers more than 2 months late on auto loan payments was 26.7% higher in December than a year earlier.

Here's the cherry on the cake: Inflation is indeed getting under control, with the CPI clocking in at 4% on the last reading, down from from the 9.1% seen a year earlier, which still is twice what it was when President Trump was in office, but quite a bit better than what we have seen from Bidenflation. That has caused the Fed to pause on the rate hikes which are driving up the mortgage and credit card rates, but it has signaled it still may hike a couple more times this year.

Despite the pause, Americans are unlikely to see any relief according to Greg McBride, CFA, chief financial analyst with Bankrate.com.

"A pause won’t bring borrowing rates lower, particularly for variable rate debt such as credit cards and home equity lines of credit that have increased in step with the Fed’s 10 previous interest rate hikes," McBride said. "Elevated inflation and a strong labor market mean the Fed is nowhere close to cutting interest rates, so borrowers will continue to be dealing with high interest rates for months to come, even if the Fed doesn’t hike rates further."

Well, lucky us.

Let's just say that these things don't happen in a healthy, growing, economy, such as we saw in President Trump's.

Worker 401(k) falls in savings are hugely demoralizing to their savers, and are said in some studies to affect voting choices, particularly for older voters more than any other factor, and voters know which parties and politicians are better for their 401(k)s just from experience.

While this ugly picture is, well, ugly, it does have potential to affect voting choices as surely as gasoline prices. One hopes that some kind of relief can come soon, but in the meantime, we can all see why so many voters are tuning out Joe Biden's ridiculously insulting claims of having fostered some kind of economic booms. To paraphrase the memorable Lloyd Bentsen, We know economic booms, Joe, we remember economic booms well, and you're no economic boom.

As a private American citizen, I would like to share some matters of public interest. Specifically, I would like to report and share my transformative thoughts through commentary about an article titled: A Walmart Worker’s View on the Retirement Divide.

All rights and credit go directly to its rightful owners. No copyright infringement intended. This is a link to the article that I referenced in my video; I encourage you to read the full article to support the author and the news source: https://inequality.org/research/walma...

Under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship and research. Fair use is a use permitted by copyright statute that might otherwise be infringing.

The matters of public interest that I discuss as a private American citizen relate to any matters of financial, political, social, or other concerns to the community or subjects of legitimate news interest; that are, subjects of general interest and of value and concern to the public. There is substantial truth in what I discuss, but please overlook any minor inaccuracies. The content that I share is for entertainment purposes only, and you should not construe any such information as legal, tax, investment, financial, real estate, insurance, or other advice. Opinions expressed are solely my own and do not express the views or opinions of my

WHAT WOULD THE HOUSING AND JOBS CRISIS BE WITHOUT 50 MILLION ILLEGALS?

IN AMERICA THE RICH GET RICHER AND ILLEGALS GET THE JOBS TO KEEP WAGES DEPRESSED.

20 Imminent Signs The American Society Is Collapsing

The largest caucus of House Republicans proposed Wednesday that the US retirement age for collecting full Social Security benefits be raised to 69 from the current 66. The Republican Study Committee (RSC), with 176 out of the 222 Republican members of the House of Representatives, made the proposal as part of a “fiscal blueprint” that would cut spending by $16.3 trillion over the next decade, compared to the projected baseline.

The plan also includes making the Trump tax cuts for the wealthy permanent—they are currently scheduled to expire in 2027—while leaving Pentagon spending untouched, at a gargantuan $886 billion for the coming year.

Automatic (entitlement) spending programs like Social Security, Medicare and Medicaid would absorb two-thirds of the cuts proposed by the RSC, with discretionary spending programs, those which must be voted on by Congress each year, absorbing one-third, or about $5 trillion. With military spending kept intact, the discretionary cuts would fall entirely on domestic social spending, and programs on the environment, mass transportation, housing and education would see cuts of 30 percent or more.

President Joe Biden and House Speaker Kevin McCarthy of California walk down the House steps Friday, March 17, 2023, on Capitol Hill in Washington. [AP Photo/Mariam Zuhaib]

It was the first time since the Republicans gained a narrow majority in the House in the 2022 elections that so many Republican members have publicly committed themselves to a major cut in Social Security benefits. The RSC made a similar proposal last year; Republicans were in the minority and its recommendations had no prospect of receiving a vote on the House floor.

The RSC dropped a proposal, adopted a year ago, to raise the eligibility age for Medicare from the present 65. But the “blueprint” includes significant measures to promote the privatization of Medicare, an intermediate step towards dismantling the program entirely.

Social Security was established under the “New Deal” Roosevelt administration in 1935. Medicare was established under the Johnson administration in 1965, as the centerpiece of its loudly proclaimed “war on poverty.” The “war” was quickly abandoned by the Democrats, but Medicare has remained as a fixture in the lives of tens of millions of elderly and retired people, many of them entirely dependent on the federal insurance program to assure access to affordable health care.

The RSC proposal would phase in the increased retirement age for full Social Security benefits gradually, adding four months a year until it is age 69 for those turning 62 in the year 2033—the more than 3 million people who were born in 1971. Age 62 will remain the lowest age at which people can take early retirement, but with severely reduced benefits.

The current retirement age is already going up gradually to age 67, a month each year, until 2027. This increase was agreed upon in the bipartisan deal between Democratic House Speaker Tip O’Neill and Republican President Ronald Reagan in 1983, which supposedly “saved” Social Security but only postponed the crisis.

The bourgeois media portrays the “crisis” in Social Security as a purely demographic problem: the elderly are living much longer than envisioned when the program was first established, and changes must be made in eligibility and benefit levels to reflect that. Similar claims were made by French President Emmanuel Macron when he pushed through a two-year increase in the French retirement age, from 62 to 64, against explosive mass resistance among working people that was diverted and suppressed by the trade unions.

In reality, the program is running short of funds primarily because of the ceiling on taxation of the wealthy—who pay Social Security taxes only on the first $160,000 in income, even if they take in millions or even billions in a year. Moreover, Wall Street looks upon the gargantuan amounts still remaining in the Social Security Trust Fund as a source of new investment funding for its parasitic financial operations, while the Pentagon views it hungrily as a potential resource for the military.

The Republican Study Committee proposal is unlikely to pass in the near future because Democrats control the Senate and the White House, and they will seek to demagogically present themselves as the defenders of Social Security in the 2024 elections. But it is highly significant politically, because it puts the question of Social Security cuts, once described as the “third rail” of American politics, squarely on the agenda of future congresses and administrations.

The pattern over many decades is that the Republican Party sets the most right-wing marker on social policy, the Democrats claim to oppose them and to defend the interests the poor, the sick and the elderly. Then the two parties make use of the next crisis—or manufacture one, as in this year’s agreement on the federal debt ceiling—to adopt a “compromise” proposal, taking a giant step in the reactionary direction first indicated by the Republicans.

There have already been a slew of right-wing Democrats, like Senator Joe Manchin of West Virginia, who have indicated their willingness to “consider” changes in Social Security and Medicare eligibility that will devastate millions of retired people.

Biden continues the posture of irreconcilable opposition to changes in Social Security that he adopted in his State of the Union speech, when he charged that Republicans wanted cuts and they vociferously denied it, some interrupting him from the floor of the House of Representatives. But there is no question that if Biden has to choose between funding the war against Russia in Ukraine, and funding full benefits for the elderly, that he will join the Republicans in demanding “sacrifices” from the American people.

Besides enlisting more than three-quarters of all House Republicans, the supposedly “mainstream conservative” RSC includes Majority Leader Steve Scalise, the third-ranking Republican Elise Stefanik, Kay Granger, chair of the Appropriations Committee, and other top House Republicans. (By convention, Speaker Kevin McCarthy does not belong to ideological caucuses.)

The RSC also includes seven of the 11 Republican representatives who participated in last week’s disruption of House functioning. These 11, all members of the far-right House Freedom Caucus, voted against the rule proposed by the Republican leadership to schedule bills for consideration and govern debate for the week. Traditionally, these are party-line votes, and with all Democrats also opposed, the rules failed and the House could not take any action.

The 11 were venting their spleen against the debt-ceiling agreement between McCarthy and Biden, saying the spending cuts provided were too little and claiming that McCarthy could have forced an even bigger surrender by the White House by blocking an increase in the debt ceiling, an action which threatened to trigger a meltdown on Wall Street.

McCarthy met with the 11 on Monday and they agreed to unblock the work of the House in return for unspecified concessions by the Republican leader on bringing up legislation and seeking even more cuts in federal spending.

As part of this process of pushing the House further and further to the right, Appropriations Committee Chair Kay Granger announced Monday evening that most Appropriations subcommittees would receive smaller allocations of spending authority than agreed on in the Biden-McCarthy deal. Money for the Pentagon, the Veterans Administration and the Department of Homeland Security would be unaffected.

For all other programs, instead of freezing spending at 2023 levels, as Biden and McCarthy agreed, the subcommittees would be instructed to hold spending to 2022 levels, cutting another $160 billion. This was the central demand of the Freedom Caucus members, who claimed McCarthy had agreed to that as part of the wheeling and dealing that made possible his election as speaker in January after an unprecedented 15 ballots.

In both capitalist parties, the dynamic is the same: the most right-wing elements drive the policy-making process, because they have the support of the capitalist ruling elite. In the Republican Party, a handful of fascists hold the whip hand over McCarthy.

In the Democratic Party, such figures as Senator Manchin exercise decisive influence. This was shown by the Senate passage of a Republican-sponsored resolution to strike down Biden’s executive action forgiving $400 billion in student loan debt, despite the Democrats holding a 51-49 majority. Manchin, Montana Democrat Jon Tester and Arizona independent ex-Democrat Kyrsten Sinema all voted for the bill, which Biden was compelled to veto Wednesday.

Confidence lags (again) in Biden's economy

20 Imminent Signs The American Society Is Collapsing

As the world was buffeted by a coronavirus tsunami leaving forced lockdowns, supply-chain problems, economic upheaval, and poverty in its wake, globalist financial elites “have had a terrific pandemic” according to a report released Monday.

The world’s 10 richest men have more than doubled their fortunes to $1.9 trillion, at a rate of $1.6 billion a day, over the past 12 months, proving elites have largely been spared the misery and financial ruin inflicted on so many by endless enforced lockdowns.

A confederation of charities that focus on alleviating global poverty, Oxfam said members of the globalist financial elites saw their wealth rose more during the pandemic more than it did the previous 14 years, when the world economy was suffering the worst recession since the Wall Street Crash of 1929.

THE END OF THE AMERICAN MIDDLE CLASSD

TALKS ABOUT THE GUTTED AMERICAN MIDDLE CLASS

Robert F Kennedy Jr: "We need a peaceful revolution"

As the world was buffeted by a coronavirus tsunami leaving forced lockdowns, supply-chain problems, economic upheaval, and poverty in its wake, globalist financial elites “have had a terrific pandemic” according to a report released Monday.

The world’s 10 richest men have more than doubled their fortunes to $1.9 trillion, at a rate of $1.6 billion a day, over the past 12 months, proving elites have largely been spared the misery and financial ruin inflicted on so many by endless enforced lockdowns.

A confederation of charities that focus on alleviating global poverty, Oxfam said members of the globalist financial elites saw their wealth rose more during the pandemic more than it did the previous 14 years, when the world economy was suffering the worst recession since the Wall Street Crash of 1929.

These are some of the main points from Oxfam’s latest report, Inequality Kills, which has been released as global business leaders meet virtually this week for the World Economic Forum (WEF) in Davos, Switzerland.

“We have a situation where 10 men hold more wealth than that of two-thirds of humanity,” Lyn Morgain, chief executive of Oxfam Australia, told Australia’s ABC news outlet.

“Not only that, but that bottom 40 percent are hanging on by a thread.”

The report highlights what the charity says are “unprecedented” levels of global inequality as coronavirus sharpens the divide between “us and them,” the “haves and have nots.”

Jeff Bezos speaks about his flight on Blue Origin’s New Shepard into space during a press conference on July 20, 2021 in Van Horn, Texas. (Joe Raedle/Getty Images)

Meanwhile the likes of Tesla co-founder Elon Musk, Amazon’s Jeff Bezos, and Facebook’s Mark Zuckerberg, enjoyed the greatest year-on-year growth since records began, the report outlined.

At a time when a group of these men were using their riches to rocket into outer space, the charity said, the World Bank had projected that more than 160 million people had been pushed into poverty.

In all, 20 new “pandemic billionaires” have also been created in Asia thanks to the international response to coronavirus, according to the charity.

Forbes listed the world’s 10 richest men as: Tesla and SpaceX chief Elon Musk, Amazon’s Jeff Bezos, Google founders Larry Page and Sergey Brin, Facebook’s Mark Zuckerberg, former Microsoft CEOs Bill Gates and Steve Ballmer, former Oracle CEO Larry Ellison, U.S. investor Warren Buffet and the head of the French luxury group LVMH, Bernard Arnault.

The Oxfam report follows a December 2021 study by the group which found that the share of global wealth of the world’s richest people soared at a record pace during the pandemic.

Analysis: Joe Biden’s ‘Build Back Better’ Would Make the Rich Even Richer

Sean Gallup/Chip Somodevilla/Jeff Gentner/Drew Angerer/Getty Images

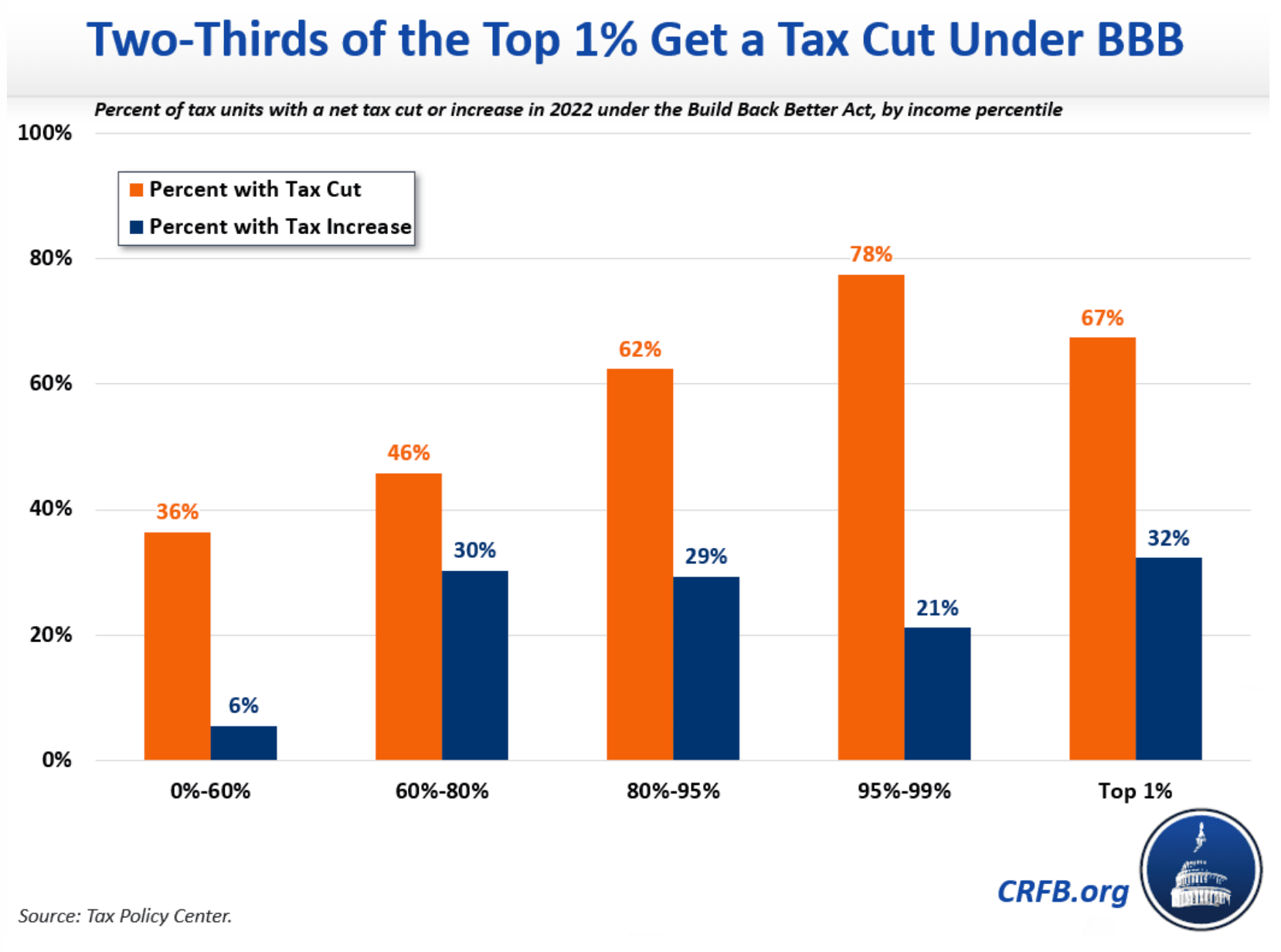

President Joe Biden’s “Build Back Better Act” is set to give a tax cut to about 67 percent of the nation’s richest Americans — those earning more than $885,000 every year.

A new analysis from the Committee for a Responsible Federal Budget reveals that the filibuster-proof reconciliation package will give a tax cut to two-thirds of the top one percent of earners even as the top one percent now hold more wealth than the entire American middle class.

“This is true despite the fact that Build Back Better would raise taxes substantially for the extremely rich (mainly those making over $10 million per year),” the analysis states.

In effect, those in the top one percent would receive an average tax cut of more than $16,000 in 2022 under Biden’s plan. The tax cuts for the wealthy would be a result of the plan’s increasing the State and Local Tax (SALT) deduction cap.

As Breitbart News has reported, the plan amounts to a $625 billion tax cut for the wealthiest of Americans living primarily in blue states.

(Chart via Committee for a Responsible Federal Budget)

“In other words, the largest tax cuts in dollars in Build Back Better would go to households in the top five percent and especially the top one percent,” the analysis continues. “Many make millions of dollars of annual income and tens of millions of dollars in assets.”President Joe Biden’s “Build Back Better Act” is set to give a tax cut to about 67 percent of the nation’s richest Americans — those earning more than $885,000 every year.

A new analysis from the Committee for a Responsible Federal Budget reveals that the filibuster-proof reconciliation package will give a tax cut to two-thirds of the top one percent of earners even as the top one percent now hold more wealth than the entire American middle class.

“This is true despite the fact that Build Back Better would raise taxes substantially for the extremely rich (mainly those making over $10 million per year),” the analysis states.

In effect, those in the top one percent would receive an average tax cut of more than $16,000 in 2022 under Biden’s plan. The tax cuts for the wealthy would be a result of the plan’s increasing the State and Local Tax (SALT) deduction cap.

As Breitbart News has reported, the plan amounts to a $625 billion tax cut for the wealthiest of Americans living primarily in blue states.

“In other words, the largest tax cuts in dollars in Build Back Better would go to households in the top five percent and especially the top one percent,” the analysis continues. “Many make millions of dollars of annual income and tens of millions of dollars in assets.”

At the same time, Biden’s plan would squeeze an extra $200 billion out of American taxpayers by mostly targeting working and middle class earners with more Internal Revenue Services (IRS) audits.

The plan ensures nearly 600,000 more working and middle class Americans earning $75,000 or less a year would be audited by the IRS. Of those new IRS audits, more than 313,000 would target the poorest of Americans who earn $25,000 or less a year.

Biden’s “Build Back Better Act” has already passed the House, thanks entirely to Democrat support, and now awaits scrutiny in the United States Senate.

In 2017, former President Trump had the SALT deduction capped at $10,000. Since then, Democrats have sought to deliver their wealthy, blue state donors with a massive tax cut by eliminating the cap altogether or greatly increasing it.

Biden, for instance, had sought to include tax cuts for his billionaire donors in a Chinese coronavirus relief package earlier this year. The plan was ultimately cut from the package. House Speaker Nancy Pelosi (D-CA), in May 2020, also tried to include the plan in a coronavirus relief package.

John Binder is a reporter for Breitbart News. Email him at jbinder@breitbart.com. Follow him on Twitter here.

When nations die, they do so with surprising speed. Ernest Hemingway made a similar observation when a person in his novel was asked how he went bankrupt, and his reply was, "Gradually, then suddenly."

Nations are built upon classical values — perseverance, self-reliance, and honor. A great nation is one whose values have made it unusually prosperous. In its latter days, the nation becomes hollowed out and burdened with a costly, top-heavy government. The middle class is expected to provide generosity to the masses. Over time, traditional values fade away, and everyone seeks to live off everyone else.

The United States shows aspects of a once great power past its prime. It is socially and politically divided, aware of the necessity for changes, unable or unwilling to make them, and losing the conviction in the shared goals that earlier invigorated it.

The decay that started gradually decades ago is now metastasizing at warp speed. The United States, ripped apart internally, has become ever less willing and able to lead internationally. The doctrines that built the United States and Western civilization, assimilated from ancient cultures over thousands of years, are being methodically dissolved. America is entering an uncharted, revolutionary time. The foundation of American life, abundant food, energy autonomy, a sound economy, sound education at all levels, and enforceable and equal application of the law, are eroding.

Our society is "fundamentally changing," and these changes are not for the better. Hard-left fanatics have absorbed the Democrat party and are transforming the country with woke and equality-of-result agendas. Prosperity and leisure have misled a complacent society into thinking the modern age no longer needs to worry about law and order.

As we recoil from spontaneous street violence and looting, Americans are coming to learn just how degraded the foundations of their society have become. Criminals walk out with stolen merchandise without fear of the law or even the outrage of witnesses. Defunding the police has discharged a torrent of criminals into the streets. Downgrading felonies, no cash bail, and no jail time are spiking violent crime. Lawlessness has become a political matter where race, ideology, and politics decide how the law will be enforced.

At the border, millions of people enter our country illegally. Joe Biden is shamefully welcoming an unvetted third-world population into our country to dilute and displace native-born Americans. No country can exist without a border, much less allow foreign crime cartels to control it while killing 100,000 citizens with drugs yearly.

The FBI is more likely to go after parents at school board meetings than those threatening the homes of Supreme Court justices. CIA and FBI directors lie under oath without consequence. They mislead the public and deceive Congress with stories of fake dossiers. They contract private news organizations to censor stories they do not like and writers whom they fear. And the IRS is weaponized against political opponents of the Democrats.

Possibly a million homeless people now live on our streets. Our major cities are cesspools of human filth with open sewers, garbage-strewn streets, and drugged out drifters.

Grocery shelves are increasingly bare, and many food items are now beyond people's budgets. Fuel costs are reaching record levels, new cars and homes are unaffordable, and inflation is at a 40-year high. The necessary medicine of high interest rates to bring down inflation is nearly as painful as the inflation itself.

The federal government spends $1.29 for every dollar in tax revenues it receives, and a quarter of IRS revenues are now needed to cover interest payments on the debt. Economic doom, market collapse, and bank runs are not far from people's minds.

China is leading BRICS countries to replace the dollar's standing as the world's reserve currency. Any success they attain will lessen demand for dollars and possibly collapse the dollar's exchange rate.

Moreover, the Chinese Communist Party authorities think they have a chance to bolster their power and change the world order in their favor. Because China's broad geopolitical interests are on the rise, a pressing question is how to check China's ambitions at a time of division and discord in America. China's current foreign policy could not happen without its substantial military forces and three-decades-long economic growth, underwritten by its exports to America.

Sensing American weakness, the CCP may invade Taiwan before Joe Biden leaves office. Are the American people willing to fight over Taiwan or freedom of navigation issues near Chinese-claimed islands? What are we truly ready to fight for? When that happens, are we prepared for economic devastation to the U.S. and the world? Meanwhile, thousands of Chinese sleeper agents are crossing our open southern border to cause mayhem when called upon to do so.

Today's threat arises from a disintegrating world order. More than at any other recent time, many dangerous intersecting events are happening at a time when the United States is unprepared to deal with them.

And it all culminates with the elections in November 2024. Democrats can win only by cheating, and since they did it successfully in 2020, you can expect them to do it again. While some election integrity measures have been increased in some states, almost nothing has been done anywhere to require open-source computer programming code of voting machines so we can be assured they are counting votes correctly. Moreover, nothing has been done to prevent voting machines from being hacked to alter election outcomes. At this point, the left has become brazenly indifferent as to whether anyone even knows of its cheating. Court challenges almost always go the leftists' way.

Regardless of who is declared the winner, there will be unrest. There could be a breakdown in civil order nationwide. If the left loses, leftists will riot and loot in a replay of the 2020 BLM riots. If the right loses, this will be a turning point, as we can't go on being lied to and threatened by the left. Another stolen election will break our country.

The decay that began slowly long ago is now upon us in full force. The only election historically comparable to 2024 was in 1860, and that one was followed by a civil war. We must defend our freedom and our country and protect it with everything we have or lose it all. We must be involved and understand that if we lose the election in 2024, America, as we know it, is over. To save the nation, all constitutionally minded Americans must see the danger and gird themselves for what lies ahead.

Jeff Lukens is a West Point graduate, U.S. Army veteran, and conservative activist. He can be reached at jplukens@hotmail.com.

ONE WILL NOT HEAR THE WORD 'HOMELESS' OUT OF THE LYING BRIBES SUCKING MOUTH OF JOE BIDEN!

The number of foreign nationals holding jobs in the United States has hit the highest level since the Labor Department began tracking the data in 1996 as the employment of native-born Americans declines, a trend under President Joe Biden.

In 2022, foreign-born workers saw their share of the labor market hit the highest level in almost 30 years at more than 18 percent, with close to 30 million now holding U.S. jobs, according to data published in the Wall Street Journal.

Even though it has gone virtually unreported by corporate media, BreitbartNews has extensively documented the Clintons’ longstanding support for “open borders.” Interestingly, as the LosAngelesTimes observed in 2007, the Clinton’s praise for globalization and open borders frequently comes when they are speaking before a wealthy foreign audiences and donors.

How Elites Will Create a New Class of Slaves | Whitney Webb |

Nearly a quarter of a million people 55 or older are estimated by the government to have been homeless for at least part of 2019.

According to the Washington Post, “People 55 and older represented 16.5 percent of America’s homeless population of 1.45 million in 2019, according to the most recent reliable data.”

According to a 2022 University of Pennsylvania Study by Rebecca Brown, an Assistant Professor of Medicine in the Division of Geriatric Medicine at the Perelman School of Medicine, and several coauthors from the University of California San Francisco, over one-third of the homeless population are now single adults over 50, triple the figure in 1990 when it stood at 11 percent.

The government makes little effort to count the homeless. The Department of Housing and Urban Development, the only federal source of information on homelessness disaggregated by age, delayed its release of the second part of their Annual Homeless Assessment Report to Congress by two years, making it difficult to get an idea of the scale of homelessness among the elderly in real time.

The latest information on homelessness with respect to the elderly is from 2019, though advocates of the homeless have noted that there is evidence that it is growing, pointing to numerous examples.

The largest shelter provider in Arizona, Central Arizona Shelter Services (CASS), is rushing to open an over-55 shelter in a former Phoenix hotel this summer with “private rooms and medical and social services tailored for older people.” The provider says that it served 1,717 elderly in 2022, a 43 percent increase compared to 2021.

In Orange County, California, a Medicaid plan, CalOptima Health, is creating a 119-bed shelter which will serve as an assisted-living facility for the elderly, according to Kelly Bruno-Nelson, executive director for the plan. Bruno-Nelson stated that the current shelter system “cannot accommodate the physical needs of this population.” Seniors are staying in respite centers for months in San Francisco, California, Portland, Oregon, and Anchorage, Alaska, that were intended for a short-term stay only. In Boise, Idaho, shelter operators are hiring staff with backgrounds in long-term care to help elderly homeless living for long periods in hotels.

“It’s just a catastrophe. This is the fastest-growing group of people who are homeless,” said Dr. Margot Kushel, a professor of medicine and vulnerable populations researcher at the University of California at San Francisco.

Elderly homeless contract chronic diseases much earlier than younger people, as well as suffering from geriatric problems. Poor access to care due to homelessness, and the threat of having their medications stolen or going bad outside, stress from having to weather the outdoors, as well as generally unsanitary conditions, and the difficulties created by the anti-homeless laws being passed around the country, all contribute to poor health outcomes.

A Journal of the American Medical Association study titled, “Factors Associated With Mortality Among Homeless Older Adults in California: The HOPE HOME Study,” detailed how, over an average of 55 months, unhoused people over 50 years died at a rate 3.5 times greater than their housed counterparts. The findings are consistent with previous studies in other parts of the country.

Dennis Culhane, a professor and social science researcher at the University of Pennsylvania, said that the population of homeless seniors 65 and older would double or even triple from 2017 before peaking around 2030.

This increase is driven by poverty. One half of renters over 50 spend more than 30 percent of their household income on rent, according to the Joint Center for Housing Studies of Harvard University.

As the American Society on Aging Generations journal noted, “Low-income people who spend more than 30 percent of their income on rent are unable to save money, leaving them vulnerable to losing their housing when they face setbacks, such as a job loss, sickness, or death of a spouse or partner.”

In other words, homelessness is a class issue. The financial elite that both parties represent, and the upper middle class have no reason to worry about becoming homeless. The workers on the other hand, such as the homeless former autoworker that the Post interviewed, are the ones which this malady overwhelmingly affects.

overty, combined with the bipartisan destruction of the social safety net, spiraling inflation driven by profit-gouging (not wages) and the US-provoked war with Russia, as well as extortionary rent, are leading to thousands of the elderly being kicked out onto the streets.

The ruling class has no response to the increase in homelessness among the elderly. Indeed, hardly any media coverage is to be found on the topic. As it doesn’t fit into the categories of race or gender, the Democratic Party wing of the political establishment finds it more convenient to merely remain quiet on the topic.

The plans to attack Medicare and Social Security under the phony pretense of fighting debt, while dumping literally over a trillion dollars into American imperialism’s war machine—not to mention the nearly unlimited bailouts sunk into the pockets of the financial elite—shows the real disdain for the elderly.

If anything, the response given by the ruling elite is to step up the attacks on the elderly, foster reactionary sentiments against them (as a burden to society and the young), and ultimately to reduce life expectancy.

The corporate media has railed against the elderly, endorsing dying early. This was visible in the campaign for the pro-corporate health plan Obamacare (the Affordable Care Act) in which the New York Times spearheaded this narrative. The result of Obamacare was to contribute to a decrease in life expectancy. One of the chief architects of Obamacare, Dr. Ezekiel Emanuel, openly advocated for a reduction in life expectancy.

The aim of the ruling class is to extract as much profit from workers as possible while they are of working age and then for them to die quickly so they don’t subtract from profits and funds for warfare. Putting the elderly out on the streets will contribute to a higher mortality rate. It is another indication of the bankruptcy of capitalism that it is not just incapable of preserving life for the elderly, but actively hostile to it.

The Greatest Retirement Crisis In US History Is A Looming Catastrophe For 47 Million Americans

The greatest retirement crisis in U.S. history has already begun, and official agencies are warning about the looming catastrophe that is about to hit older Americans. Without enough savings or assets, 80% of households with older adults are at risk of falling into economic insecurity as they age. But don’t be mistaken -- the impact on younger generations will be just as disastrous, they say. With seniors staying longer in the workforce to be able to make ends meet, younger workers are losing precious opportunities to advance their careers and start saving for retirement, too. A new analysis by Fidelity Investments exposes that this snowballing crisis is going to lower everyone’s standard of living over the next few years and continue to widen the inequality gap that is leaving each generation a little poorer than the one before. According to Ronald P. O'Hanley, the firm’s president of asset management and corporate services, millions of older Americans are now headed for destitute financial futures and old ages spent in poverty. "I'm not sure what would be worse," he continued, "millions of elderly unable to house and feed themselves, or the intergenerational strife that surely would erupt if young people are forced to lower their standard of living to pay for our failure to act in a timely manner to avert this crisis." Fidelity data shows that today, 40% of retiree households do not have sufficient income to cover their monthly expenses, O'Hanley said. "Well over half of all Americans have less than $25,000 in total savings, not counting the value of their primary residence or pension plans. And 28 percent have put aside less than $1,000." A recent survey from the American Advisors Group detailed that 47% of seniors rated the conditions of their retirement savings as poor and 44% said they had not saved enough to retire comfortably. At the same time, 62% of adult children are worried that the cost of living crisis is impacting their parent's retirement savings, with many (35%) worried they'll have to help their senior parents financially. Amid this anxiety over whether their parents will have enough retirement savings, a growing number of adults are planning about using their parents' home equity as a financial solution, the survey said. However, only 18% of those 62 and older would benefit from using their home equity to pay for long-term care and other expenses, should the need arise. The remaining 82% may actually not have enough home equity to cover these costs due to the ongoing correction in housing prices and the economic recession that is upon us. For that very reason, about a third of Americans over traditional retirement age, between 65 and 74, are expected to be still working in 2030. The increase in older workers staying on their jobs is causing concerns amongst business owners, too because employers have been expecting their expensive older workers to retire which would open senior-level jobs for younger workers looking to advance their careers. In other words, the current retirement crisis is reaching such alarming proportions that other generations are missing key opportunities to become financially independent, debt-free, and able to build wealth to afford their own retirements when the time arrives. This is going to create major distortions in our economy and continue to impoverish younger Americans, who may never enjoy the same standard of living their parents and grandparents once had. At the end of the day, this crisis is going to impact each and every one of us as it erodes our quality of life and delays our collective growth.

DeSANTIS VOWS TO PUSH THE MEXICAN DRUG CARTELS OUT OF AMERICA'S UNDEFENDED BORDER

Ron DeSantis: The FBI and DOJ have been weaponized against Americans

A flooded labor market from mass immigration has had a devastating impact on working- and middle-class Americans, while redistributing billions in wealth to the top one percent of earners and big business. While creating an economy that tilts in favor of employers, the mass immigration economic model has helped keep wages stagnant for decades. JOHN BINDER

"This is how they will destroy America from within. The leftist billionaires who orchestrate these plans are wealthy. Those tasked with representing us in Congress will never be exposed to the cost of the invasion of millions of migrants. They have nothing but contempt for those of us who must endure the consequences of our communities being intruded upon by gang members, drug dealers and human traffickers. These people have no intention of becoming Americans; like the Democrats who welcome them, they have contempt for us." PATRICIA McCARTHY

Records: Son of Billionaire Democrat Donor George Soros Has Visited the White House 14 Times

Hungarian Prime Minister Viktor Orbán warned that the Soros empire, the reigns of which will be handed over to 37-year-old scion Alexander, is planning to “incite” another migrant crisis in Europe.

In his weekly radio appearance, Hungarian Prime Minister Viktor Orbán said according to 24.hu that he believed that the latest migrant relocation scheme from the European Union was a result of pressure from George Soros’ son Alex, who is set to take over the $25 billion financial empire.

Orbán, who has long maligned the mal-influence of the 92-year-old Hungarian billionaire in his country and elsewhere, warned that his heir may be more ruthless in achieving the goals of the ‘Open Society’ foundations owned by the family.

The EU migration deal, which was reached earlier this month, was opposed by Hungary and Poland, with both countries objecting to accepting migrants who entered other countries. Under the parameters of the plan, EU member states would either have to accept a number of relocated asylum-seekers per year or pay €20,000 for each migrant refused.

According to Orbán, the plan would see some 8,500 migrants forced onto Hungary, however, the populist leader has so far maintained that he has no intention of abiding by the diktats from Brussels.

The Hungarian leader said that he believed the reason why the deal was struck, seemingly out of nowhere, was as a result of a lobbying effort from Alex Soros, whom he said “dictates an even tougher pace” than his father and that Hungary should prepare for the Soros family to ” incite the migrants, and increase the pressure on Hungary’s southern border.”

“One could say that the Soros empire has struck back, something that’s been forced down the throats of the majority of Europeans,” Mr Orbán said.

On Monday, George Soros announced that he would be handing over the reins of his empire to his son, 37-year-old Alexander “Alex” Sorors. For his part, Alex Soros has claimed to be “more political” than his globalist financier father.

In an interview this week with the Wall Street Journal, Soros said that he would continue to pursue hard-left policies on issues such as abortion, voting, and gender equality.

Following the announcement of the handover, Orbán was quick to respond, posting a gif on his Twitter account from The Godfather, showing Vito Corleone kissing his son Micheal, along which the Hungarian leader wrote: “Soros 2.0”.

In his Friday radio appearance, Orbán went on to accuse George Soros of acting as a “war speculator” and trying to stymie attempts from figures such as himself to peacefully negotiate an end to the war in Ukraine.

This was the reason why the Soros family, he claimed, is attacking former U.S. President Donald Trump “with all its means,” given Trump’s persistent calls for peace talks between Moscow and Kyiv.

“The pro-war camp [is] attacking with full force. That’s what you get nowadays if you’re on the side of peace. Keep on fighting, Mr. President! The world needs you, the world needs peace,” Orban said to Mr Trump on Friday following the latest arrest of the former president.

Follow Kurt Zindulka on Twitter:or e-mail to: kzindulka@breitbart.com

‘Spider-Man: Across the Spider-Verse’ Teams with Soros-Backed American Immigration Council

Sony’s animated blockbuster Spider-Man: Across the Spider-Verse has released an ad in partnership with a George Soros-backed group whose goal is to import more cheap immigrant labor.

The American Immigration Council (AIC) is taking credit for the PSA — but instead of mentioning immigration, the Hollywood partnership is being marketed as a plea for “belonging,” with the goal of creating a “more welcoming nation.”

The Spider-Man tie-in consists of a 30-second video featuring characters from the hit sequel accompanied by a voice-over urging greater acceptance of others.

“It doesn’t take a superhero to bring forces together. We all have the power to reach out and help someone feel like they belong,” the narrator says.

Watch below:

Spider-Man is partnering with a group called Belonging Begins with Us, which is a project of AIC — the Soros-backed organization that is trying to flood the country with cheap labor by pushing for more immigration as well as amnesty for some illegal aliens.

Belonging Begins with Us works with the Ad Council to partner with prominent brands and entertainment titles in an attempt to push its soft message of “belonging” and “welcoming.”

“Belonging” has emerged as a key marketing buzzword for the AIC, which defines it as a “fundamental human need, and one that is linked to many of the most complex challenges of our time.” The organization has even published a study titled “The Belonging Barometer,” which calls for greater acceptance of “non-citizen immigrants” and other groups.

“The Americans who report being treated as ‘less than’ tend to be younger, first-generation or non-citizen immigrants, identify as non-Hispanic white, or identify as a gender minority,” the study concludes. “The range of demographic categories who reported being treated as ‘less than others.'”

The Hollywood push comes amid falling support for immigration, as the Biden administration’s open-border policies have resulted in an unprecedented tsunami of illegal border crossings.

As Breitbart News reported, a YouGov poll found a growing plurality of citizens alongside almost two out of three Republicans say immigration makes the nation “worse off.”

Spider-Verse 2, which is a Marvel Studios production, is poised to become one of the biggest movies of the summer. The sequel has so far grossed $225 million domestically and is in the midst of its global rollout.

The Soros network may go through a shakeup in the coming years, as the infamous left-wing billionaire has handed over the reins of his activism-charity projects to his millennial son Alex.

President Joe Biden’s “Build Back Better Act” is set to give a tax cut to about 67 percent of the nation’s richest Americans — those earning more than $885,000 every year.

A new analysis from the Committee for a Responsible Federal Budget reveals that the filibuster-proof reconciliation package will give a tax cut to two-thirds of the top one percent of earners even as the top one percent now hold more wealth than the entire American middle class.

“This is true despite the fact that Build Back Better would raise taxes substantially for the extremely rich (mainly those making over $10 million per year),” the analysis states.

In effect, those in the top one percent would receive an average tax cut of more than $16,000 in 2022 under Biden’s plan. The tax cuts for the wealthy would be a result of the plan’s increasing the State and Local Tax (SALT) deduction cap.

As Breitbart News has reported, the plan amounts to a $625 billion tax cut for the wealthiest of Americans living primarily in blue states.

(Chart via Committee for a Responsible Federal Budget)

“In other words, the largest tax cuts in dollars in Build Back Better would go to households in the top five percent and especially the top one percent,” the analysis continues. “Many make millions of dollars of annual income and tens of millions of dollars in assets.”President Joe Biden’s “Build Back Better Act” is set to give a tax cut to about 67 percent of the nation’s richest Americans — those earning more than $885,000 every year.

A new analysis from the Committee for a Responsible Federal Budget reveals that the filibuster-proof reconciliation package will give a tax cut to two-thirds of the top one percent of earners even as the top one percent now hold more wealth than the entire American middle class.

“This is true despite the fact that Build Back Better would raise taxes substantially for the extremely rich (mainly those making over $10 million per year),” the analysis states.

In effect, those in the top one percent would receive an average tax cut of more than $16,000 in 2022 under Biden’s plan. The tax cuts for the wealthy would be a result of the plan’s increasing the State and Local Tax (SALT) deduction cap.

As Breitbart News has reported, the plan amounts to a $625 billion tax cut for the wealthiest of Americans living primarily in blue states.

“In other words, the largest tax cuts in dollars in Build Back Better would go to households in the top five percent and especially the top one percent,” the analysis continues. “Many make millions of dollars of annual income and tens of millions of dollars in assets.”

At the same time, Biden’s plan would squeeze an extra $200 billion out of American taxpayers by mostly targeting working and middle class earners with more Internal Revenue Services (IRS) audits.

The plan ensures nearly 600,000 more working and middle class Americans earning $75,000 or less a year would be audited by the IRS. Of those new IRS audits, more than 313,000 would target the poorest of Americans who earn $25,000 or less a year.

Biden’s “Build Back Better Act” has already passed the House, thanks entirely to Democrat support, and now awaits scrutiny in the United States Senate.

In 2017, former President Trump had the SALT deduction capped at $10,000. Since then, Democrats have sought to deliver their wealthy, blue state donors with a massive tax cut by eliminating the cap altogether or greatly increasing it.

Biden, for instance, had sought to include tax cuts for his billionaire donors in a Chinese coronavirus relief package earlier this year. The plan was ultimately cut from the package. House Speaker Nancy Pelosi (D-CA), in May 2020, also tried to include the plan in a coronavirus relief package.

John Binder is a reporter for Breitbart News. Email him at jbinder@breitbart.com. Follow him on Twitter here.

Here's What We Know About Alex Soros, Progressive Scion Taking Over His Father's Political Empire

The Democratic megadonor George Soros has ceded control of his political empire to his son, Alexander Soros.

The succession plan was revealed Sunday, in a Wall Street Journalprofile of the 37-year-old Soros scion. All eyes are now on Alex Soros as he prepares to take his father's place atop the country’s most powerful progressive political operation.

Here's what we know about the younger Soros.

He's ‘More Political’ Than His Pops

The younger Soros says he is "more political" than his 92-year-old father, the Democratic Party’s biggest donor.

Alex Soros has given tens of millions of dollars to Democrats over the years. He contributed $5.25 million to the Senate Majority PAC in 2016 and 2018. He contributed $721,300 to the Biden Victory Fund in 2020 and $350,000 to Hillary Clinton’s victory fund in 2016. Soros has given millions more to the DNC and other Democratic committees.

Alex Soros has not contributed as much to other political advocacy groups as his father has over the years. George Soros, through his Democracy PAC and Democracy PAC II, has contributed tens of millions of dollars to traditional political committees, as well as to advocacy groups like Planned Parenthood, MoveOn, and American Bridge. Both Soroses have contributed this election cycle to moderate Democratic senator Jon Tester (Mont.), considered one of the most vulnerable incumbents in 2024.

The elder Soros has also funded a network of left-wing prosecutors whose soft-on-crime policies have been blamed for surging crime and low police morale. In 2018, Alex Soros contributed $100,000 to help elect Minnesota attorney general Keith Ellison, a progressive Democrat who faced allegations of domestic abuse and blamed police for damage sustained during the George Floyd riots.

His Money Opens Democratic Doors

Alex Soros’s extensive campaign giving appears to open doors for him to many senior Democratic lawmakers.

The younger Soros huddled with Vice President Kamala Harris last week and declared he was "Ridin’ with Biden" in a recent photo with President Biden. He has rubbed shoulders with former House Speaker Nancy Pelosi, Senate Majority Leader Chuck Schumer, and former President Barack Obama, according to his social media feeds.

He Spends A Lot of Time At the Biden White House

Alex Soros also appears to have open access to the White House, having visited at least 17 times during Biden’s tenure, according to visitor logs.

Most of those meetings have been with Biden’s political and domestic policy advisers, but Soros has had five meetings with Jon Finer, the principal deputy national security adviser.

The Washington Free Beaconreported that Soros met with Finer on the same day that Brazilian president Luiz Inácio Lula da Silva visited the White House. According to the Wall Street Journal, Soros met the left-wing Brazilian leader to advocate on behalf of the Open Society Foundations, his father’s philanthropy.

He Runs His Father's Left-Wing Nonprofit

Alex Soros took over in December as chairman of the board of Open Society Foundations, which pours hundreds of millions of dollars annually into progressive causes in the United States and around the world.

Alex Soros told the Journal he plans to use Open Society’s $25 billion war chest to fund the expansion of abortion and voting rights across the country.

He Lacks Dad's Business Savvy

Alex Soros does not appear to have his father’s business acumen, raising questions about the long term viability of his political empire. George Soros has amassed a fortune of around $7 billion, largely through his Soros Fund Management hedge fund.

Jonathan Soros, Alex’s older half-brother, was initially seen as the heir apparent to his father’s business and political empire, but the pair had a falling out over management style.

Alex Soros is an adviser to an apparel supply chain fund, Tau Management, funded by his father. Tau invests in apparel and textile factories in Asia in order to build "agile, sustainable manufacturing partners" to major apparel brands. The fund requires its partners to have a "strong and sincere commitment to [Equity, Sustainability, Governance]."

He Just Wants to Party

Before his ascent to the top of his father’s political empire, Alex Soros was better known for his semi-playboy lifestyle. According to the New York Post, Soros hosted celebrities at a $72 million Hamptons estate he rented in 2016, and has often been spotted hanging out with NBA players and supermodels.

Soros reportedly hired New York City club promoter Adam Spoont to recruit models to attend Soros’s house parties. Spoont’s success landed him an invitation to an Alex Soros fundraiser, where he was able to meet President Obama, according to Page Six.

His Father Has Been Accused of Domestic Abuse

George Soros on the beach / Splash News

The elder Soros's ex-girlfriend, Brazilian model Adriana Ferreyr, says Alex's dad once slapped and choked her while they were in bed. Ferreyr later sued George Soros for $50 million.

He pissed off Taylor Swift

Alex Soros led a consortium of investors who bought rights to Swift’s unreleased music for $330 million, drawing the ire of the pop superstar.

"It looks to me like Scooter Braun and his financial backers, 23 Capital, Alex Soros, and the Soros family and The Carlyle Group, have seen the latest balance sheets and realized that paying $330 million for my music wasn't exactly a wise choice and they need money," Swift said in 2020. "In my opinion, just another case of shameless greed in the time of Coronavirus. So tasteless, but very transparent."

In truth, the Golden State is becoming a semi-feudal kingdom, with the nation’s widest gap between middle and upper incomes—72 percent, compared with the U.S. average of 57 percent—and its highest poverty rate. Roughly half of America’s homeless live in Los Angeles or San Francisco, which now has the highest property crime rate among major cities.

The costs of illegal immigration are being carefully hidden by Democrats. MONICA SHOWALTER

California approves ‘shocking’ policy giving weekly checks to migrants: Report

Migrant enclaves already are at the top of the U.S. lists for bad places to - 10 of the 50 worst places in America to live according to this list are in California, and all of them are famous for their illegal populations. MONICA SHOWALTER

House GOP Report: Illegal Aliens Costing American Hospitals Billions in Unpaid Medical Bills

Illegal aliens released into the United States interior are costing American taxpayers, and the public hospitals they help fund, billions in unpaid medical bills every year, a report from Republicans on the House Homeland Security Committee details.

The report, wherein Chairman Mark Green (R-TN) notes the failures of President Joe Biden’s Department of Homeland Security (DHS) Secretary Alejandro Mayorkas, revealed the extent to which illegal immigration wreaks havoc on the nation’s hospitals intended to provide first-class care for Americans and legal immigrants.

“Hospital and emergency room care for illegal aliens is one of the most significant expenses,” the report states, mentioning that illegal aliens typically have no form of health insurance and therefore rely especially on emergency room services for free care.

“Consequently, this has led to significant costs for hospitals because providers are often not reimbursed for these services,” the report states:

In a January 2021 filing challenging the Biden administration’s deportation moratorium, Texas Attorney General Ken Paxton wrote that his state alone was required to pay anywhere between $62- 90 million per year to cover illegal aliens under its Emergency Medicaid program. [Emphasis added]

He also pointed out that between 2006-2008, uncompensated costs borne by Texas state hospitals providing care to illegal aliens ranged from $597 million to $717 million. That’s as much as $1.03 billion in May 2023 dollars. [Emphasis added]

In Florida, for Fiscal Year 2021, illegal aliens cost state hospitals about $312 million. Meanwhile, in Illinois, a statewide healthcare benefits program for illegal aliens has ballooned from a projected $2 to $4 million cost to what has now become a $1.1 billion program for taxpayers.

Locally, in Yuma, Arizona, executives with the Yuma Regional Medical Center said that in just one year, taxpayers were left with $26 million in unpaid medical bills from illegal aliens who showed up to the hospital requesting free care.

“Some migrants come to us with minor ailments but many of them come in with significant disease. We have had migrant patients on dialysis, cardiac catheterization and in need of heart surgery,” Dr. Robert Trenschel, CEO of the hospital, previously told the House Homeland Security Committee. “Many are very sick. They have long-term complications of chronic disease that have not been cared for. Some end up in the ICU for 60 days or more.”

One of the main strains on the hospital is pregnant illegal aliens arriving with little-to-no prior prenatal care, putting them at high risk for potentially serious complications which results in longer, costly stays at the hospital.

The issue has been raised by more than just House Republicans.

Most recently, Democrat presidential candidate Robert F. Kennedy Jr. visited the U.S.-Mexico border to warn of the massive waves of illegal immigration that are straining the nation’s security and social safety net resources.

During his visit, Kennedy said he talked to local officials in Arizona who explained that their hospitals’ maternity wards are so packed with pregnant illegal aliens that American women are having to reschedule their delivery dates.

“Moms occupied 32 of 36 beds in Yuma hospital maternity ward so that local moms had to delay induced pregnancies for two weeks,” Kennedy wrote in a Twitter post.

Months ago, the Federation for American Immigration Reform reported that illegal immigration costs the nation’s hospital systems at least $23 billion annually — $8.2 billion of which is uncompensated medical care for illegal aliens.

John Binder is a reporter for Breitbart News. Email him at jbinder@breitbart.com. Follow him on Twitter here.

Biden’s DHS Rewards Sanctuary Cities, NGOs with $290M for Resettling Illegal Aliens in U.S.

Ting Shen/Bloomberg/GUILLERMO ARIAS/AFP via Getty Images

President Joe Biden is rewarding sanctuary cities and non-governmental organizations (NGOs) with more than $290 million in taxpayer money for resettling border crossers and illegal aliens across the United States.

Biden’s Department of Homeland Security (DHS) is taking the millions in taxpayer money from the Shelter and Services Program (SSP) — a federal initiative launched by the administration and funded by Congress.

This week, DHS officials announced that more than $290 million from SSP had been rewarded to various towns and cities, many of which are sanctuary jurisdictions, along with NGOs like Catholic Charities and United Way for helping resettle hundreds of thousands of border crossers and illegal aliens across American communities after their release into the nation’s interior.

In total, 34 cities, towns, and NGOs are getting the millions in federal funds.

Many of the cities are sanctuary jurisdictions. For example, San Diego County, California, a sanctuary jurisdiction, is set to secure more than $15 million in SSP funds, while the sanctuary city of Denver, Colorado, will receive more than $8.6 million.

The sanctuary city of New York City is securing the largest amount of SSP funds, more than $104 million, to aid border crossers and illegal aliens, while the sanctuary city of Chicago has scored more than $10.5 million and the sanctuary state of Illinois will get nearly $19.4 million.

The World Hunger Ecumenical Arizona Task Force (WHEAT), an NGO based in Arizona, is set to get $15.5 million to help border crossers and illegal aliens across the state and Catholic Charities, across California and Texas, will rake in more than $24 million in SSP funds.

Last month, Reps. Jim Jordan (R-OH) and Lance Gooden (R-TX) requested a full accounting by the Biden administration in regard to federal funds being rewarded to cities and NGOs that are aiding illegal immigration in the U.S.

“The surge of illegal immigration, fueled in part by NGOs like those on the [Emergency Food and Shelter Program] National Board is unsustainable and unfair to law-abiding citizens and immigrants alike,” Gooden said.

Illegal immigration imposes an enormous burden on American taxpayers.

Annually, the 11 to 22 million illegal aliens living in the U.S. costs taxpayers more than $143 billion. That amount, though, does not include any of the social and economic costs — such as higher housing prices, depleted wages, lost jobs, increased crime, and strained public resources at hospitals and schools — associated with illegal immigration.

John Binder is a reporter for Breitbart News. Email him at jbinder@breitbart.com. Follow him on Twitter here.

WATER MILL, NY - JULY 29: Alex Soros attends The 24th Annual Watermill Center Summer Benefit & Auction at The Watermill Center on July 29, 2017 in Water Mill, New York. (Photo by Jared Siskin/Patrick McMullan via Getty Images)")

No comments:

Post a Comment