1:39

U.S. stocks moved sharply lower Wednesday, led by a deep downturn in tech stocks.

The tech-heavy Nasdaq Composite plunged 4.4 percent. Semiconductor stocks were some of the worst performers following weak earnings news from AT&T and Texas Instruments.

The S&P 500 slid by about 3.1 percent, erasing all of its gains for the year. The Dow Jones Industrial Average fell 608 points, or 2.4 percent. It too erased all of its gains for 2018.

Despite signs of weakness in the housing market, the U.S. economy appears to be very strong. Analysts attributed Wednesday’s sell-off to fears of economic weakness around the globe that could reduce demand for the products and services from U.S. companies.

The market initially appeared to take in stride the news that several prominent Democratic politicians had been sent mail bombs. The Dow opened up in the morning. But the sell-off accelerated later in the day, perhaps as word spread that the bombs could be part of an international terrorist strike against the U.S. Several people noted on Wednesday that one of the images of the bombs appeared to bear the likeness of an ISIS flag.

Stocks have been shaky for weeks as investors have worried about global growth, potential impacts from trade disputes, and the Fed’s determination to raise interest rates. On Tuesday, White House economic adviser Larry Kudlow said stocks were under pressure because investors feared the Democrats would gain more power in the midterm elections.

now watch the globalist billionaires and their criminal banksters come out just fine after the next "recession".

|

Stock bubble bigger than 2008 & coming crash far larger, warns Peter Schiff

Wall Street and the US economy are on the verge of recession, according to the CEO of Euro Pacific Capital, Peter Schiff, who has raised alarms after this week’s market selloff.

“This is a bubble not just in the stock market, but the entire economy,” he told Fox News. Schiff predicts a recession, accompanied by rising consumer prices, that will be “far more painful” than the 2007-2009 Great Recession.

“I think as Americans lose their jobs, they are going to see the cost of living going up rather dramatically, and so this is going to make it particularly painful,” he said.

Stock markets sank on Wednesday and Thursday, led by a steep decline in tech shares and worries of rapidly rising rates which made investors flee the risky stocks.

Both the Dow Jones Industrial Average and S&P 500 posted their biggest one-day drops since February. The Nasdaq notched its largest single day sell-off since June 2016.

US President Donald Trump has blamed the central bank for the selloff, saying the Federal Reserve “has gone crazy.”

According to Schiff, the Fed has been acting irrationally for a long time: “What is crazy is for the Fed to believe that they can raise interest rates without pricking their own bubble.”

Schiff added: “All bear markets start off as corrections. I think this one is probably a bear market. It’s long overdue. This is a bigger bubble than the one that blew up in 2008, and the crisis that is going to ensue is going to be far larger.”

THE OBAMA – CLINTON – GLOBALIST CONSPIRACY: Finish off the middle-class and build a “cheap” labor Mex servant class.

“Our entire crony capitalist system, Democrat and Republican alike, has become a kleptocracy approaching par with third-world hell-holes. This is the way a great country is raided by its elite.” ---- Karen McQuillan THEAMERICAN THINKER.com

Obama Is Making You Poorer—But Who’s Getting Rich?

Goldman Sachs, GE, Pfizer, the United Auto Workers—the same “special interests” Barack Obama was supposed to chase from the temple—are profiting handsomely from Obama’s Big Government policies that crush taxpayers, small businesses, and consumers. In Obamanomics, investigative reporter Timothy P. Carney digs up the dirt the mainstream media ignores and the White House wishes you wouldn’t see. Rather than Hope and Change, Obama is delivering corporate socialism to America, all while claiming he’s battling corporate America. It’s corporate welfare and regulatory robbery—it’s OBAMANOMICS TO SERVE THE RICH AND GLOBALIST BILLIONAIRES.

NEW YORK — In the midst of a public relations nightmare, former White House Deputy National Security Adviser Dina Habib Powell took charge of Goldman Sachs’s global charitable foundation, helping to resurrect the big bank’s shattered image after it was implicated in practices that contributed to the financial crisis of 2007-2008.

GOOGLE WORKED TO RIG ELECTION FOR SWAMP EMPRESS HILLARY CLINTON TO KEEP THE FOREIGN INVADERS COMING!

http://hillaryclinton-whitecollarcriminal.blogspot.com/2018/09/google-rigged-it-so-illegals-would-vote.html

1. Globalism: Google VP Kent Walker insists that despite its repeated rejection by electorates around the world, “globalization” is an “incredible force for good.”

2. Hillary Clinton’s Democratic party: An executive nearly broke down cryingbecause of the candidate’s loss. Not a single executive expressed anything but dismay at her defeat.

3. Immigration: Maintaining liberal immigration in the U.S is the policy that Google’s executives discussed the most.

BARACK OBAMA

GLOBALIST FOR BANKSTERS AND THE SUPER RICH and OPEN BORDERS TO FINISH OFF THE AMERICAN MIDDLE-CLASS.

http://mexicanoccupation.blogspot.com/2018/09/barack-obama-and-his-muslim-style.html

“Democrats Move Towards ‘Oligarchical Socialism,’ Says Forecaster Joel Kotkin.”

GLOBALISTS’ BILLIONAIRES’ DICTATORSHIP FOR THE RICH

https://mexicanoccupation.blogspot.com/2018/10/facebook-and-google-assault-free-speech.html

THE INVITED INVADING HORDES: IT’S ALL ABOUT KEEPING WAGES DEPRESSED!

"In the decade following the financial crisis of 2007-2008, the capitalist class has delivered powerful blows to the social position of the working class. As a result, the working class in the US, the world’s “richest country,” faces levels of economic hardship not seen since the 1930s."

"Inequality has reached unprecedented levels: the wealth of America’s three richest people now equals the net worth of the poorest half of the US population."

Another financial earthquake in the making

By Nick Beams

The key issue to emerge from the semiannual meeting of the International Monetary Fund (IMF) held in Bali, Indonesia last week is that 10 years out from the 2008 global financial crisis the conditions have been created for another economic and financial disaster. And those in charge of the global economy have no means of preventing it, not least because the very policies they have carried out over the past decade have helped prepare it.

It was somewhat symbolic that the meeting took place in the immediate aftermath of the devastating earthquake and tsunami on the Indonesian island of Sulawesi, which again underscored the extent to which the record growth of social inequality, accelerating after 2008, has left hundreds of millions of impoverished people the world over vulnerable to the impact of both natural and economic disasters.

The meeting also coincided with another significant anniversary—20 years since the Asian financial crisis that devastated the Indonesian economy, along with others in the region.

And while the meeting was being held, there were signs that another financial earthquake is in the making, as Wall Street and global stock markets were shaken by the second major sell-off this year after five years of relative stability.

Two reports prepared by the IMF for the meeting pointed to the mounting problems of the global economy and financial system.

The World Economic Outlook revised down the estimate of global growth issued by the IMF in April and noted that the “synchronised” expansion of 2017 had come to an end. While growth would continue, there would be no return to the growth path that had prevailed prior to 2008. A review of the effects of the financial crisis, which produced the biggest economic downturn in the post-war period, drew out that, compared to the growth trajectory prior to the crisis, a large number of economies had suffered a contraction ranging from 10 percent to as high as 40 percent.

The Global Financial Stability Report pointed to the impact of rising interest rates in the US and elsewhere on “emerging markets” with high levels of external debt and dollar-denominated loans. The higher rates have already impacted Argentina—at present in receipt of a record bailout of $57 billion from the IMF—and have hit a number of other countries, including Turkey, Indonesia, India, Pakistan and South Africa, with signs that it will extend.

According to a report in the Financial Times, the financial stress hitting emerging market economies “dominated” discussions at the meeting, as IMF Managing Director Christine Lagarde warned that the present situation had the potential to lead to a withdrawal of capital from these countries as large as that which took place after the 2008 financial crisis.

The other key issue was the trade war initiated by the United States against China and other countries. At its spring meeting in April, the IMF warned that these measures posed significant risks to the world economy. Now those risks had materialised, with Lagarde and World Trade Organisation head Roberto Azevedo both issuing calls for “reform” of the WTO and for the international trading system to be repaired, not wrecked.

But the US has already stated it doubts that its objections to Chinese trade practices, including the subsidisation of state-backed businesses and the alleged theft of intellectual property, can be resolved within the WTO framework. Rather than seeking a strengthening of the so-called “rules-based” international trading order, the US, almost on a daily basis, is stepping up its attacks on China, regarding it as the central threat to its global economic and military dominance.

While it is pushing for a reduction of the Chinese trade surplus, Washington’s primary objective is to break up global supply chains so that key manufacturing and high-tech industries are brought back to the US to enhance its national military capacities for war.

At the same time, it is using standover tactics in relation to its “strategic allies,” above all the European Union, Japan and Canada, threatening them with the imposition of auto tariffs as high as 25 percent if they do not enter bilateral trade negotiations with the US and join its actions against China.

In the middle of the IMF meeting, as if the representatives of global capitalism needed to the reminded of the fact that none of the underlying factors that produced the crisis of 2008 has been resolved, Wall Street experienced a major two-day sell-off.

As an article in Bloomberg noted: “[W]hile this week wasn’t wholesale carnage, it’s more proof that a new era of volatility is upon us, one that is likely to last. Bad days pile up, and it gets harder to deny that five of the quietest years ever seen in equities are over.”

Those “quiet years” were the direct result of the lowering of interest rates to record lows and the policies of quantitative easing by the US Federal Reserve and other major central banks, which have pumped trillions of dollars into the financial system and sent the US stock market to record heights. But now the Fed and other banks are lifting interest rates and pulling back on easy money policies, not least because they want to have some “ammunition” to meet the next major economic and financial crisis.

As a number of more perceptive reports and comments have noted, the very measures adopted in the wake of the 2008 crash have only created the conditions for another disaster. Writing in the New York Times on September 18, Ruchir Sharma explained that while central bankers and other authorities have sought to contain the banks’ risky lending practices for home mortgages, new risks have emerged.

Sharma pointed out that within the $290 trillion global financial market, “there are hundreds of new risks, pools of potentially troubled debt” produced by the turn of corporate borrowers to non-bank lenders.

“As bank lending dried up, more and more companies began raising money by selling bonds, and many of those bonds are now held by those non-bank lenders—mainly money managers such as bond funds, pension funds or insurance companies.”

The result is that among the corporations listed on Wall Street’s S&P 500 index, debt has tripled since 2010 to one-and-a-half times annual earnings, near the peaks reached in the recessions of the early 1990s and 2000s, with the debt load much higher in some areas.

In the reports on the global financial system from the IMF and other institutions, the claim is regularly made that banks are in a much stronger position than they were in 2008 because of regulatory changes such as the Dodd-Frank Act in the US.

But as Carmen and Vincent Reinhart point out in an article in Foreign Affairs, the result has been the growth of so-called “shadow banking,” as borrowers for homes turn to organisations such as Quicken Loans rather than to Wells Fargo. “A majority of US mortgages are now created by such non-banking institutions, also known as ‘shadow banks.’ The result is that financial vulnerability remains but is harder to spot.”

The two authors point to another major change in the global financial system. As a result of quantitative easing, “the majority of government debt that is sold in the open market in the United States, Japan and the euro zone is now owned by central banks.” The concentration of government debt in official coffers makes the private market for it less liquid, which could make it harder for governments in advanced economies to borrow more in the future, they write.

A key feature of the build-up to the crash of 2008 was the way in which credit rating agencies gave their approval to the arcane financial instruments that proved to be worthless. Those practices have continued in another form.

An investigation by Bloomberg published on Thursday points to what it calls a “$1 trillion powder keg that threatens the corporate bond market.” The article explains that faced with weak sales growth coupled with rock-bottom interest rates, major companies felt that the way to growth was to borrow large amounts of money to buy out competitors.

According to the article, an investigation into 50 of the largest corporate acquisitions over the past five years revealed that “by one key measure more than half of the acquiring companies pushed their leverage to levels typical of junk-rated peers. But those companies, which have almost $1 trillion of debt, have been allowed to retain investment-grade ratings by Moody’s Investor Services and S&P Global Ratings.”

The report states that rating agencies simply accepted assurances from companies involved in the takeover deals that they would be able to “cut costs and pay down borrowings quickly, before the easy money ends.”

The investigation found that there had been a surge in the lowest rungs of investment-grade bonds, most of it driven by corporate acquisitions, with the result that there was now $2.47 trillion worth of corporate debt rated at the lower investment grade, more than triple the level at the end of 2008.

What these and other reports make clear is that the very measures undertaken in the wake of the 2008 crash, far from overcoming the crisis, have simply created a new financial house of cards, which is set to collapse with potential consequences even more serious than the breakdown ten years ago. The sharp fall on Wall Street this week, a result of fears of the consequences of interest rate rises, did not lead to a meltdown, but the tremors it sent out signalled the approach of another earthquake.

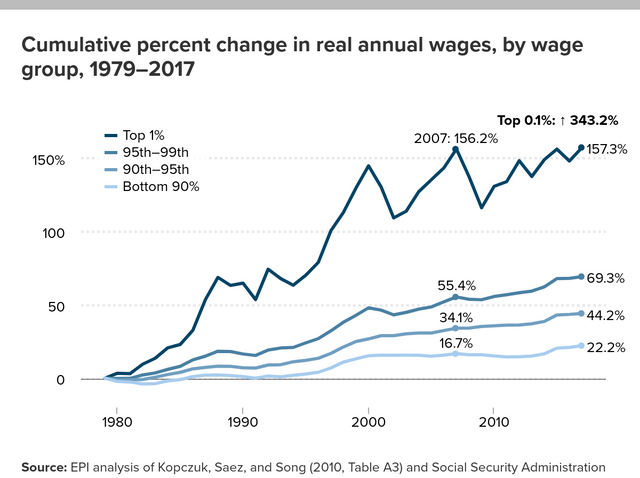

Record high income in 2017 for top one percent of wage earners in US

By Gabriel Black

In 2017, the top one percent of US wage earners received their highest paychecks ever, according to a report by the Economic Policy Institute (EPI).

Based on newly released data from the Social Security Administration, the EPI shows that the top one percent of the population saw their paychecks increase by 3.7 percent in 2017—a rate nearly quadruple the bottom 90 percent of the population. The growth was driven by the top 0.1 percent, which includes many CEOs and corporate executives, whose pay increased eight percent and averaged $2,757,000 last year.

The EPI report is only the latest exposure of the gaping inequality between the vast majority of the population and the modern-day aristocracy that rules over them.

The EPI shows that the bottom 90 percent of wage earners have increased their pay by 22.2 percent between 1979 and 2017. Today, this bottom 90 percent makes an average of just $36,182 a year, which is eaten up by the cost of housing and the growing burden of education, health care, and retirement.

Meanwhile, the top one percent has increased its wages by 157 percent during this same period, a rate seven times faster than the other group. This top segment makes an average of $718,766 a year. Those in-between, the 90th to 99th percentile, have increased their wages by 57.4 percent. They now make an average of $152,476 a year—more than four times the bottom 90 percent.

Graph from the Economic Policy Institute

Graph from the Economic Policy Institute

Decades of decaying capitalism have led to this accelerating divide. While the rich accumulate wealth with no restriction, workers’ wages and benefits have been under increasing attack. In 1979, 90 percent of the population took in 70 percent of the nation’s income. But, by 2017, that fell to only 61 percent.

Even more, while the bottom 90 percent of the population may take in 61 percent of the wages, large sections of the workforce today barely pull in any income at all. For example, Social Security Administration data found that the bottom 54 percent of wage earners in the United States, 89.5 million people, make an average of just $15,100 a year. This 54 percent of the population earns only 17 percent of all wages paid in America.

However unequal, these wage inequalities still do not fully present the divide between rich and poor. The ultra-wealthy derive their wealth not primarily from wages, but from assets and equities—principally from the stock market. While the bottom 90 percent of the population made 61 percent of the wages in 2017, they owned even less, just 27 percent of the wealth (according to the World Inequality Report 2018 by Thomas Piketty, Emmanuel Saez, and Gabriel Zucman).

The massive increase in the value of the stock market, which only a small segment of the population participates in, means that the top 10 percent of the population controls 73 percent of all wealth in the United States. Just three men—Jeff Bezos, Warren Buffet and Bill Gates—had more wealth than the bottom half of America combined last year.

Wages are so low in the United States that roughly half of the population falls deeper into debt every year. A Reuters report from July found that the pretax net income (that is, income minus expense) of the bottom 40 percent of the population was an average of negative $11,660. Even the middle quintile of the population, the 40th to 60th percentile, breaks even with an average of only $2,836 a year.

As the Social Security Administration numbers show, 67.4 percent of the population made less than the average wage, $48,250 a year in 2017, a sum that is inadequate to support a family in many cities—especially, with high housing costs, health care, education, and retirement factored in.

For the ruling class, though, workers’ wages are already too much. The volatility of the stock market and the deep fear that the current bull market will collapse has made politicians and businessmen anxious of any sign of wage increases.

In August, wages in the US rose just 0.2 percent above the inflation rate, the highest in nine years. Though the increase was tiny, it was enough to encourage the Federal Reserve to increase the interest rate past two percent for the first time since 2008. Raising interest rates helps to depress workers’ wages by lowering borrowing and spending. As the Financial Times noted, stopping wage growth was “central” to the Federal Reserve’s move.

Further analysis of the Social Security Administration data shows that in 2017, 147,754 people reported wages of 1 million dollars or more—roughly, the top 0.05 percent. Their combined total income of $372 billion could pay for the US federal education budget five times over.

These wages, however large, still pale in comparison to the money the ultra-rich acquire from the stock market. For example, share buybacks and dividend payments, a way of funneling money to shareholders, will eclipse $1 trillion this year.

Whatever the immediate source, the wealth of the rich derives from the great mass of people who do the actual work. Across the United States and around the world, workers, young people, and students have entered into struggle this year over pay, education, health care, immigration, war and democratic rights. This growing movement of the working class must set as its aim confiscating the wealth and power of this tiny parasitic oligarchy. Society’s wealth must be democratically controlled by those who produce it.

As CEO compensation soars and

banksters' plunder to new heights

"Another Fed study, “The Demographics of Wealth,” found that people born in the 1980s, part of the millennial generation, were at the greatest risk of becoming a “lost generation” in terms of wealth accumulation. This age group is one of the most likely to be saddled with student debt."

While workers are told by politicians of both big business parties that there is “no money” to pay for decent wages, education, health care or retirement, companies in the Standard & Poor’s 500 stock index are sitting on the largest cash stockpile in history, with estimates varying between $1.8 and $2.2 trillion as of the end of 2017.

Fifty-one million US households cannot afford “survival budget”

By Kate Randall

26 May 2018

Newly released data cast a revealing light on the state of income inequality in America a decade after the Great Recession. While CEO pay soars to unheard of heights, nearly 51 million US households cannot afford basic necessities like housing, food and health care. The figures show that a tiny oligarchy of the super-rich continues to tighten its grip over society, as more and more families struggle to get by.

The New York Times on Friday published the Equilar 200 Highest-Paid CEO Rankings for 2017. The survey, conducted annually by the executive compensation consulting firm Equilar, lists the pay packages awarded to CEOs at US public companies with more than $1 billion in revenue.

Entries regarding the 10 highest-paid CEOs in 2017 show not only massive compensation packages, but huge percentage increases over 2016.

· No. 1: Hock E. Tan of Broadcom, total compensation of $103,211,163—a 318 percent increase over 2016

· No. 2: Frank J. Bisignano of First Data, total compensation of $102,210,396—a 646 percent increase over 2016

· No. 10: Stephen Kaufer of TripAdvisor, total compensation of $43,160,584—a 3,400 percent increase over 2016

This year for the first time, as part of the 2010 Dodd-Frank banking law, publicly traded US corporations must begin publishing comparisons between the pay of their chief executive and the median compensation of other employees. (Figures are not yet available for all of the highest-earning CEOs.)

The following are just a few of the pay ratios for 2017:

· Mindy Grossman, Weight Watchers International, with $33,371,856 in total compensation, received 5,908 times the median employee pay ($6,013).

· Margaret H. Georgiadis, Mattel, with $31,275,289 in total compensation, received 4 , 987 times the median employee pay ($6,271).

· Michael Rapino, Live Nation Entertainment, whose total compensation rose by 577 percent to $70,615,760, received 2,893 times the median employee pay ($24,416).

Put another way, a Walmart worker earning the company’s median salary of $19,177 would have to work for more than 1,000 years to earn the $22.2 million that company CEO Doug McMillon was awarded in 2017.

Among the companies that disclosed CEO pay ratios, the median was 275 to 1, i.e., the typical employee would have to work 275 years to earn the annual compensation of his or her company’s CEO.

While CEO compensation continues to climb—with the top 200 CEOs receiving an average raise of 14 percent in 2017, compared to 9 percent in 2016 and 5 percent in 2015—there are 50.8 million US households that cannot afford a basic monthly budget, including housing, food, child care, health care, transportation and a smart phone. The new data was made available Tuesday by the United Way ALICE Project.

Those struggling to meet a basic monthly budget include 16.1 million households living below the official federal poverty level, an abysmally low $24,300 for a family of four in 2016. Also included, however, were another 34.7 million families called ALICE, which stands for Asset Limited, Income Constrained, Employed. In other words, these households include working members and are not “officially” poor, but cannot afford basic necessities.

As the ALICE Project press release on the data notes, “ALICE is the nation’s child care workers, home health aides and store clerks—those men and women who work at low-paying jobs, having little or no savings and are one emergency from poverty.” Workers at companies whose CEOs rank in the top 200 in pay fall into this category, including McDonald’s, Walgreens, Office Depot and food service companies Aramark and Sysco.

Data highlighted by the research includes the following:

· Two-thirds of all US jobs in the country are low-paying—less than $20 an hour, or $40,000 a year if full-time.

· More than 30 percent of households in each state cannot afford a basic “survival budget.” The percentage of these families ranges from 32 percent in North Dakota to 49 percent in California, New Mexico and Hawaii.

· Those families earning over the poverty level but struggling to afford basic necessities outnumber similarly struggling households living in poverty in all 50 states.

· California, Texas and Florida—the first, second and fourth most populous states, respectively--have the largest number of ALICE households in the country.

Also published Tuesday was a study by the Federal Reserve Board that exposes the precarious financial situation facing millions of American workers and their families. The “Report on the Economic Well-Being of US Households in 2017” found that 4 in 10 adults, if faced with an unexpected expense of $400, would either be unable to cover it or would pay for it by selling a possession or borrowing money.

For working class families, such unexpected expenses could include a medical bill, a car repair, home repairs, appliance replacement, unexpected taxes or fines—the list goes on. While the CEOs in the top 200 have assets stashed away in rainy day funds in the millions, an unexpected emergency can mean going without food, being forced deeper into credit card debt, debt collection or eviction. The study found that 3 percent of renters were evicted or moved because of the threat of eviction in the last two years.

The report noted that one-fifth of non-retired adults are pessimistic about their future employment opportunities. A substantial number of workers are in precarious employment, with one-sixth having irregular work schedules imposed by their employer, and one-tenth receiving their work schedules less than a week in advance.

The study reported that over half of college attendees under age 30 have taken on debt to pay for their education. Those who failed to complete a degree, and those who attended for-profit institutions, were more likely to have fallen behind on their payments. Among those making payments on their student loans, the typical monthly payment was between $200 and $300, or 6 to 9 percent of total income for someone working full-time at $20 an hour.

Another Fed study, “The Demographics of Wealth,” found that people born in the 1980s, part of the millennial generation, were at the greatest risk of becoming a “lost generation” in terms of wealth accumulation. This age group is one of the most likely to be saddled with student debt. While all families headed by someone born in 1960 or later have failed to recover economically since the Great Recession, those born in the 1980s are the least likely to have recovered to their pre-1980 financial level.

Not surprisingly, the “Economic Well-Being” report found that less than two-thirds of non-retired adults thought their retirement savings are on track. One-fourth had no retirement savings or pension whatsoever.

While workers are told by politicians of both big business parties that there is “no money” to pay for decent wages, education, health care or retirement, companies in the Standard & Poor’s 500 stock index are sitting on the largest cash stockpile in history, with estimates varying between $1.8 and $2.2 trillion as of the end of 2017.

The obscene levels of compensation doled out to the CEOs and the corresponding struggle of working class families to pay basic monthly bills provoke no serious response from the Democratic Party, which is fixated on the claims of Russian “meddling” in the 2016 elections.

The Democrats have provided the votes to fund the Pentagon’s record $700 billion budget and secure the confirmation of black-site torture administrator Gina Haspel to head the CIA. They put up no serious opposition to Trump’s multi-trillion-dollar tax cut for corporations and the rich. Meanwhile, work requirements are being imposed on Medicaid and food stamps, with virtually no opposition from the Democratic Party.

The working class must break from both parties of the capitalist class and build a mass socialist movement to seize the wealth of the financial elite and put an end to the profit system. This is the only basis for meeting essential social needs.

Australian housing market slumps toward potential crash

By James Cogan

17 October 2018

Amid the growing global economic turmoil and uncertainty, statistics, studies and comments published in the financial press are drawing attention to the fragility of the Australian real estate market and the immense social and political implications of a severe slump.

After close to a decade of soaring house prices in the major cities, Australian households are among the most indebted in the world, with household debt compared to income close to 200 percent. Millions of families have been compelled to borrow staggering sums to achieve the so-called “Australian dream” of home ownership.

At the same time, speculators have gambled that the purchase and resale of real estate offered greater capital gains than stocks and other investments. The major Australian banks became among the most profitable in the world by facilitating a speculative frenzy, borrowing at near zero interest rates internationally and lending at higher margins in Australia.

By the end of 2017, housing in Sydney and Melbourne, the country’s largest cities and the focus of real estate speculation, was ranked as among the “least affordable” in the world. Sydney was ranked as the second worst after Hong Kong, with median house prices nearly 13 times median household income. Melbourne was the fifth worst internationally, with prices close to 10 times higher than what the median household earns in a year.

In August 2018, there were 613 suburbs nationally where the median house price was over $1 million—double the number just five years ago and overwhelmingly in Sydney and Melbourne.

Rampant profit-gouging is rife in the financial industry, some aspects of which were revealed during the recent Royal Commission. Between 2013 and 2015, for example, the banks doubled the amount they lent, mainly to speculative investors, on “interest only” repayment terms, meaning lenders did not have pay any of the principal on a loan for as long as seven years. More generally, bank assessors overestimated the income or underestimated the weekly expenses of applicants to justify extending huge loans to make home purchases or acquire small businesses.

A great deal of money has been made by the capitalist class and sections of the upper middle class at the direct expense of millions of workers, who have been effectively transformed into debt slaves to the banks and finance houses. Outstanding housing debt in Australia reached $1.762 trillion in May 2018—a historic high of 130 percent of Gross Domestic Product.

Under these conditions, a slump in the real estate market is now underway. The median home price has fallen 4.4 percent this year in Sydney and 4.6 percent in Melbourne. Auction clearances have dropped to barely 50 percent. The number of unsold properties on the market has soared by 19.5 percent in Sydney and 18.4 percent in Melbourne.

The developing crisis is partly due to oversupply, but also because the banks have taken belated and desperate steps to tighten credit and therefore their exposure to potential problem loans. Up to 40 percent of applications are now being rejected, compared with barely 5 percent in 2017. The number of new loans to investors has fallen 17.7 percent compared with 12 months ago. Even new loans for owner-occupier dwellings are down 3.6 percent.

The downturn is just beginning. Investment house Morgan Stanley predicted this month at least 10 to 15 percent will be slashed off property values over the next several years.

Other analysts are giving more dire estimates. Martin North, a researcher with Digital Finance Analytics, was widely criticised for predicting on the “60 Minutes” current affairs program that prices could crash by as much as 30 to 45 percent and plunge Australia into its worst economic conditions since the Great Depression.

North’s worst-case scenario, however, is based on significant and credible research. A major study this year by his company found that at least one in four mortgage-holding households—some 820,000—are already in financial stress, meaning they can only meet repayments by reducing other expenses such as food, health care and entertainment.

Digital Finance Analytics considered the implications if interest rates rise. While the Reserve Bank of Australia (RBA) has sought to keep rates at historic lows, its ability to continue to do so is in question due to the steady rise of official rates in the United States. The US Federal Reserve is expected to raise rates again in December and throughout 2019.

Each US rise puts downward pressure on the value of the Australian dollar, increasing the borrowing costs of the banks, which source anywhere up to 40 percent of their capital from overseas markets, especially Wall Street.

Even if the RBA did try to resist matching US increases, the major banks will raise their rates regardless. Their parasitic business model consists of borrowing internationally and lending within Australia at higher interest rates. As the cost of their borrowings increase, they are passing on the burden to Australian households.

Even small rate rises will cause staggering social distress. If rates rose just by 2 percent, back to the level in 2012, well over 50 percent of mortgaged households, some 1.6 million, would sink into financial stress due to their huge repayments.

In dozens of working class and middle class suburbs, between 60 and 100 percent of households would be affected. Many borrowers face the prospect of becoming so-called “mortgage prisoners,” condemned to paying off outstanding loans that are greater than the value of their homes. A wave of foreclosures would have to be expected, further aggravating the slump in property prices.

The Digital Finance Analytics study into the impact of interest rates did not consider the impact of a significant rise in unemployment. That is, it assumed that mortgage holders still had jobs and could struggle to meet their repayments.

Several factors are coming together, however, that threaten to plunge Australia into recession and cause a sharp increase in unemployment.

The construction industry and related real estate activity collectively employs 1.4 million people. As the property slump develops, tens, if not hundreds of thousands of workers in this sector may well lose their jobs.

The launch of open trade war by the United States against China, Australia’s largest export market and trading partner, as well as the general descent into dog-eat-dog competition between the major economic blocs, looms as the greatest threat.

On October 12, the RBA expressed guarded, but serious concerns in its latest “Financial Stability Review”. The central bank stated:

“Australia would be sensitive to a sharp contraction in global growth or dislocation in global financial markets because of the importance of trade and capital inflows. A worsening in external conditions could see a downturn in the domestic economy, reduced availability and higher cost of offshore funding and falls in asset prices, with a resulting deterioration in the performance of borrowers and lenders.”

The RBA continued: “In the current environment, a range of possible triggers could precipitate a global economic downturn. An escalation of trade protection could see a sharp fall in trade, business confidence and investment.”

The central bank issued pro forma reassurances about the “resilience” of the Australian financial system and the ability of households to continue to meet their debt obligations.

In the scenario of a property market crash,

however, the Australian capitalist class would

face the same situation as its counterparts in

the US and Europe after the 2008 financial

crisis. To save the banks from insolvency,

they would demand that the government step

in with massive multi-billion bail-outs and

impose savage austerity on the working class

to pay for them.

It is essential that the working class advance its own interests against the social disaster that the capitalist system has already produced and threatens to inflict. A mass political movement must be developed to fight for a workers’ government that will implement the most far-reaching socialist policies.

The socialist re-organisation of society would necessarily start with the expropriation of all banks and financial institutions which would be placed in public ownership, and an end to the subordination of the basic right to decent housing to the profit interests of a super-wealthy minority.

Housing Market Wobbles, Supporting Trump’s Case Against Fed Rate Hikes

3:07

U.S. homebuilding dropped more than expected in September and mortgage application volume for last week came 15 percent lower than a year ago, adding credence to President Donald Trump’s complaints that the Federal Reserve is raising interest rates too rapidly.

“My biggest threat is the Fed. Because the Fed is raising rates too fast. And it’s independent, so I don’t speak to them. But I’m not happy with what he’s [Powell’s] doing. Because it’s going too fast,” Trump said in an interview Tuesday with Trish Regan of the Fox Business Network.

Housing market data released Wednesday appear to support the president’s view that the Fed’s rate hikes are slamming the breaks in some areas of the economy. Refinancing applications, the most interest-rate-sensitive type of mortgage, fell 9 percent for the week. These are now 33.5 percent lower than a year ago. The average rate for 30-year fixed-rate mortgages climbed to 5.10 percent, up from 5.05 percent a week earlier. That is the highest rate since 2011.

“The numbers are tepid enough that you need to wait,” CNBC’s Jim Cramer said Wednesday morning. “If you are on the Fed and you are a rigorous thinker and you’re not anecdotal, you’d say, ‘Okay. Maybe we can do December. Maybe we shouldn’t [do more].”

The Fed is widely expected to hike its interest rate target by a quarter of a percentage point in December.

Cramer said he thought the president was “bashing the Fed unfairly” but addded that the Fed was “putting its head in the sand” by continuing to move rates upward despite signs of weakness in housing.

Higher rates make home-buying less affordable and mean fewer borrowers can benefit from refinancing.

Housing starts, which measure groundbreaking on new homes, declined 5.3 percent to a seasonally adjusted annual rate of 1.201 million units in September, the Commerce Department said on Wednesday. Data for August was revised down, showing the housing market had slowed by even more than previously reported.

Trump country has been especially hard hit by the higher rates. Starts in the South, the biggest market for homebuilding, crashed 13.7 percent last month. It’s likely that Hurricane Florence played a role in that steep decline.

But housing starts in the Midwest fell 14 percent, suggesting a broader weakness.

Housing starts in the Northeast and the West rose, with the Northeast posting a 29 percent gain.

Applications for permits were lower as well. In the Midwest, these fell nearly 19 percent. Nationwide, building permits fell 0.6 percent to a rate of 1.241 million units in September. Since permits are an indication of future building, this is a signal that homebuilding is likely to remain slow.

Home building pulls above its weight in the economy because construction is labor intensive and new home purchases often result in the subsidiary shopping, as homebuyers pick up new appliances, furniture, and even cars when they move in.

The housing market has been a weak spot in an otherwise strong economy, principally because of rising mortgage rates and already elevated home prices. Homebuilder sentiment, however, rebounded in October, suggesting that some of the worst fears for the housing market have eased.

Wall Street volatile as global economy becomes “fragile”

By Nick Beams

Volatility has continued on Wall Street following two days of major falls last week. The Dow Jones index shot up by more than 500 points on Tuesday, followed by a more than 300-point decline during Wednesday before recovering to finish 80 points down.

Yesterday, after a global sell-off, the Dow finished down by 327 points, after dropping 470 points during the course of the day. In what was described as a “jittery session,” the S&P 500 was down 1.4 percent, its largest fall in a week, and has now experienced a decline in 10 out of the 14 trading sessions this month.

The immediate volatility is being driven by two conflicting tendencies. On the one hand, US markets are being pushed down by the further expected increases in the Federal Reserve’s base interest rate and the general tightening of monetary conditions expressed in the rise of the rate on the benchmark 10-year US Treasury bond, which is now hovering around 3.2 percent. Monetary conditions are also being made more restrictive by the Fed’s reduction of its assets holdings by $50 billion per month as part of its program to reduce its balance sheet. Its previous quantitative easing program saw Fed assets expand from less than $1 trillion to $4.5 trillion.

On the other hand, share prices are being boosted by the rise in profits being reported by banks and major companies. There is also an expectation that US growth will continue and that, while asset valuations may be “stretched,” there is still some way for the market to run and gains to be reaped.

The underlying instability and fears of a major sell-off were underscored by further comments by US President Donald Trump following his denunciation of the Fed’s interest rate rises as “crazy” and “loco” during last week’s sell-off. In an interview with the Fox Business News Network, he repeated his assertion that the Fed was raising interest rates too fast and described the central bank’s actions as “my biggest threat.”

Nominally adhering to the independence of the Fed, Trump said he had not spoken to its chairman Jerome Powell, whom he appointed last year. But he was “not happy” with what Powell was doing, “because it’s going too fast.” Powell, he asserted, was “being extremely conservative, to use a nice term.”

Former Fed chairwoman Janet Yellen weighed into the debate, saying she agreed with the Fed’s present policies and that there was a danger of the economy overheating. She said the present growth rate of 3 percent was “terrific” but cast doubt on whether it was sustainable in the longer term. The Fed would need to be “skilful and lucky” to achieve a soft landing after 2019.

It is a significant observation when a former Fed chief remarks that US growth needs “luck” to continue.

The minutes from the Fed’s interest-rate setting Open Market Committee of September 25-26, released on Wednesday, indicated that the central bank is still on course for another interest rate rise in December, with some participants wanting to tighten policy still further.

The minutes noted that some members thought it would be necessary to “temporarily raise the federal funds rate above their assessments of its longer-run level in order to reduce the risk of a sustained overshooting of the Committee’s two percent inflation objective or the risk posed by significant financial imbalances.”

The chief concern is not with inflation per se but whether the lowering of the unemployment rate and labour shortages lead to a significant push for increased wages, which the Fed is determined to suppress.

Market volatility is also being fuelled by the worsening global economic outlook resulting from the rise in US interest rates, the increasing value of the dollar, and the escalation of trade tensions between the US, China and other countries.

The dollar’s rising value has a major impact on emerging markets because it increases the real level of dollar-denominated loans, making the repayment of the interest and principal more expensive. The Financial Times has described the situation facing emerging markets as “ugly,” noting that the JPMorgan Chase EM currency index has fallen by 12 percent since April. Stock markets have also been hit, with the MSCI Emerging Markets Index down by more than 16 percent in the same period.

The elevated stock market values in the US stand in contrast to the rest of the world. While the S&P 500 index is up more than 4 percent for the year, the Stoxx Europe 600 index has experienced a 6.2 percent decline, Japan’s Nikkei 225 is down by 0.9 percent and the Shanghai Composite has fallen by 23 percent.

Trade tensions are continuing to rise. There was a sharp exchange at a World Trade Organisation (WTO) meeting on Tuesday between the US representative Dennis Shea and his Chinese counterpart Zhang Xiangchen.

Shea demanded that the WTO confront China’s alleged trade abuses and remove its rights as a developing economy. Zhang countered that “no one can be singled out” and that efforts to undermine the basic principles of the organisation had to be opposed. But Shea insisted that the world body target China.

“Adequately responding to the challenges of non-market economies is nothing less than an existential matter for this institution,” Shea said.

This is a thinly-veiled threat that unless the WTO takes action over what the US calls China’s “market-distorting” policies, including subsidies for state-backed industries and its alleged acquisition of high-tech knowledge through forced technology transfers or outright theft, it will withdraw from the body.

The US has already significantly undermined the WTO by blocking the appointment of members to its appellate body, which has the final say on trade disputes. The Trump administration has refused for more than a year to consider new appointments because it says former members went beyond their mandate and took an “activist approach” detrimental to the US. The administration’s actions have reduced the normally seven-member body to just three and if the present stand-off continues it will not be able to function past December next year.

As part of its trade war against China, the US has been seeking to bring its “strategic allies” into its camp by opening up negotiations with them on bilateral trade deals. These moves, including the recently-concluded US Mexico Canada Agreement (USMCA) and agreements with the European Union and Japan for one-on-one negotiations, have been accompanied by threats of auto tariffs of up to 25 percent.

In addition, the USMCA contained what the US side characterised as a “poison pill.” If either of the other partners entered a free trade agreement with a “non-market” economy, namely China, the US could withdraw. US trade officials have made it clear they want to see this provision included in other bilateral deals.

Negotiations with Europe, agreed on at a meeting between Trump and European Commission President Jean-Claude Junker in July, have already produced conflict.

In talks on Wednesday each side accused the other of undermining the July agreement. Commerce Secretary Wilbur Ross said of his EU counterpart Cecilia Malmstrom that it was “as though she was at a different meeting from the one that we attended.”

Ross said the purpose of the meeting was to get “near-term deliverables including both tariff relief and standards.” Trump’s “patience was not unlimited.”

Malmstrom said the EU had asked several times for a “scoping exercise”—the prelude to a full-scale trade deal—but the US had failed to respond. “So far,” she stated, “the US has not shown any big interest there, so the ball is in their court.”

Ross said the contention that the US was slowing things down was “simply inaccurate.” The US ambassador to the EU, Gordon Sondland, was even more blunt and implicitly raised the threat that auto tariffs could be put back on the agenda.

“If the president sees more quotes like the one that came out today his patience will come to an end,” Sondland said, attacking the “complete intransigence” of the EU and warning that any attempt to “wait out” Trump’s term as president was a “futile exercise.”

Warning that politics was putting the “skids under the bull market,” Financial Times economics commentator Martin Wolf wrote on Wednesday that, as the recent IMF meeting had made clear, reasons for concern “abound.” Above all, the “struggle between old and new superpowers” could “change everything.”

Wolf noted that the valuation of risky assets was “stretched” and just a small shift in global financial conditions could damage not only emerging markets. Wolf said the aggregate debt in countries “with systemically important financial sectors now stands at $167 trillion, or over 250 percent of aggregate gross domestic product,” compared with 210 percent in 2008.

The global economy and financial systems are “fragile,” Wolf concluded. “These are dangerous times—far more so than many now recognise. The IMF’s warnings are timely, but predictably understated. Our world is being turned upside down. The idea that the economy will motor on regardless while this happens is a fantasy.”

Tumbling markets complicate Trump’s midterm messaging

Charles Boeddinghaus, left, and Michael Milano work on the floor of the New York Stock Exchange on Wednesday. (Richard Drew/AP)

U.S. stock markets fell sharply Wednesday, erasing all gains for the year and muddying one of President Trump’s favorite talking points two weeks before the midterm elections.

The technology-heavy Nasdaq fell 4.4 percent Wednesday, its worst one-day drop since the financial crisis. The index has slid more than 12 percent since the end of August. The Standard & Poor’s 500-stock index, which tracks a broader group of U.S. companies, has lost $2 trillion in value since late September, down 9 percent. The Dow Jones industrial average, meanwhile, lost 608 points Wednesday and is down 8.3 percent in the past three weeks.

The financial swoon threatens to undermine a market rise for which Trump has frequently claimed credit and to highlight controversial aspects of Trump’s agenda, including tariffs many companies are blaming for their struggles and a tax cut that polls suggest the public views as inadequately helpful for the middle class.

Trump has increasingly looked to shift focus away from economic indicators he once touted and toward immigration and other issues — and assign blame elsewhere for any economic setbacks.

He has pummeled the Federal Reserve, alleging higher interest rates pose the biggest risk to growth — even musing he might have made a mistake when he nominated Jerome H. Powell as the nation’s top central banker less than a year ago. It is unusual for a president to attack the central bank — the Fed aims to maintain independence from the White House to avoid the taint of politics on its economic decisions.

President Trump said repeatedly during the summer that the United States was experiencing the greatest economy in its history, largely citing the low unemployment rate. (Leah Millis/Reuters)

Trump has also promised a 10 percent middle-class tax cut, a proposal that caught his aides by surprise and that lawmakers said was exceedingly unlikely in the near future.

In recent days, Trump has suggested he could mobilize the military to protect the southern border from a caravan of migrants, But he has said little about the recent stock-market movement.

“The president is very good at manipulating the narrative and getting people — either through traditional media or social media — to focus on what he wants them to focus on,” said Brian Gardner, managing director at Keefe, Bruyette & Woods, an investment bank.

Trump’s focus on immigration and his surprise proposal for a middle-class tax cut come as the strong economy exhibits signs of strain.

Beyond the slumping market, rates on 30-year mortgages are climbing, with many loans now eclipsing 5 percent. Higher interest rates can limit borrowing, slowing home sales and the economy. And multiple businesses — including firms that Trump has praised, such as Harley-Davidson and United Technologies — are warning that the White House’s trade strategy could cost them millions of dollars in revenue.

Forty-eight S&P 500 companies mentioned “tariffs” during calls with analysts in recent days, many warning that they threaten to cause a drag on the economy.

Trump has dismissed complaints from chief executives about the White House’s trade policy, telling the Wall Street Journal that overpaid executives will not take responsibility for their own bad decisions.

“I have created such an incredible economy,” Trump said in Montana last week. “I have created so many jobs.”

Trump said repeatedly during the summer that the United States was experiencing the greatest economy in its history, largely citing the low unemployment rate. And Tuesday, in an interview with the Wall Street Journal, he falsely denied imposing any tariffs on imports, even though he has implemented numerous tariffs against a range of countries this year.

His comments to the Journal directly contradict his Twitter post from a few hours earlier, in which he said the tariffs he had launched were bringing billions of dollars into the government’s coffers. Trump has mischaracterized the way tariffs work, suggesting they are paid by other countries rather than by U.S. companies that import the products — often passing those costs to U.S. consumers.

White House officials have denied that Trump’s recent behavior is driven by concerns about a weakening economy, saying the new tax plan, despite its surprise rollout, is meant to build on last year’s tax law and help the middle class. And a number of senior officials have said the fundamentals of the economy remain strong, and the White House has an upbeat outlook for next year.

“Our job is to focus on what the economic numbers say, and the numbers are very solid right now,” Kevin Hassett, chairman of the White House Council of Economic Advisers, said in an interview. “If your policies have produced the numbers we are observing, then you shouldn’t duck.”

Douglas Holtz-Eakin, a Republican economist, said the new tax-cut announcement struck many as an act of knee-jerk desperation.

“I don’t think it helps to have the president invent a tax cut,” he said. “That looks panicky. That hurts the larger effort. That wasn’t the White House. That was him.”

Job growth during Trump’s presidency is roughly comparable to the last four years of the Obama administration, though the jobless rate is lower and economic growth has picked up. Economists are mixed on whether this is sustainable, with some cautioning the gains from tax cuts and higher federal spending are temporary.

“It’s easy to say [Trump is] trying to set the Fed up for the fall here, but a lot of people were warning that the president was taking a risk and Republicans were taking a risk by putting forward a bunch of fiscal stimulus at this point in the business cycle,” said James Pethokoukis, a policy analyst at the American Enterprise Institute.

New-home sales sank for the fourth straight month in September, reflecting the impact of mortgage rates that now top 5 percent for many borrowers.

Sales of new single-family homes last month fell 5.5 percent from the previous month, to a seasonally adjusted annual rate of 553,000, according to a government report. September’s sales volume was more than 13 percent lower than the same month one year earlier, and figures for June, July and August were also revised down.

Though the strong labor market is likely to support demand, some economists are beginning to worry about collateral damage from a housing downturn.

“The economy cannot grow at a sustainable 3 percent pace for long if new-home sales continue to tumble,” warned economist Chris Rupkey of MUFG Union Bank.

Many executives had hoped trade fights with China and other countries would be resolved swiftly, but it appears a number of disagreements will drag into at least next year.

The $260 billion in tariffs Trump unleashed on Beijing took effect in this year’s third quarter, covering roughly half of what the United States buys from China.

American companies have warned for months that Trump’s trade war with China and other nations could wrench their bottom lines, and now they are quantifying that damage in dour earnings reports.

Ford recently reported levies on metals will shave $1 billion off the automaker’s profits, while consumer-goods giant Honeywell said it expects to absorb “hundreds of millions of dollars” in new duty-related costs.

Minnesota manufacturer 3M projected a loss next year of $100 million, blaming “tariff head winds.” Caterpillar shares took the sharpest dive in seven years after the tractor maker said the commercial battle between the world’s two largest economies was driving up the price of steel.

Walmart cautioned that prices could swell because a third of the products on its shelves arrive from outside the United States — and many are labeled “Made in China.”

United Technologies, which once lauded Trump for saving its Carrier subsidiary’s Indianapolis furnace factory, has changed its public stance on the president’s economic moves, saying his flurry of levies will sting to the tune of $200 million.

And Harley-Davidson said this week the duties will zap $20 million out of its wallet this year and that retaliatory tariffs from the European Union could deal an additional $45 million blow.

More than a third of the 110 S&P 500 companies that have shared third-quarter earnings since Tuesday have discussed the impact of higher border taxes during their conference calls with analysts, according to the investor research group FactSet.

Some companies have appealed directly to the administration, urging Trump to lower the trade barriers before the burden falls on American shoppers.

“As the largest retailer in the United States and a major buyer of U.S. manufactured goods, we are very concerned about the impacts these tariffs would have on our business, our customers, our suppliers and the U.S. economy as a whole,” Walmart wrote in a late-September letter to U.S. Trade Representative Robert E. Lighthizer.

Several economic factors could converge in the coming weeks to put more pressure on growth, including a decision from Powell about whether to again raise a key borrowing rate in December and an expected fight over federal spending levels. The results of those could give investors and households a new perspective on Trump’s stewardship of an economy that looks much different from its appearance one year ago.

Offering one of the last snapshots of the economy before the midterm elections, the government is scheduled to release economic data Friday that measures how much the economy grew from July through September. Analysts diverge strongly on how strong or weak the report will be.

David J. Lynch contributed to this report.