Hundreds of Billions in Unrealized Loan Losses Threaten to Spark the Next Bank Liquidity Crisis

NEW YORK (Reuters)—The Federal Reserve's preferred bond market signal of an upcoming recession has plunged to fresh lows, bolstering the case for those who believe the central bank will soon need to cut rates in order to revive economic activity.

Research from the Fed has argued that the "near-term forward spread" comparing the forward rate on Treasury bills 18 months from now with the current yield on a three-month Treasury bill was the most reliable bond market signal of an imminent economic contraction.

That spread, which has been in negative territory since November, plunged to new lows this week, standing at nearly minus 170 basis points on Thursday.

Fed Chair Jerome Powell said last year that the 18-month U.S. Treasury yield curve was the most reliable warning of an upcoming recession.

"Powell's curve ... continues to plunge to fresh century lows," Citi rates strategists William O'Donnell and Edward Acton said in a note on Thursday. Refinitiv data showed the curve was the most inverted since at least 2007.

Recession fears have surged in recent weeks, with investors worried the tumult in the banking system sparked by the March collapse of Silicon Valley Bank will tighten credit conditions and hurt growth.

The Fed - which has embarked on one of its most aggressive rate hiking cycles in decades to defeat inflation over the past year - has forecast borrowing costs will remain around current levels to the end of 2023. But market participants believe tighter monetary policy is already starting to hurt growth and are betting on rate cuts later this year.

When looking at that curve inversion in light of recent declines in economic indicators and money supply, "it's not hard to see why markets may be increasingly thinking 'policy error' when reading about further rate hikes," Citi’s analysts said.

Continuing its inflation-fighting campaign, the Fed last month raised interest rates by a quarter of a percentage point, though it indicated it was on the verge of pausing further increases in borrowing costs after the banking turmoil.

Some Fed officials have recently argued for more hikes, with St. Louis Fed President James Bullard saying on Thursday that the Fed should stick to raising interest rates to lower inflation while the labor market remains strong. Money market investors, however, on Thursday were largely betting the Fed would have cut rates by about 70 basis points by December, from the current 4.75%-5% range. "All this tightening of financial conditions, with the Fed raising rates significantly, now it's morphing into maybe a little bit of a credit tightening," said Jack McIntyre, portfolio manager at Brandywine Global. "Our conviction level down the road is that rates are going to be lower," he said.

(Reporting by Davide Barbuscia; editing by Ira Iosebashvili and Chizu Nomiyama)

Published under: Economy , Inflation

This is the Beginning of a Huge Wave of Bankruptcies and Layoffs Indicate It's Going to Get Worse

JOE BIDEN: LYING SOCIOPATH GAMER PARASITE LAWYER!

Despite his Wall Street, big business, Big Tech, and billionaire donations, Biden has attempted to portray himself as a small-town fighter from Scranton, Pennsylvania. JOHN BINDER

“This was not because of difficulties in securing indictments or convictions. On the contrary, Attorney General Eric Holder told a Senate committee in March of 2013 that the Obama administration chose not to prosecute the big banks or their CEOs because to do so might “have a negative impact on the national economy.”

“Attorney General Eric Holder's tenure was a low point even within the disgraceful scandal-ridden Obama years.”

DANIEL GREENFIELD / FRONTPAGE MAG

Silicon Valley Bank Board Included Barack Obama, Hillary Clinton Donors

Moody’s Chief Economist: Customers Will Ultimately Pay to Save SVB, Signature Bank Depositors

On Monday’s broadcast of C-SPAN’s “Washington Journal,” Moody’s Analytics Chief Economist Mark Zandi stated that ultimately, “we all bear the cost” of backstopping the depositors of Silicon Valley Bank and Signature Bank because banks will pass part of the cost on to consumers, but he thinks the backstopping was the least bad decision.

Zandi said, “In terms of who pays, most directly, it’s the banks themselves. Because the FDIC — who is coming in to resolve these failed institutions and pay off depositors and other creditors — pulls that money out of the Deposit Insurance Fund, the fund that’s been established where banks contribute into that for this very purpose, to pay for failed institutions. But clearly, the banks will then try to pass at least some of that along to their customers. So, they’ll eat some of it in the form of less earnings, lower profits, it probably affects the pay of their executives and other employees. But, ultimately, it likely also ends up in lower deposit rates for depositors and higher lending costs for lenders. So, ultimately, the cost is borne broadly by the customers of the banking system, which is most of us.”

He continued, “Now, having said that, the calculation you have to do here is, if the FDIC didn’t step in and resolve those institutions and if the government hadn’t provided those — that kind of strong backstop, what was the counterfactual then? What would have happened? And it felt really — a couple of weeks ago, it felt pretty uncomfortable. It felt like the banking system could come under extreme pressure, we could have deposit runs and then, ultimately, the cost to all of us would be even greater, because the government would have had to step in, provide more support, there would be more failures, and the cost to us would be even greater. So, it’s kind of a no good choice here…I think policymakers made the least bad choice that they had. But ultimately, we all bear the cost of that as customers of the bank.”

Follow Ian Hanchett on Twitter @IanHanchett

One can make a good argument that banking is part of global economic problems. The system allows banks to get bigger and bigger, with profits going, not to people who create, but to those who despoil. This is no longer a case of lenders driving capitalism. Instead, it is a closed system that works with the government to police people and entices them into bad financial decisions (think of the 2008 collapse over equity-free housing loans). It promotes spending much of our productivity, national and personal, on banking services.

Dem Rep. Gottheimer: We Still Don’t Know What Regulators Did During SVB Collapse

On Wednesday’s broadcast of CNBC’s “Power Lunch,” Rep. Josh Gottheimer (D-NJ) stated that we still don’t know what regulators did over the weekend that Silicon Valley Bank collapsed.

Co-host Tyler Mathisen asked, “Chairman McHenry was incensed, I guess is a possible way of putting it, over what he described as a lack of transparency over the weekend when SVB was engineered out of existence. He says there are no notes publicly available from the regulators’ emergency meetings over the weekend, and that lack of transparency has a negative effect on the public view of the safety of the financial arena. How do you feel about that? Was there — is there enough transparency about what was going on on that weekend when regulators finally stepped in?”

Gottheimer answered, “Not yet. Which is why I and others have called for an investigation. It starts with this hearing, but it’s got to go a lot deeper. There [were] a lot of question marks. We were all talking over that weekend, and I spoke to the chairman, I spoke to the ranking member, I spoke to a lot of banks, small or medium regional-sized regional banks. We’re all having — and investors and consumers and many non-profits, and we were all having the same discussion of what — they were all panicked, what’s going on. Because it was quiet for a long period, as you know, over that weekend, and a lot of money left small or medium regional banks over the weekend, as we have seen in the numbers. That’s a problem. We should understand why we didn’t have better information, especially those of us on the committee. And we’re going to want to have answers, which is why we’re doing this in-depth investigation.”

Follow Ian Hanchett on Twitter @IanHanchett

BLOG EDITOR: BLACKROCK IS BIDEN'S BIGGEST BRIBESTER. THEY OPERATE OUT OF THE BIDEN WHITE HOUSE UNDER GAMER LAWYER BRIAN DEESE.

Currently, the world is run by moneymen. You only have to look at the way Vanguard and BlackRock own everything between the two of them, even as they use our money to drive those companies into socially destructive and economically wasteful ESG policies (e.g., green energy, DEI, CRT, trans ideology, etc.). (And no, this Reuters article does not debunk the charge, because it ignores the fact that the companies are driven more by ESG policies than by working for their investors. ESG is a huge breach of fiduciary duty.

Australia shows the devastating power that modern banks have over people’s lives

Most Americans cling to the old-fashioned notion that a bank honorably holds their money and pays interest on that money, with the interest coming from the fact that the bank loans that same money to others for an even higher interest rate. We all imagine Jimmy Stewart explaining how banks work to his Bedford Falls neighbors in It’s a Wonderful Life. That’s not true anymore and, Australia’s experience illustrates that, in the 21st century, banks have almost unlimited control over people’s lives.

My parents were loyal to Australia’s Commonwealth Bank way beyond what was logical. It took a lot of evidence from the bank’s own actions for them even to consider changing banks, and even then, it was emotionally painful for them. The reality is that banks have been appalling for a very long time, and their pathology has been progressing exponentially lately, as they no longer try to hide their craven intent.

Here in Australia, for a $10.00 “overdraft” that exists for less than 24 hours, banks charge $25.00. They call this a “fee” because, if they acknowledged that it’s an interest charge, that rate per annum would be over 90,000%!

Banks block our accounts for any number of reasons. My favorite is because a government bureaucracy decides the accountholder transgressed. As we all know, in the world of bureaucracy, everyone is guilty until proven innocent. Getting access to the account again is an uphill battle. You must spend time and money proving that the money you earned and that you put into the bank for safekeeping is, in fact, your property. The costs associated with that proof are yours alone to keep you in your place—and the interest during that time is the bank’s bonus.

Banks devise “products” that promise to pay you interest at a rate that is competitively commercial but build into it certain hoops that you must jump through to achieve that commercial interest rate. They call the hoops a service to help you—to save you time and to focus your energies—but the reality is that they use the fine print to reduce the commercial interest to a theft rate and laugh each month that you fail to comply with the minutiae of their scam.

Banks offer loans that transfer your hard-earned income to their palatial corporate headquarters, where they promote fiscal irresponsibility by lending higher and higher proportions of property value, and they pitch interest rates to reflect risk, even as they assure that they never take a risk. All costs are passed on to the client so that a loan of one million dollars may cost three million by the time the bank forecloses—and it will magically force foreclosure just as the property price and legal fees hit three million dollars. Inflation drives property value increases, and banks help drive that inflation.

One can make a good argument that banking is part of global economic problems. The system allows banks to get bigger and bigger, with profits going, not to people who create, but to those who despoil. This is no longer a case of lenders driving capitalism. Instead, it is a closed system that works with the government to police people and entices them into bad financial decisions (think of the 2008 collapse over equity-free housing loans). It promotes spending much of our productivity, national and personal, on banking services.

Currently, the world is run by moneymen. You only have to look at the way Vanguard and BlackRock own everything between the two of them, even as they use our money to drive those companies into socially destructive and economically wasteful ESG policies (e.g., green energy, DEI, CRT, trans ideology, etc.). (And no, this Reuters article does not debunk the charge, because it ignores the fact that the companies are driven more by ESG policies than by working for their investors. ESG is a huge breach of fiduciary duty.

What the new system means is that we have lost control. We are all working to pay interest on debt that we didn’t need in the first place. Debt investment has created Big Tech, Ukraine, and so much more—unaffordable fads swirling around so-called climate change, unaffordable social programs based on fact-averse policies, all leading to what I’ve heard is 300 trillion in global debt this year (which I suspect underestimates the scope of the problem).

I have a very simple understanding of finance, and probably no understanding of global finance. As I see it, the world works if individuals are in charge of production, innovation, and entrepreneurship, with enterprises functioning at a human level.

The mess we are in is no longer human scale. It is no longer controllable, and to continue to pretend that it is requires short-sighted stupidity at a level no one thought possible two years ago. When we lose human scale, we lose humanity. I’d like to point the finger of blame at a specific person, party, or institution but, basically, it is us. We let it happen.

Nodrog is a pseudonym because Australia is no longer a free country.

Bank TURMOIL Will Make Getting a Mortgage IMPOSSIBLE

Summers: We’ll Either Have ‘Substantially Unsustainable Inflation’ or ‘Fairly Hard’ Downturn Due to Bank Issues

During an interview aired on Friday’s edition of Bloomberg’s “Wall Street Week,” Harvard Professor, economist, Director of the National Economic Council under President Barack Obama, and Treasury Secretary under President Bill Clinton Larry Summers stated that “we are still a substantially unsustainable inflation country unless the economy turns down fairly hard” due to issues in the banking system.

Summers said that while the most recent PCE numbers are better than previous numbers, “I don’t think one should make too much of that. I think we are still a substantially unsustainable inflation country unless the economy turns down fairly hard in response to the credit issues raised by the banking system, and we don’t know yet whether that’s going to happen.”

He added, “So, in a sense, the outcomes here are a bit bifurcated. Either the banking crisis will pass without incident and without large impact on credit, in which case we really do have serious inflation issues and the Fed will have to tighten much more than is priced in, or we’re going to see some kind of real downturn here. And I think both are plausible outcomes and I recognize that there’s a chance we’ll skate through right in between, but I have to say that seems very much odds off to me. Soft landings are very hard, even in the best environment.”

Follow Ian Hanchett on Twitter @IanHanchett

Very Few Are READY For What's Coming!!! (PLEASE PREPARE)

NEXT HUGE BANK FAILURE WILL ROCK THE WORLD? BANKRUPTCIES SURGE, LAYOFFS WORSEN

15 Signs A Massive Car Market Crash Is Already Upon Us

Consumer Sentiment Cracks: First Drop in Four Months

Consumer sentiment unexpectedly worsened in March as worries over a looming recession took hold.

The University of Michigan’s index of consumer sentiment fell to 62.0 in March from 67 in February, an eight percent decline. Compared with a year ago, the index is down four percent.

The midmonth preliminary reading came in at 63.4, so the final number indicates that sentiment continued to deteriorate as March progressed. Economists had expected the final March reading to more or less hold steady with the mid-month score.

Surprisingly, it was not the banking crisis that depressed consumer sentiment.

“This month’s turmoil in the banking sector had limited impact on consumer sentiment, which was already exhibiting downward momentum prior to the collapse of Silicon Valley Bank. Overall, our data revealed multiple signs that consumers increasingly expect a recession ahead,” said Joanne Hsu, the director of the survey.

There were steep declines in both the assessment of current conditions and expectations for the future.

“While sentiment fell across all demographic groups, the declines were sharpest for lower-income, less-educated, and younger consumers, as well as consumers with the top tercile of stock holdings. All five index components declined this month, led by a notably sharp weakening in one-year business conditions,” Hsu said.

Year-ahead inflation expectations fell from 4.1 percent in February to 3.6 percent, the lowest reading since April 2021. Long-run inflation expectations came in at 2.9 percent for the fourth consecutive month.

Walmart Reports A Large Number Of Store Closings As Catastrophic Retail Collapse Intensify

A CLOSE LOOK AT BIDENOMICS

CALIFORNIA HAS THE MOST ILLEGALS IN THE COUNTRY AND THE MOST HOMELESS. NOT HARD TO DO THE MATH ON THAT ONE.

VIDEOS

THE NIGHTMARE BEGINS IN JULY!? FINANCIAL CRISIS 2.0, PAYCHECK TO PAYCHECK CROWD

Bank TURMOIL Will Make Getting a Mortgage IMPOSSIBLE

Wave of Loan Defaults Hit the Real Estate Market (Housing Market Warning)

Middle Class Families Can No Longer Afford Rent As Prices Hit Astronomical Levels

Report: 62% of American Consumers Live Paycheck to Paycheck

A report revealed 62 percent of United States adults live paycheck to paycheck.

A report by PYMNTS and LendingClub, a peer-to-peer lending platform, revealed that as of February, 62 percent of Americans live paycheck to paycheck, including 48 percent of high-income consumers.

The report noted that though inflation is lower than it was in July, consumers are still contending with rising costs.

“Inflation has made life more and more expensive, and consumers have already made moves to cope, such as pulling back on discretionary expenses,” the report read. “But one can only pull back so far on spending, and PYMNTS’ data reveals that consumers are finding another way to navigate their lower purchasing power.”

The report observed that for some people “supplemental income may be the key” and noted that about a quarter of consumers had a side job in addition to 17 percent who had other forms of supplemental income.

The report noted 39 percent of those who lived paycheck to paycheck “with issues paying their bills” mentioned “extraordinary expenses” as their reason for seeking side work.

Some 55% percent of respondents reported their supplemental income grew as a share of their total income over the last 90 days.

The report surveyed 4,125 U.S. consumers from Feb. 7 to Feb. 23 and also considered economic data from other sources.

A February press release from LendingClub indicated that in January 60 percent of consumers were living paycheck to paycheck, two percent lower than in February.

The press release also touched on data about outstanding credit card balances, with the average consumer having credit card debt totaling 35 percent of their savings.

However, this figure varied among different consumer groups. Those who indicated they were living paycheck to paycheck without issues paying their bills maintained credit card balances equaling 62 percent of their savings, and those who were living paycheck to paycheck and had trouble paying their bills had credit card debt exceeding their available savings by more than 50 percent.

The Retirement Crisis Financially Destroys The Entire Baby Boomer Generation

WH: Biden 'Is Going to Focus on the American People' -- But He's Going to UK and Ireland Next Week

(CNSNews.com) - The Biden White House had no comment Tuesday on former President Donald Trump's arraignment.

President Joe Biden, however, flashed a big, wide smile when reporters shouted questions about Trump’s indictment as they were ushered out of the room where Biden was meeting with his science and technology advisers.

At the White House press briefing on Tuesday, spokeswoman Karine Jean-Pierre said, "It's an ongoing case, so we’re just not going to comment on the case specifically itself.

"Look, the President is going to focus on the American people, like he does every day," Jean-Pierre said.

"He is not — this is not something that is a focus for him. He is going to focus on things like making sure that the — that we lower — continue to lower prices for the American people."

At least seven times, in response to other questions, Jean-Pierre repeated that Biden's focus "is on the American people."

So it came as a bit of a surprise on Wednesday morning, when Jean-Pierre announced that "President Joseph R. Biden, Jr. will travel to the UK (Northern Ireland) and the Republic of Ireland from April 11-14."

It's unclear how this underscores Biden's focus on the American people.

According to the White House statement issued by Jean-Pierre:

"President Joseph R. Biden, Jr. will travel to the United Kingdom and Ireland from April 11-14.

"President Biden will first travel to Belfast, Northern Ireland from April 11-12 to mark the tremendous progress since the signing of the Belfast/Good Friday Agreement 25 years ago and to underscore the readiness of the United States to support Northern Ireland’s vast economic potential to the benefit of all communities.

"The President will then travel to Ireland from April 12-14. He will discuss our close cooperation on the full range of shared global challenges. He will also hold various engagements, including in Dublin, County Louth, and County Mayo, where he will deliver an address to celebrate the deep, historic ties that link our countries and people.

"Additional information about the trip will be forthcoming."

President Biden often refers to his Irish roots, so the upcoming trip would have personal meaning for him.

Here are the various comments Jean-Pierre made at Tuesday's press conference about Biden's "focus on the American people."

-- "Again, our focus right now is on the American people. And I’m just not going to comment on any ongoing — ongoing case."

-- "What I can tell you for sure is that the President is focused on the American people. That, I know for sure."

--"Look, our focus is always going to be on the American people, doing everything that we can to make sure that we lower costs and meet the American people where they are, which is why the President took the actions that he has taken this past — this past year."

-- "But again, that’s the main — the main focus for this President is the American people. We’ll continue to work with all producers and consumers to — to ensure energy markets, support economic growth, and lower — again, lower prices for the American consumer."

-- "And so, you know, that is what the President is going to continue to focus on: on how to — how do we lower the prices for the American people."

-- "You’re seeing companies, like Micron, take action and continue to invest here in America. And that’s what the President is focused on."

-- "Look, the President is focused on securing America’s energy independence.

-- "So he has an economic policy that’s going to build — build the economy from the bottom up, middle out. That’s going to be his focus. But also lowering costs for the American people, something he talks about very often."

Miserable and Broke in the US? Blame Reagan

I Drove Around California For A Month. It Was A Disaster.

Food Insecurity in America Reaches the Highest level in Four Years

Major US Asset Manager is Limiting Withdrawals as Investors Race to Get Out Before the Next Crash

https://www.youtube.com/watch?v=9rVZtj7BOow

Half The U.S. Is Worse Off - How Are You Feeling About The Economy?

What Retirement REALLY Looks Like: The Inside Story

BANKS IN FEAR, BIG LENDING PULLBACK, DEFAULTS SURGE, REAL MONEY COMING BACK

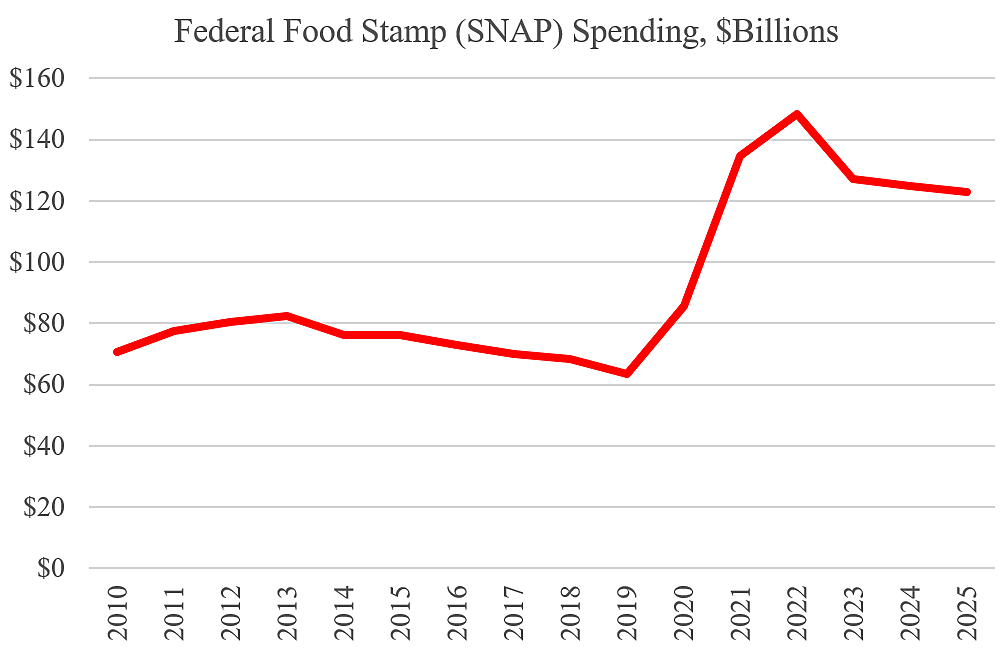

Food Stamp Spending Doubles to $127 Billion

")

Federal government spending soared 40 percent between 2019 and 2023. The government passed large spending bills in response to the pandemic, but spending remains high today even though the crisis has passed.

The ratcheting‐up of spending is evident with the Supplemental Nutrition Assistance Program (SNAP). SNAP benefits, or food stamps, are administered by the states but funded by the U.S. Department of Agriculture (USDA) and ultimately federal taxpayers.

SNAP spending doubled from $63 billion in 2019 to $127 billion in 2023. The Congressional Budget Office (CBO) projects that spending will dip as pandemic benefits expire but will remain far above the 2019 level, as shown in the chart.

Here are some causes of the SNAP spending spike:

- The number of recipients increased from 36 million in 2019 to 42 million in 2023. In 2019, CBO projected that the number would fall to 34 million by 2023.

- The March 2020 pandemic bill provided additional SNAP benefits called emergency allotments, and the Biden administration boosted the amounts. The benefits ended in March 2023.

- The December 2020 pandemic bill temporarily increased benefits 15 percent, and the Biden administration extended the increase through September 2021.

- Some SNAP recipients are subject to a three‐month limit on benefits. This work requirement was suspended during the pandemic but is set to be reinstated in 2023.

- Recipients were allowed to delay eligibility recertification during the early pandemic.

- The 2018 farm bill directed the USDA to update the Thrifty Food Plan (TFP), which helps to determine benefit amounts. Angela Rachidi says the update should have been cost‐neutral, but in 2021 the USDA permanently boosted overall benefits by 21 percent.

- SNAP benefits are adjusted annually for inflation.

Some of these changes were temporary, but the TFP and inflation adjustments boosted benefits permanently. AEI analysts calculate that the maximum benefit for a family of four has jumped 46 percent since 2019, while CBPP analysts calculate that the average per‐person benefit has jumped 50 percent.

SNAP is up for reauthorization in this year’s farm bill, which is an opportunity for policymakers to cut costs. The federal government needs to pursue broad spending reforms to reduce dangerously high budget deficits.

Here are some options for SNAP reform:

- Beef up work requirements, as proposed by two dozen House Republicans.

- Eliminate broad categorical eligibility, which states use to loosen eligibility standards notes Leslie Ford.

- Repeal the 21 percent TFP increase, which was an administrative action that costs taxpayers more than $20 billion a year.

- Convert SNAP to a fixed block grant for the states and cut spending.

- Devolve the SNAP program, including funding, to the states as part of a broader effort to revive federalism. There are few advantages in funding such programs federally but many disadvantages.

Originally published in Cato at Liberty ( titled "SNAP Spending Doubles to $127 Billion").

JOE BIDEN: LYING SOCIOPATH GAMER PARASITE LAWYER!

Despite his Wall Street, big business, Big Tech, and billionaire donations, Biden has attempted to portray himself as a small-town fighter from Scranton, Pennsylvania. JOHN BINDER

NOT ONE CRIMINAL LOOTING BANKSTER WIL EVER GO TO PRISON SO LONG AS THE LAWYER-POLITICIAN DEMS RUN THE ECONMY FOR THE BANKSTER CLASS.

“This was not because of difficulties in securing indictments or convictions. On the contrary, Attorney General Eric Holder told a Senate committee in March of 2013 that the Obama administration chose not to prosecute the big banks or their CEOs because to do so might “have a negative impact on the national economy.”

Banking Crisis just got WORSE. Fed Reports $400 BILLION in Losses.

NOW WATCH CALIFORNIA ! NOT ! CUT ILLEGALS FROM 'FREE' HEALTHCARE!

'CREDIT CARD' Joe Biden Moves to Cut Medicare Advantage

")

President Joe Biden’s administration announced that it would cut Medicare Advantage, after the president has frequently claimed that Republicans want to slash Medicare and Social Security.

The Centers for Medicare and Medicaid Services (CMS) announced this week that they would cut Medicare Advantage by 1.12 percent in 2024, which is not as significant a cut as what the administration proposed two months ago.

Bloomberg reported:

The agency will also phase in controversial changes that determine payments based on the severity of patients’ health problems. That policy will take effect over three years instead of one year, after the proposal drew fierce criticism from the industry.The changes add up to a near-term victory for the industry, which had argued that the Biden administration went too far in its initial proposal. But the policy may mark the start of a period of slower growth for a market that has doubled in size in the last decade, driving growth and profits at major insurers.

Biden has proposed these cuts to Medicare Advantage as he has frequently accused Republicans of wanting to slash Social Security and Medicare as part of a potential compromise to address the coming debt ceiling deadline.

Republicans such as Sens. Steve Daines (R-MT), Tom Cotton (R-AR), and Rep. Kevin Hern (R-OK), the chairman of the Republican Study Committee (RSC), have called out Biden’s apparently hypocrisy.

Breitbart News reported that Biden sponsored a bill in 1975 that would sunset and reauthorize all federal programs, which includes Social Security and Medicare.

“We must… begin reviewing existing programs to determine whether they are still effective, and whether they are worth the money that we are putting in them. We must eliminate the wasteful ones,” Biden said when introducing the 1975 legislation.

“One thing that we have all observed is that once a federal program gets started, it is very difficult to stop it, or even change its emphasis, regardless of its performance in the past,” then-Sen. Biden continued. “It is time for us to require, on a regular and continuing basis, that both the administrators of these programs and we legislators who adopt the programs, examine their operations with care and detail.”

Sean Moran is a policy reporter for Breitbart News. Follow him on Twitter @SeanMoran3.

OBAMACARE WAS WRITTEN BY OBOMB'S BIG PHARMA CRONIES AND THEY'VE RAKED IT IN SINCE!

Obamacare: Still Killing People 13 Years In

On March 23, 2010, President Obama signed his namesake legislation, the Affordable Care Act (ACA) colloquially Obamacare, into law. On March 23, 2023, the Biden-Harris administration celebrated the ACA's thirteenth anniversary. They should be holding a funeral, not a celebration party.

The ACA has caused countless avoidable American deaths. They are due to Washington's conflation of a piece of paper (an insurance policy) with a professional service: medical care.

Xavier Becerra, the Health and Human Services secretary, astonishingly missing during the entire COVID health crisis, declared the following: "As we celebrate the anniversary of the Affordable Care Act today ... this law has lived up to its name, providing a way for Americans to access quality, affordable health coverage."

The ACA did indeed expand medical insurance to more Americans. In 2000, Medicaid enrollment was 15.6 percent of the U.S. population. In 2022, that number has nearly doubled: 27.7 percent of Americans — 92,340,585 individuals — were enrolled in the taxpayer-funded, no-charge-to-enrollees program. Thus, nearly one third of the country has medical insurance and, according to Secretary Becerra, "have the peace of mind that comes with high-quality health care."

Note the conflation of care with insurance. Washington wants you to think having the latter means you get the former, presumably when you need it. Otherwise, what good is insurance? Having insurance does not mean getting timely care. In fact, there is a seesaw effect: as the number of people with government-provided insurance increases, access to care decreases.

Before the ACA, average maximum wait time to see a primary care physician was a unconscionable: 92 days. With ACA expansion of government-provided, no-charge Medicaid insurance, maximum wait times increased to 120 days and produced death-by-queue.

Death by queue is a phrase coined in the United Kingdom, meaning dying while waiting in line for care that is technically possible but unavailable in time to save lives. Death by queue has long been a feature of the vaunted British National Health Service (NHS) and has now become noticeable in the U.S.

In Illinois over three years, 752 Medicaid enrollees died waiting for desperately needed medical treatment. An internal Veterans' Affairs Department audit concluded that "47,000 veterans may have died" waiting in line for care that was technically possible but unavailable. Veterans are covered by federal Tricare insurance.

An accurate estimate of death by queue in the U.S. is not available. In Great Britain, at least "117,000 die[d] on waiting lists for NHS" in 2020 and 2021.

My wife may have been a victim of death-by-queue. She waited seven months before she could see her primary physician for her abdominal pain. The diagnosis was inoperable pancreatic cancer. She died 22 months later. Her case is certainly not unique. Numerous studies prove that delay in diagnosis of life-threatening conditions such as cancer leads to deaths that could be prevented. What is killing these patients is excessive wait times.

The reason for the long wait times and death-by-queue is Washington's repeated fixes applied to healthcare. First there are federal regulations. Physician time that should be spent on patients is consumed by regulatory and administrative burdens.

Second, there is "bureaucratic diversion," when money is taken from clinical care to pay for bureaucracy, administration, rules, regulations, compliance, and oversight. Each dollar spent on these non-clinical activities is a dollar that cannot be spent on patients. Estimates of this outlay range from 31 percent to 50 percent of all U.S. healthcare spending. In 2021, the U.S. expended $4.3 trillion on its healthcare system. Thus, Washington took roughly $2 trillion away from patients to pay federal (and state) activities that provide no care. Imagine how short wait times could be — can you say 48 hours?! — with an additional $2 trillion available to pay providers! Possibly my wife would be alive today.

For decades, Washington has been fixing health care with federal programs such as Medicare and Medicaid (both created in 1965), the Emergency Medical Transport and Labor Act of 1986 (which created health care's unfunded mandate), the Health Insurance Portability and Accountability Act of 1996, and the ACA (2010). Prior to 1965, the U.S. expended 6.5 percent of GDP on health care. Last year, it was 19.7 percent.

The end result of federal over-regulation and all that spending is what we have today: death-by-queue and impending bankruptcy of both Medicare and possibly the U.S.

Biden's "celebration" of Washington's healthcare achievements is a travesty. By constantly increasing government-provided insurance, Democrats increase the number of Americans who die waiting too long for life-saving care.

If we want to shrink wait times, see the doctor before it's too late, and save American lives, kick Washington out of healthcare (the system), stop budget-focused bureaucrats from dictating our health (medical) care, and reconnect patients directly with their doctors with no third-party decision maker in between.

Deane Waldman, M.D., MBA is professor emeritus of pediatrics, pathology, and decision science at the University of New Mexico. He is the former director of the Center for Healthcare Policy at Texas Public Policy Foundation and author of multi-award-winning book Curing the Cancer in U.S. Healthcare: StatesCare and Market-Based Medicine.

Image via Max Pixel.

Josh Hawley: Biden’s ‘Concierge Service’ for Illegal Aliens Comes at Expense of Americans’ Jobs, Wages

President Joe Biden’s “concierge service” for illegal aliens comes at the expense of Americans’ jobs and wages, Sen. Josh Hawley (R-MO) said this week.

In a letter to Department of Homeland Security (DHS) Secretary Alejandro Mayorkas, Hawley blasted the administration’s migrant mobile app — known as CBP One — that has released more than 30,000 foreign nationals into the United States since early January by allowing them to schedule appointments at the southern border.

Specifically, the migrant mobile app allows foreign nationals who are pregnant, mentally ill, elderly, disabled, homeless, or crime victims living in Mexico to schedule appointments at the border for release into the U.S. interior.

Hawley writes that the migrant mobile app is in effect “like making a restaurant reservation” and will have dire effects on Americans’ jobs and wages:

Under your leadership, the Department is marketing a new phone app, called CBP One, that allows unauthorized migrants to reserve a time to cross the border, like making a restaurant reservation. How convenient. I gather the app is meant to expedite asylum claims, or so your Department’s promotional material says. But I noticed you said nothing about asylum when I asked you at the hearing. And the Texas Monthly has recently reported that “[a]t no point does the app ask users ‘Are you seeking asylum?’” Worse, when migrants show up at the border to enter the country, they “are given no interviews and asked no questions about vulnerabilities they listed in the app or about why they’re seeking asylum in the U.S.—they’re simply released into the country on official parole.” [Emphasis added]

…I imagine there are plenty of Americans who would appreciate this level of service from their government. Your choice to spend untold sums of taxpayer money—you said you had no idea what it cost—on concierge service for illegals is baffling. It is also revealing. It demonstrates your priorities: open borders, no matter the cost to Americans; no matter the jobs lost, the wages lost, the drugs flooding our schools. [Emphasis added]

Hawley calls the migrant mobile app “a full-on institutionalization of an open border and the abuse” of U.S. asylum laws, pressing Mayorkas to disclose how many foreign nationals have used the app since its inception, how many are expected to use the app after border controls end in May, and if the app will be updated to ask applicants if they have legitimate asylum claims.

The tech companies involved in the migrant mobile app’s creation, Hawley writes, should also be disclosed to the public and Congress along with the taxpayer costs associated with the app.

Biden’s expansive Catch and Release network at the border is pumping hundreds of thousands of foreign workers, often illegal, into working- and middle-class American jobs. At the same time, fewer Americans are working.

As Breitbart News reported, at the end of 2022, there were nearly two million fewer native-born Americans working compared to the same time in 2019, while two million foreign-born workers have been added to the workforce compared to the same time period.

In particular, the decline in the labor participation rate among working-class native-born Americans has dropped to 70.3 percent at the end of last year compared to 71.4 percent in 2019, 74.8 percent in 2006, and 76.4 percent in 2000.

Working-class native-born American men, those without a bachelor’s degree between 25 to 54 years old, had only an 83.7 percent labor participation rate at the end of 2022 — declining consistently since the year 2000.

The Biden administration has largely ignored efforts to get native-born Americans back into the workforce, instead adding millions of foreign workers to the labor market which adds downward pressure, particularly for working-class Americans in terms of finding jobs and securing higher wages.

John Binder is a reporter for Breitbart News. Email him at jbinder@breitbart.com. Follow him on Twitter here.

Gallup: 83% of Americans View Economic Conditions as 'Poor/Only Fair'

")

(CNSNews.com) -- A new survey shows that 83% of American adults view current economic conditions as "only fair" or "poor," reported Gallup. In addition, 72% think economic conditions are getting "worse."

On other issues, only 2% of Americans said "Environemnt/Pollution/Climate change" was the most important problem facing the country, and only 2% said the "situation with Russia" was a top problem.

In the poll, conducted Mar. 1-13, 2023, Gallup asked a random sample of 1,009 adults living in all 50 states and D.C., to describe current economic conditions. In response, 43% said poor, 40% said only fair, 15% said good, and 1% said excellent.

")

As for their outlook on the economy, only 23% said it was "getting better" while 72% said "getting worse."

Gallup also asked, "What do you think is the most important problem facing this country today?"

In response, 33% said "economic problems (net)," with "high cost of living/inflation" topping the list of concerns at 12%.

Another 12% of Americans said the "economy in general."

")

As for non-economic problems, 20% said "the government/poor leadership" is the most important problem facing America today; 11% said "immigration."

From there, the numbers dropped way off, with 3% citing "crime/violence," 2% citing "race relations/racism," and 2% saying the "situation with Russia."

Despite the Biden administration's push to eliminate fossil fuels and impose a green agenda across the country, only 2% of Americans said climate change was the most important problem.

Also, only 1% of Americans said "guns/gun control" was the main problem. And another 1% said "police brutality."

To read the survey, click here.

")

Very Few Are READY For What's Coming!!! (PLEASE PREPARE)

NEXT HUGE BANK FAILURE WILL ROCK THE WORLD? BANKRUPTCIES SURGE, LAYOFFS WORSEN

15 Signs A Massive Car Market Crash Is Already Upon Us

Consumer Sentiment Cracks: First Drop in Four Months

Consumer sentiment unexpectedly worsened in March as worries over a looming recession took hold.

The University of Michigan’s index of consumer sentiment fell to 62.0 in March from 67 in February, an eight percent decline. Compared with a year ago, the index is down four percent.

The midmonth preliminary reading came in at 63.4, so the final number indicates that sentiment continued to deteriorate as March progressed. Economists had expected the final March reading to more or less hold steady with the mid-month score.

Surprisingly, it was not the banking crisis that depressed consumer sentiment.

“This month’s turmoil in the banking sector had limited impact on consumer sentiment, which was already exhibiting downward momentum prior to the collapse of Silicon Valley Bank. Overall, our data revealed multiple signs that consumers increasingly expect a recession ahead,” said Joanne Hsu, the director of the survey.

There were steep declines in both the assessment of current conditions and expectations for the future.

“While sentiment fell across all demographic groups, the declines were sharpest for lower-income, less-educated, and younger consumers, as well as consumers with the top tercile of stock holdings. All five index components declined this month, led by a notably sharp weakening in one-year business conditions,” Hsu said.

Year-ahead inflation expectations fell from 4.1 percent in February to 3.6 percent, the lowest reading since April 2021. Long-run inflation expectations came in at 2.9 percent for the fourth consecutive month.

No comments:

Post a Comment